The largest home improvement retailer in the US beat second-quarter earnings and sales expectations but lowered its comparable sales and profit forecasts for the year. This aligns with our ongoing theme of an emerging consumer slowdown.

Here's a quick look at Home Depot's second-quarter results (courtesy of Bloomberg):

-

Comparable sales -3.3% vs. -2% y/y, estimate -2.39%

-

US comparable sales -3.6% vs. -2% y/y, estimate -2.63%

-

Net sales $43.18 billion, +0.6% y/y, estimate $43.79 billion

-

Adjusted EPS $4.67, estimate $4.52

-

EPS $4.60 vs. $4.65 y/y

-

Customer transactions -1.8%

-

Average ticket sales $88.90, -1.3% y/y

-

Average ticket -1.3%

-

Sales per square foot -3.6%

-

Merchandise inventories $23.06 billion

-

Total location count 2,340, +0.6% y/y

-

SG&A expense $7.14 billion, +3.3% y/y

"During the quarter, higher interest rates and greater macro-economic uncertainty pressured consumer demand more broadly, resulting in weaker spend across home improvement projects," Home Depot CEO Ted Decker wrote in a statement.

The focus is on Home Depot's full-year outlook. It now expects comparable sales to decrease by 3% to 4% compared to the previous forecast of -1%. This is far worse than the average Wall Street estimate tracked by Bloomberg of -1.65%. It lowered earnings per share for the year to -2% to -4%, down from +1%.

Snapshot of the full-year forecast (courtesy of Bloomberg):

-

Sees comparable sales -3% to -4%, saw about -1%, estimate -1.65% (Bloomberg Consensus)

-

Sees sales +2.5% to +3.5%, saw about +1%

-

Sees operating margin 13.5% to 13.6%, saw about 14.1%

-

Sees EPS growth -2% to -4%, saw about +1%

-

Sees adjusted EPS growth -1% to -3%

Here is Goldman's reaction to earnings:

HD – Weak, As Expected. Will They Also Get a Pass Like Housing Peers?: We think a comp miss and FY comp sales cut was widely expected. It was always going to just be a matter of magnitude and whether or not the stock would get punished for it. Whether fair or not, most housing/big ticket exposed names who cut have acted pretty well on 2Q EPS day, despite many cutting 2H numbers. Ultimately, they did miss the mark slightly here on top-line for the quarter and the guide. Commentary on the call about whether they have seen further deterioration, or just still sluggish trends will be important to watch. Would expect some weakness to start, but expect the move in rates the next couple days to matter just as much for the stock as actual results, if other housing prints are any indication. They beat EPS, with upside from revenue and SG&A. Comps were -3.3% (US was -3.6%) vs Consensus -2.1% and we think the bogey was -3%. They took FY comps down to down 3-4%. They said -3% is where it will be if the demand holds where it is now into 2H. We think they bogey for the guide was down 2-3%.

In an interview with CNBC, CFO Richard McPhail said consumers have been undergoing a "deferral mindset" since the middle of 2023. The reason is straightforward: high mortgage rates have paralyzed the housing market, and elevated inflation and high interest rates, in general, have led households to pull back on spending.

McPhail said, "Pros tell us that, for the first time, their customers aren't just deferring because of higher financing costs," adding, "They're deferring because of a sense of greater uncertainty in the economy."

"What our customers tell their pros is, 'Everything I read tells me interest rates will be lower in three to six months,'" the exec said, explaining," 'Why would I borrow to finance the project now rather than just wait a few months?'"

Companies heavily exposed to consumers have posted weak results this earnings season and warned about consumer weakness.

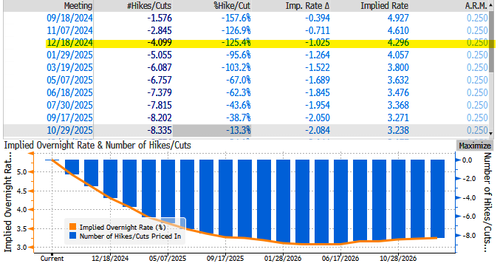

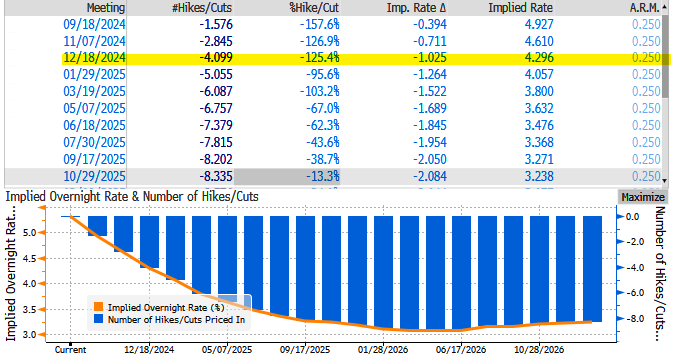

Rate traders are currently pricing in as many as four 25bps cuts by the end of the year. The labor market is cooling, and the economy is trending in the wrong direction.

Low/mid-tier consumers have been tapping out in the Biden-Harris economy, plagued with elevated inflation and high interest rates. Many of these folks have depleted savings and maxed out credit cards. The big question is whether lowering interest rates will create a soft economic landing, or if the Fed has already missed the mark.