Summary:

- ECB policy announcement due Thursday 11th April; rate decision at 13:15BST/08:15EDT, press conference from 13:45BST/08:45EDT

- Focus will be on how/if policymakers guide markets towards future rate cuts

- Markets fully price a 25bps reduction in June with a total of 83bps of cuts seen by year-end

The incoming data have been mixed since the March ECB meeting. While spot measures of growth have remained weak, the more forward-looking indicators have continued to improve. Inflation has come in broadly as expected in the March staff projections, with some measures of underlying inflation ticking up but wage growth slowing a bit more than anticipated. Today's meeting is therefore likely to be relatively uneventful: most economists expect the Governing Council to leave its key policy language broadly unchanged without formally pre-committing to a June cut. Instead, Lagarde is likely to reiterate that the Governing Council will have “a lot of data” in June to decide whether to lower policy rates. Also don't expect much if any additional color on the likely pace of rate cuts, with emphasis on data dependence

Separately, Lagarde will again emphasize that the ECB is independent of the Fed, which will be helpful for EUR/USD downside as Euro Area data are in a completely different place. And EUR has been in a 5 big figure range for most of the last 16 months or so, so there’s no obvious reason for them to be concerned about the currency. The key question is whether the data will continue to justify a faster pace as well.

Some more details courtesy of Newsquawk

OVERVIEW: Analysts are unanimous in expecting the ECB to stand pat on the deposit rate at 4.0% with markets assigning a circa 92% likelihood of such an outcome. Policymakers continue to guide participants towards a June reduction with even the likes of arch-hawk Holzmann falling into line with such an outcome. With the April decision itself seemingly a given, focus will naturally fall on any tweaks to the policy statement and any hints over forthcoming action. In terms of market pricing beyond April, June is fully priced for a 25bps reduction with a total of 83bps of loosening seen by year-end.

PRIOR MEETING: As expected the ECB opted to stand pat on rates as policymakers continued to monitor progress towards the Bank's inflation mandate. Furthermore, guidance on rates was reaffirmed as stating that "rates will be set at sufficiently restrictive levels for as long as necessary". The accompanying macro projections saw 2024 and 2025 inflation forecasts lowered, leaving the latter matching the Bank's 2% target. At the follow-up press conference, Lagarde noted that the Bank is not yet "sufficiently confident" when it comes to meeting its target. In terms of the policy path beyond the March meeting, Lagarde stated the Bank will know a little more in April but a lot more in June. When it comes to the discussions held during the meeting, Lagarde stated that there was not a discussion over rate cuts but the GC has begun discussing dialling back its restrictive stance. Subsequent source reporting via Reuters noted that policymakers overwhelmingly favour June for the first rate cut, whilst some policymakers floated the idea of a second reduction in July to win over a small group still pushing for an April start.

RECENT ECONOMIC DEVELOPMENTS: Headline inflation in March pulled back to 2.4% from 2.6% with the supercore metric now below 3% for the first time in two years. That being said, services inflation remains uncomfortably high at 4%. The ECB's latest Consumer Inflation Expectations survey for February saw the 1yr-ahead projection slip to 3.1% from 3.3% whilst the 3yr ahead forecast held steady at 2.5%. In terms of market proxies, the EZ 5yr5yr inflation gauge has picked up to 2.32% from around 2.26% at the time of the last meeting. With Q1 GDP not released until 30th April, expectations for the bloc’s growth prospects have instead been guided by survey data which has seen the EZ March composite PMI climb into expansionary territory for the first time since June last year. The accompanying report noted that “expectations for business activity were at their most optimistic since February 2022 during March”. In the labour market, the unemployment rate remains at its historic low of 6.5%.

