A programming note: I initially wanted to cover Microsoft’s earnings today, but I am changing the schedule a bit as I felt more inspired to write today’s piece.

Almost two decades ago, Hewlett-Packard (HP) was the first tech company to exceed $100 Billion annual revenue threshold in 2007. At that time, HP had 172k employees. The very next year, IBM joined the club, but IBM had almost 400k employees.

Today’s megacap tech companies all exhibit a common characteristics: their growth is pretty much decoupled from their headcount. Intuitively, this might not be a news to anyone, but when I sat down and carefully jotted the numbers, the extent of the decoupling even before Generative AI truly came to the scene was a bit astonishing to me.

Let me show you one by one.

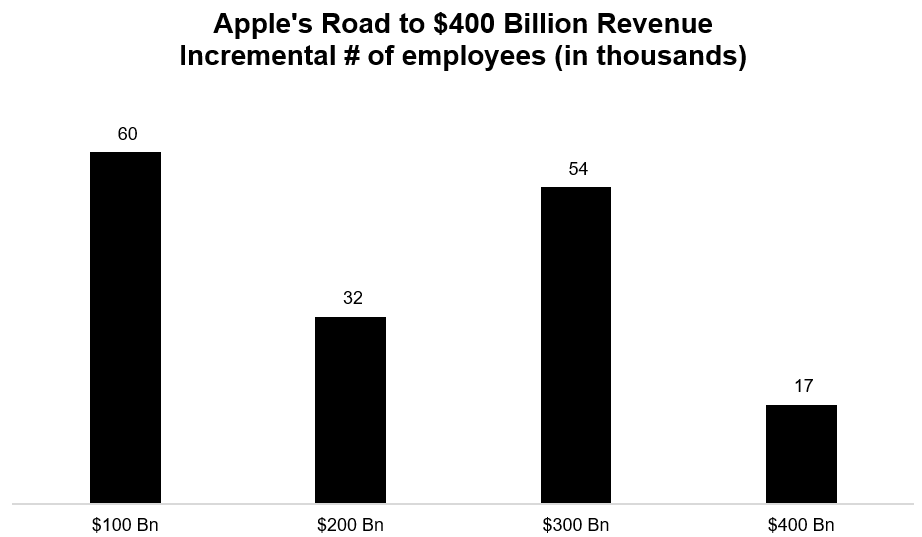

Apple reached its first $100 Billion revenue with just 60k employees in 2011. The next incremental $100 Billion revenue took just half of the incremental number of employees! The most recent incremental $100 Billion revenue for Apple took only ~17k incremental employees.

Of course, a $100 in December 2011 is $144 today after adjusting for inflation. Moreover, while Apple was certainly not the worst offender of pandemic over hiring, their journey from $200 Billion to $300 Billion did break the overall pattern.

Let’s see some other companies to see how their journey to become a behemoth evolved over time.

Alphabet hasn’t quite reached $400 Billion revenue yet, but they are likely to get there next quarter! Alphabet required 76k employees to get to their first $100 Billion. Their most recent incremental $100 Billion? Just 11,000! (assuming they add another 3k employees in 4Q’25)

Now, Alphabet certainly did over hire people post-Covid which they corrected later. Despite such over hiring, Alphabet fits the broader pattern: each incremental $100 Billion revenue took a noticeably fewer incremental employees!

