02 · arr audit

The "$10M ARR" doesn't reconcile — by their own numbers.

"approaching $10M ARR" · "$1M/week, approaching $10M"polsia.com marketing · 2026-05-22

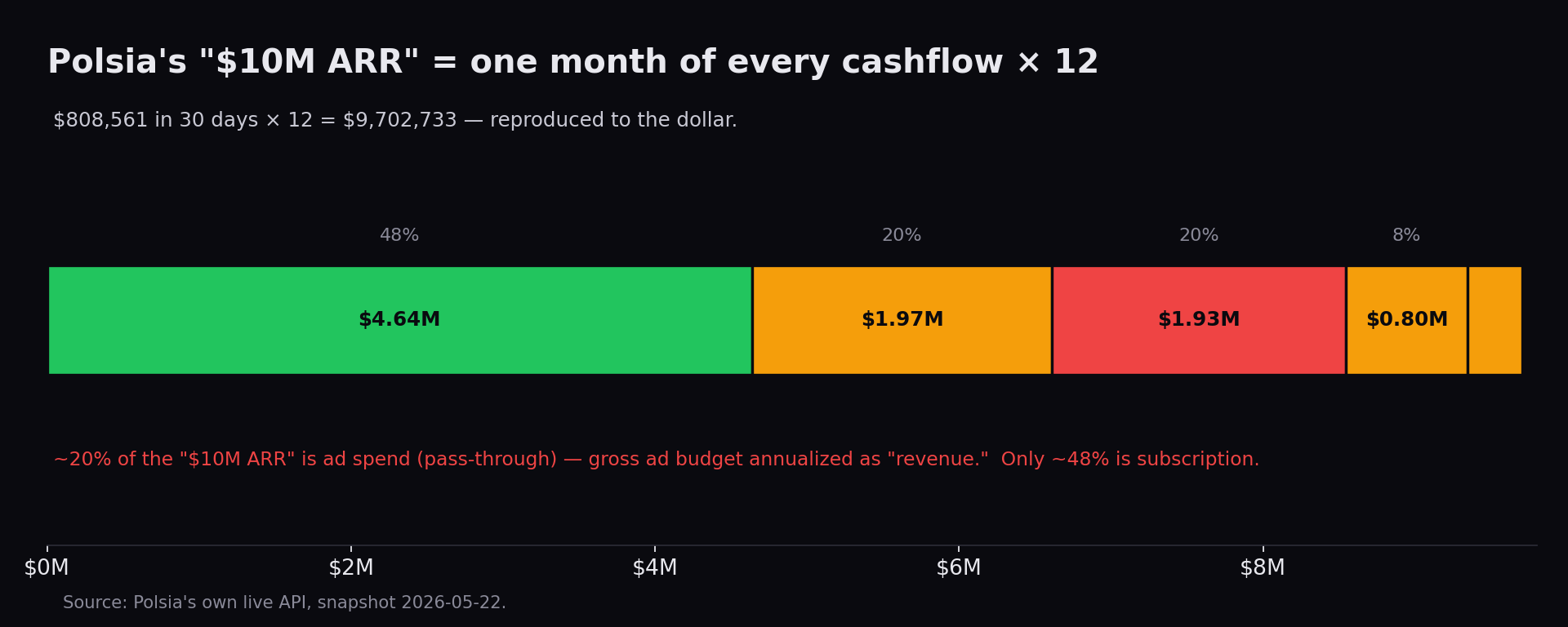

A · What the “$10M ARR” is actually made of

The headline $9.70M is five annualized 30-day cashflow buckets (snapshot 2026-05-22): subscriptions $4.64M (47.8%), one-off packs $1.97M (20.3%), ad-spend pass-through $1.93M (19.9%), 1-hour “boosts” $0.80M (8.2%), user-company payments $0.36M (3.7%). ~20% of their “ARR” is literally ad spend — money flowing through for ad buys, annualized as revenue. Only the subscription slice (~$4.6M) is recurring revenue at all — and even that isn't durable or profitable: it churns ~48%/month (so it doesn't actually recur a year out — real ARR ≈ $0, above), and AI compute alone eats ~57% of every subscription dollar (§02-D). The ~$4.6M is not a profitable recurring business; it's a number that evaporates and loses money on the way.

reproduce — public, no auth (snapshot 2026-05-22)

curl -s https://polsia.com/api/public/live/dashboard | jq '.stats.arr_usd' # "9702733" = (subscription + instant_packs + ad_spend + boosts + user_company over 30d) × 12 — ~20% is ad spend

B · The "$1M a week" lasted about a week

Their own arrHistory peaked at +$894K the week ending May 14, then +$347K the next — a 61% drop. Live, the trailing-7-day add is +$282K and still falling. Decelerating, not accelerating; and the near-monotonic curve despite their own ~48% monthly churn is what cumulative gross-flow looks like, not net recurring ARR.

| Week ending | ARR add | vs peak |

|---|---|---|

| May 14, 2026 | +$894K | peak |

| May 21, 2026 | +$347K | −61% |

| Trailing 7d (live) | +$282K | −68% |

C · The run-rate ladder keeps moving its own bottom rung

Every figure here is the founder's own — but the starting number changes with the telling. On Apr 23: "$700k → $7M in 7 weeks." By May 17: "$250k → $9.5M in 3 months." The endpoint rises, the baseline drops, the window stretches. (And May 8: "$8.5M run rate… got hit by a $1M Anthropic bill last month" — the LLM-cost side of the same ~48% picture.)

| Date (founder, first-party) | Claimed story | Implied baseline |

|---|---|---|

| Apr 23, 2026 | $700k → $7M | $700k / 7 weeks |

| May 8, 2026 | $8.5M run rate | "$1M Anthropic bill last month" |

| May 17, 2026 | $250k → $9.5M | $250k / 3 months |

D · And even the recurring slice doesn’t pay for itself

Same-period, no annualization: their own daily_ai_cost ($7,344) against their own daily subscription run (sub-MRR ÷ 30 ≈ $12,887) — AI compute alone eats ~57% of every subscription dollar. What’s left doesn’t cover the human ops team + infra, so the recurring line is net-unprofitable (their dashboard even publishes a per-task cost). The DD question the round skipped: where’s the durable, profitable business?

reproduce — public, no auth (snapshot 2026-05-22)

curl -s https://polsia.com/api/public/live/dashboard | jq '{ai_cost_per_day: .stats.daily_ai_cost, sub_mrr: .stats.subscription_mrr}' # $7,344/day compute ÷ ($12,887/day recurring) ≈ 57% to compute alone