RECENT COMMUNICATIONS: Since the prior meeting, President Lagarde has continued to reaffirm her guidance from the March meeting that the GC will know a "bit more by April and a lot more by June", whilst noting that "...we cannot wait until we have all the relevant information. To do so could risk being too late in adjusting policy." Chief Economist Lane has stated that the Bank must avoid "giving calendar guidance" but is confident that wage growth is slowing as expected. The influential Schnabel has not given much in the way of clear policy guidance, however, other notable figures such as Villeroy of France have remarked that an ECB rate cut is "very likely" in Spring (describing Spring as April-June 21st). He also noted that the GC needs to take out insurance against a hard landing by starting to cut rates. At the dovish end of the spectrum, Stournaras of Greece put forward the view that the ECB should cut rates twice before the summer break, adding that four rate cuts this year "seems reasonable". In terms of the hawks on the GC, Austria's Holzmann cautioned that investors should consider the risk that the ECB does not lower rates this year, whilst at a later date noting that he has no in-principle objection to a June rate cut, but wants to see more supportive data.

RATES: Analysts are unanimous in expecting the ECB to stand pat on the deposit rate at 4.0% with markets assigning a circa 92% likelihood of such an outcome. With the April decision itself seemingly a given, focus will naturally fall on any tweaks to the policy statement and any hints over forthcoming action. As a reminder, current guidance on rates notes "... rates are at levels that, maintained for a sufficiently long duration, will make a substantial contribution to this goal". ING suggests that the GC’s lightest-touch option for a change in communication would be to alter the existing "confident" inflation is falling but "not sufficiently confident" phraseology. Alternatively, the GC could explicitly declare an outright intention to cut rates at the June meeting (possibly with or without attached conditionality). In terms of market pricing beyond April, June is fully priced for a 25bps reduction with the next cut thereafter fully priced in September and a total of 83bps of loosening seen by year-end.

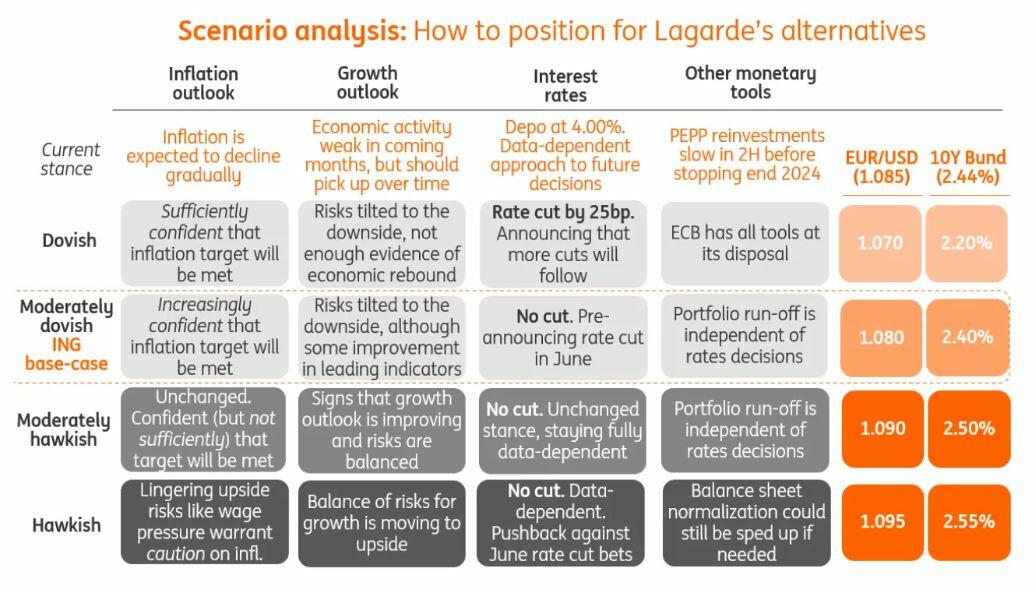

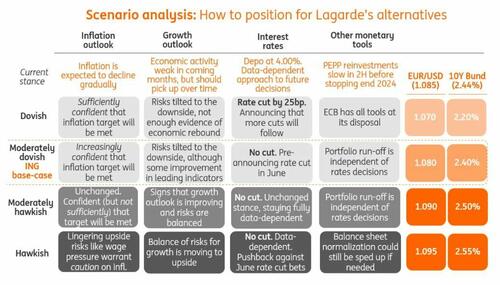

Finally, while the market is unlikely to move much due to the lack of surprises, here is the traditional market matrix reaction function courtesy of ING Economics.