Part of Teaching an AI Agent to Make Beautiful Charts

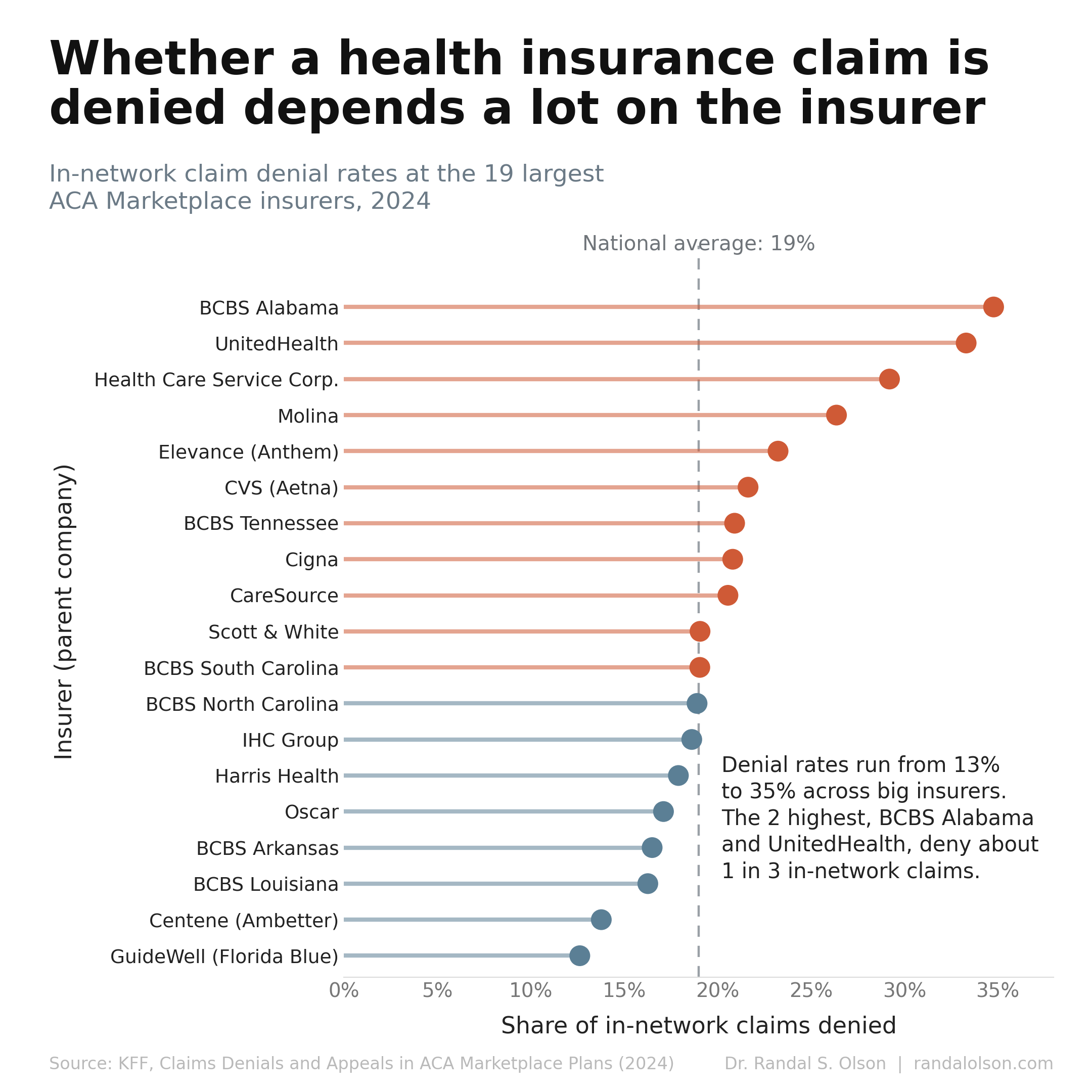

Health insurers turn down a lot of claims, and they do not all turn them down at the same rate. In 2024, the largest plans sold on the Affordable Care Act marketplace denied anywhere from 13% to 35% of the in-network claims their members filed. Whether your claim got paid depended a lot on whose name was on your card.