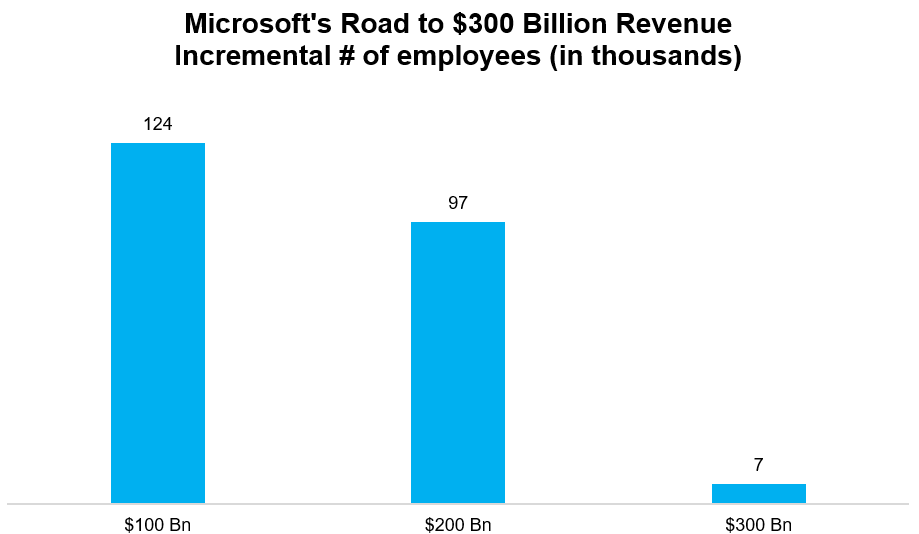

Microsoft also hasn’t reached $300 Billion revenue milestone yet, but they will get there next quarter.

Historically, Microsoft used to be much more human capital intensive company as they required 124k and 97k incremental employees to get to $100 Billion and $200 Billion revenue milestones respectively.

But their most recent $100 Billion? Only SEVEN thousand!

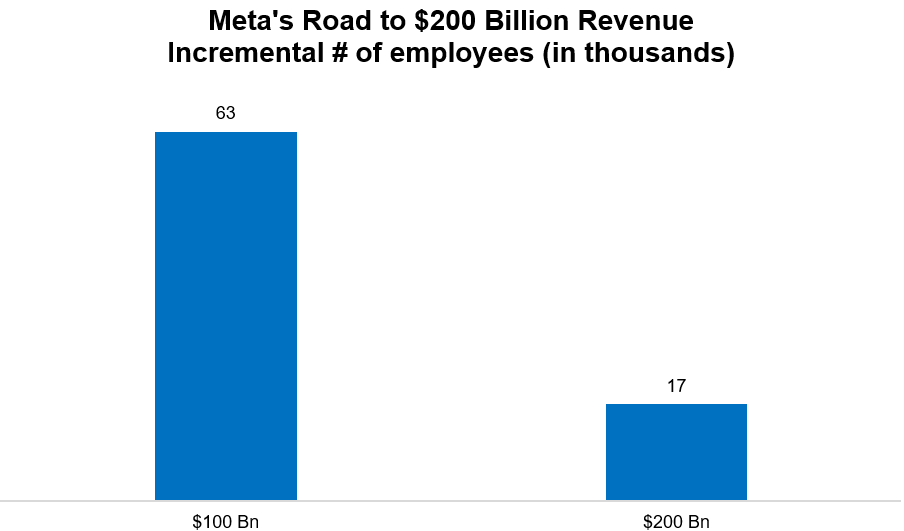

Meta is the youngest of these companies. They will likely reach $200 Billion revenue milestone next quarter. Their first $100 Billion took 63k employees while the recent one will likely take one-third of that number!

As they say, the first hundred billion is the most difficult one!

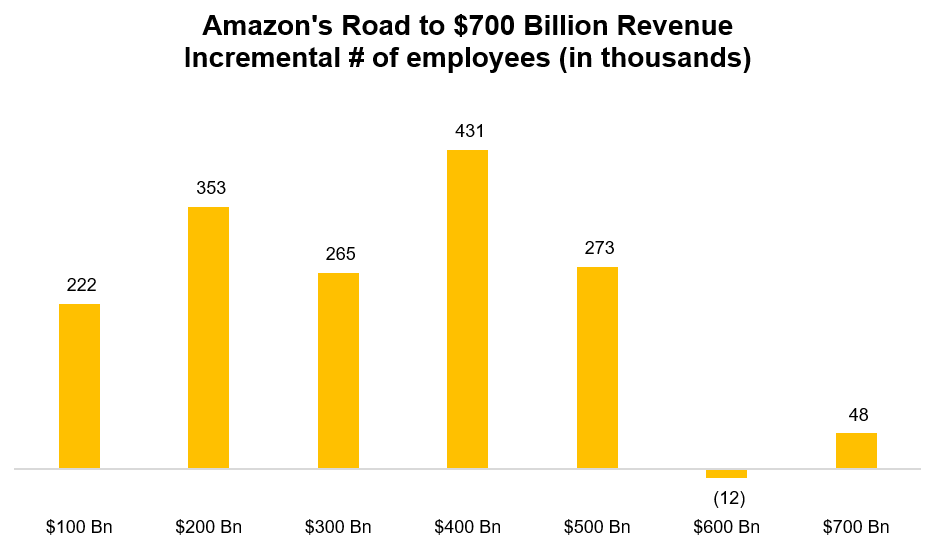

I almost didn’t want to include Amazon here given their massive retail employee base. But after taking a peek at their number, I decided to include them as well.

