Highlighting mixed consumer trends, discount retailer Five Below reported a smaller-than-expected decline in second-quarter comparable sales, beating analysts' projections tracked by Bloomberg. Although the company lowered its full-year comparable sales forecast, it still exceeded analysts' expectations.

Here's a snapshot of second-quarter results (courtesy of Bloomberg):

-

Net sales $830.1 million, +9.4% y/y, estimate $822 million

-

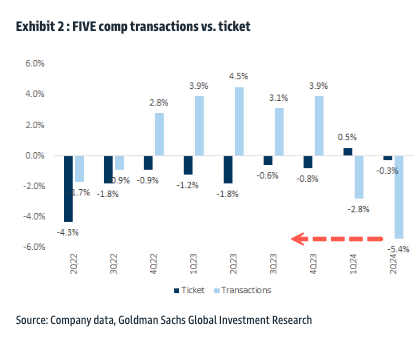

Comparable sales -5.7%, estimate -6.4%

-

EPS 60c vs. 84c y/y, estimate 54c

-

Total location count 1,667, +3.9% q/q, estimate 1,660

-

Stores opening 62, +55% y/y, estimate 60

Third quarter forecast:

-

Sees net sales $780 million to $800 million, estimate $790.2 million

-

Sees a mid-single-digit decrease in comparable sales

-

Sees adjusted EPS 10c to 22c, estimate 15c

-

Sees net loss $2 million to $13 million

Full-year forecast:

-

Sees net sales $3.73 billion to $3.80 billion, saw $3.79 billion to $3.87 billion, estimate $3.78 billion (Bloomberg Consensus)

-

Sees comparable sales about -5.5% to -4%, saw -5% to -3%, estimate -5.9%

-

Sees adjusted EPS $4.35 to $4.71, saw $5.00 to $5.40, estimate $4.75

-

Sees net income $220 million to $244 million

-

Sees gross capital expenditures about $335 million to $345 million

Commenting on Five Below's mixed earnings is Goldman's Kate McShane.

McShane noted that "declines in comp ticket during 2Q with lower units per transaction" only "suggests that FIVE's core customer remains pressured and is continuing to reduce discretionary spending, and that FIVE's assortment is not currently providing an attractive value to their customers."

"While we were encouraged to hear that traffic trends have improved quarter to date, conversion likely remains pressured as guidance implies that comp trends for 2H24 will be similar to 2Q's -5.7%," McShane said.

She continued, "We also note that FIVE continues to see diverging trends between income cohorts, with softer trends from lower-income households but stronger trends from higher-income households, suggesting at least some element of trade down is taking place. Although the implied trade-down trends are encouraging, we believe pressure on FIVE's lower-income customers will continue to weigh on conversion in the near term."