Claim denials are back in the national conversation. Luigi Mangione, charged in the December 2024 killing of UnitedHealthcare CEO Brian Thompson, was back in court this week for a pretrial hearing, and legal analysts expect his trials to double as a referendum on a health care system many people find costly and hard to navigate. He has pleaded not guilty. The outrage is easy to find. The data on how insurers actually behave is harder to come by, so here is what the federal numbers show.

A denied claim depends a lot on your insurer

Nationally, insurers on the federal HealthCare.gov marketplace denied about 1 in 5 in-network claims in 2024, or 19%. That is roughly 85 million denied in-network claims in a single year. The rate is not uniform, though: among the largest insurers it ran from 13% to 35%, so the company holding your policy can change your odds of a denial by nearly 3 times.

A 19% average makes denials sound like a coin that lands the same way for everyone. It does not. The spread across insurers is wide enough that the single biggest factor in whether a claim gets paid may be which plan you happened to buy.

Size doesn't predict who denies the most

The 2 highest denial rates among the largest insurers belong to Blue Cross Blue Shield of Alabama (34.8%) and UnitedHealth (33.3%), each rejecting about 1 in 3 in-network claims. UnitedHealth is the largest health insurer in the country, and its marketplace arm sits near the top of the denial list.

Bigger does not mean stingier, though. Centene's Ambetter plans and GuideWell's Florida Blue handled the most in-network claims of any companies here, tens of millions each, yet posted 2 of the lowest denial rates, about 14% and 13%. Scale and denial rate move independently.

Most denials aren't about whether care was necessary

The popular image of a denial is an insurer overruling a doctor on whether a treatment is needed. That is the exception. Only about 5% of denied in-network claims were turned down because the care was deemed not medically necessary. The rest were administrative, for an excluded service, for a missing referral or prior authorization, or for a reason the insurer never specified.

In fact the single largest category, 36% of denials, was an unexplained "other." A system that rejects tens of millions of claims a year and files more than 1/3 of those rejections under no stated reason is hard for an outsider, or a member, to audit.

Almost no one appeals, and most appeals lose

Members rarely push back. Consumers appealed fewer than 1% of denied in-network claims in 2024, and when they did, insurers upheld the original denial about 2/3 of the time.

So a denial is usually the end of the story. The vast majority are never challenged, and most of the few that are get denied again. That mix, common denials and rare, mostly unsuccessful appeals, is part of why one CEO's killing turned into a national argument about the whole industry.

What this data does and doesn't capture

This is the most complete public window into claim denials, and it is still partial. The figures cover only the insurers that sell through the federal HealthCare.gov platform, about 16 million of the 21.3 million people in ACA marketplace plans in 2024. They leave out employer coverage, Medicare, Medicaid, and the state-run exchanges. Reporting is not fully standardized, and that large "other" bucket means some of the spread reflects how companies record and process claims, not only how often they refuse care.

Even with those caveats, the variation is the headline. When the same kind of claim is nearly 3 times as likely to be denied at one large insurer as at another, the insurer you carry is not a detail. It is one of the biggest factors in whether your care gets paid for.

How this chart was made

An AI agent built this chart end-to-end as part of the Beautiful Charts with AI series. It pulled the per-insurer denial rates from KFF's analysis of the federal Transparency in Coverage data, built the chart in Python, and iterated on the design until it passed the Tufte Test, a data visualization quality standard from Goodeye Labs. The workflow behind it is public: run the same high-signal chart workflow to make your own.

Data source: KFF's Claims Denials and Appeals in ACA Marketplace Plans in 2024, which analyzes the federal government's Transparency in Coverage data for HealthCare.gov plans. Per-insurer denial rates are read from KFF's own published figures. The dataset used for this chart is available here.