Unlike the other tech companies, Amazon really didn’t exhibit much of a pattern for their journey to $500 Billion revenue milestone. In fact, their hiring pattern is perhaps the poster child of post-pandemic over hiring as the company really was in the thick of pandemic induced massive upward demand shock and misread the post-pandemic hangover. While historically they took 200k to 400k employees for their incremental $100 Billion revenues, they added their last $200 Billion revenue with only 36k incremental employees!

I do want to note that Andy Jassy in his June 2025 memo to employees said the following:

As we roll out more Generative AI and agents, it should change the way our work is done. We will need fewer people doing some of the jobs that are being done today, and more people doing other types of jobs. It’s hard to know exactly where this nets out over time, but in the next few years, we expect that this will reduce our total corporate workforce as we get efficiency gains from using AI extensively across the company.

I wouldn’t be surprised if Amazon reaches $1 Trillion revenue in 3-4 years by adding only ~100-200k incremental headcount. If that happens, it would mean while Amazon required 1.5 million employees to get to $500 Billion revenue, the next $500 Billion revenue would come with only ~10-15% of incremental headcount!

Of course, I haven’t even mentioned the largest company in the world: Nvidia! When they reached $100 Billion LTM revenue in 2024, they only had 30k employees and they will likely reach their next $100 Billion with only ~6-8k incremental headcount!

The trend isn’t necessarily just confined to tech companies either. Walmart’s full-time employees number remained relatively constant for the last 10 years while their revenue grew by $200 Billion during this period. In fact, Walmart recently mentioned that the headcount will remain static for the next three years as well. So, it is likely that Walmart will add $300 Billion incremental revenue since 2015 with basically no incremental headcount!

If you add Apple, Microsoft, Alphabet, Meta, Nvidia’s last $100 Billion incremental revenue, then add Amazon’s last $200 Billion, and Walmart’s ~$300 Billion revenue, we are essentially looking at ~$1 Trillion incremental revenue with only ~100k headcount growth!

Remember, this has happened even before generative AI. The next $1 trillion incremental revenue may require even fewer employees! This is what I mean by the great decoupling between labor and capital has been an ongoing theme for a while now.

It’s also why I believe the narrative around “AGI” may be a little misguided. Many people talk about “AGI” as if you would receive an email on one fine Monday from your company that would read “we have reached AGI. We no longer need your service”.

Personally, I think what is much more likely is that AGI is perhaps not a moment in time, rather we are simply marching towards “AGI” which itself is an asymptote. AI will accelerate the pace at which we would be going towards this “AGI”. Even if in a strictly theoretical sense we never reach “AGI”, the actual difference of reaching and not reaching “AGI” may prove to be minimal in a couple of decades.

There are, of course, deeper societal, political, and philosophical implications for such a world. Exploring the implications in full detail is a bit beyond the scope of this piece. But I do want to highlight some musings related to investment implications.

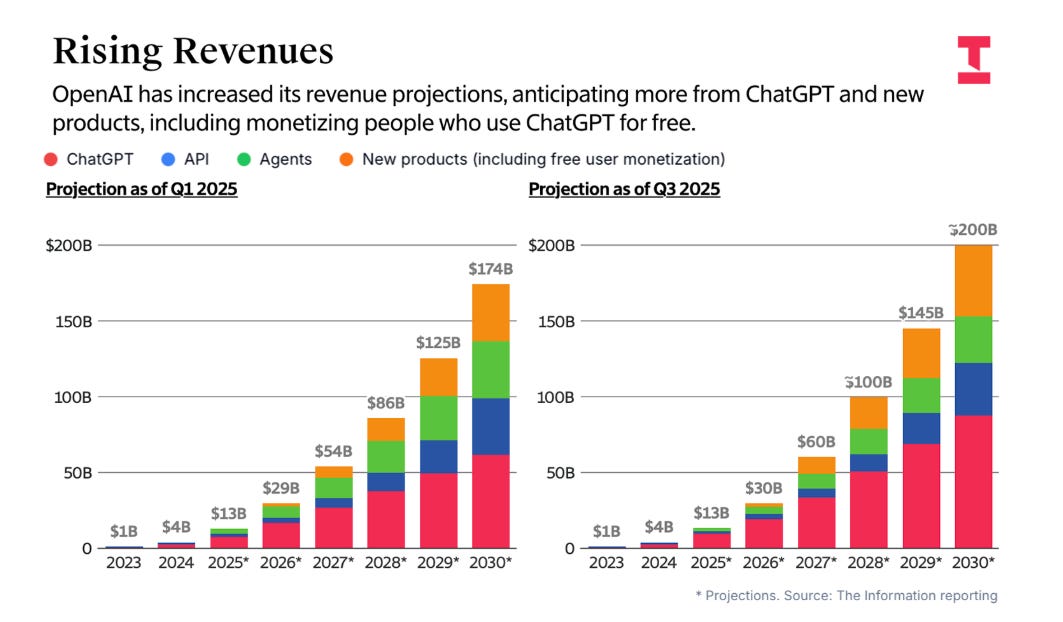

While I used to snicker a bit on OpenAI’s revenue ambitions in the next 5 years, going through big tech’s earnings last week made me want to tone it down a bit. If Reels can scale from $1 Billion revenue run rate to $50 Billion in just three years, perhaps I should be less cynical about OpenAI’s ability to go from $30 Billion revenue in 2026 to $200 Billion revenue in 2030. I am not sure you can quite “model” these things in any precision, but I am updating my opinion that reaching $200 Billion is not a top 0.1 percentile outcome for OpenAI, rather perhaps a top 1-2 percentile outcome (which is ~10-20x higher probability). Given this possibility, I am updating the distribution of outcomes in my mind for OpenAI.

If OpenAI reaches $200 Billion revenue in 2030, what does that imply for the current crop of big tech companies? Should I update the distribution of outcomes for them as well? It’s a difficult question, but let me share some brief thoughts.

One of the things that I have consistently noticed in my last seven years of following big tech companies is the way investors (including me) often frame the debates in “us vs them” framework. As fundamental analysts and active investors, we are understandably geared to assess the companies in a relative sense, and yet, all these companies have all performed pretty well over the last 10 years even though a lot of concerns around some of these companies indeed proved to be valid.

Is there any doubt that Google search ads consistently lost share to Amazon ads? Is there any doubt that Meta has lost share in time spent to TikTok? Is there any doubt that Google search has and will continue to lose overall query share to ChatGPT?

Of course, one of the reasons such “us vs them” framing turned out to be misguided is we persistently underestimated the potential for a new dynamic to expand the market itself. Another thing that I believe is often under appreciated for all these tech companies is the massive consumer surplus they tend to leave on the table which gives them ample time to respond to somewhat unforeseen concerns.

Imagine how many articles we have all read about the mental health crisis that is allegedly accelerated by social media companies. I don’t doubt that these companies can inflict negative impact on some users, but I have always believed the core consumer surplus for social media companies is deeply underappreciated. Take the recent hysteria around short form video. Perhaps almost everyone reading this piece is convinced that this is just “brain rot” imposed on us. I personally don’t find short-form videos too addicting (but I don’t doubt that it might be too addicting for many), but I do think it is deeply underappreciated that during any point of the day, I can open an app and I am absolutely guaranteed to watch a video that would make me smile for free! Similarly, while countless pieces will be written on ChatGPT related psychosis, it is perhaps not quite deeply internalized how incredible it is that we can type something to a query box and learn about anything homo sapiens has ever figured out so far!

One of the reasons I think they are not deeply internalized is it actually feels uncomfortable to write about. You almost feel like a “Meta or OpenAI shill”. It may be much more socially acceptable to worry about the impact of big tech companies than to write think pieces on how our lives have become consistently better thanks to these tech companies!

One of my current major takeaways from this exercise was the broader economy may increasingly be more of a smiling curve: on one hand you have these big tech companies dominating the economy without adding much headcount in the process, on the other hand they will keep empowering “little” guys: think more Amazon 3P sellers, more content creators, more niche app developers etc. while everyone in the middle continues to be squeezed. As I have mentioned repeatedly, this has been an ongoing theme. AI is simply a further accelerant.

Even if this is true, this won’t preclude us from interim hiccups, and I expect narrative to swing from one extreme to the other even though the destination may not quite change much.

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 64 Deep Dives here.

Current Portfolio:

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below:

This post is for paying subscribers only

Already have an account? Sign in.