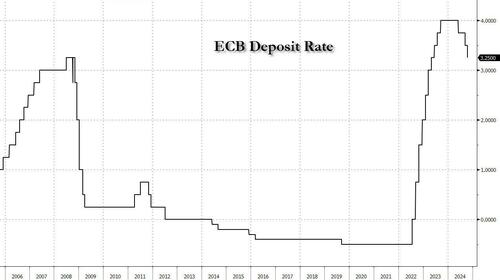

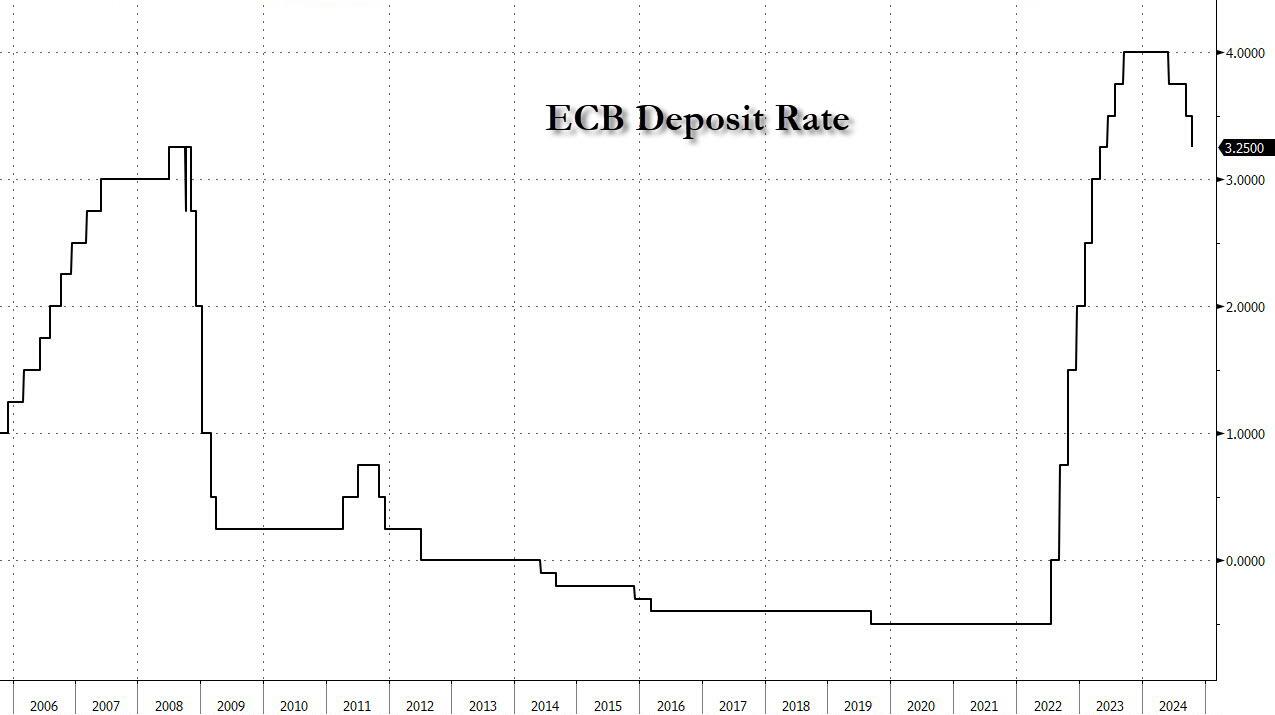

As expected by literally every economist, moments ago the ECB cut its three key rates by 25bps for the second consecutive meeting, in a show of support to the rapidly shrinking European economy and saying it did so because "incoming information on inflation shows that the disinflationary process is well on track" and adding that "the inflation outlook is also affected by recent downside surprises in indicators of economic activity. Meanwhile, financing conditions remain restrictive."

Specifically, the ECB cut its Marginal Lending Facility from 3.90% to 3.65%, the Refinancing rate from 3.65% to 3.40% and the Deposit Rate from 3.50% to 3.25%.

Some highlights from the statement:

Inflation

- Domestic inflation remains high, as wages are still rising at an elevated pace.

- Inflation is expected to rise in the coming months, before declining to target in the course of next year

- Disinflationary process is well on track

Labor Market

- At the same time, labour cost pressures are set to continue easing gradually, with profits partially buffering their impact on inflation.

Guidance:

- Will keep policy rates sufficiently restrictive for as long as necessary. The Governing Council is not pre-committing to a particular rate path, and data will determine level, duration of restriction

- ECB to Follow Data-Dependent, Meeting-by-Meeting Approach

- ECB to Keep Rates Sufficiently Restrictive as Long as Needed

Here is the comment on the unchanged guidance:

“The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. It will keep policy rates sufficiently restrictive for as long as necessary to achieve this aim. The Governing Council will continue to follow a data-dependent and meeting-by-meeting approach to determining the appropriate level and duration of restriction.”

Some have pointed out that the only real alteration to the statement’s wording is the line around inflation being at 2% in the course of 2025, as opposed to in H2-2025, potentially an acknowledgement of recent HICP progress, with this morning’s Final September Y/Y measure subject to a downward revision to 1.7%, though we await the presser for more clarity on the importance of the language change.

Commenting on the ECB, Bloomberg Intelligence European Equity Strategist Laurent Douillet said that there was “no surprise there,” adding that "a 50-bp cut at the next meeting in December is a possibility if the two inflation and PMI prints of October and November continue to surprise on the downside. With this rate cut and many more -- five by the end of next year -- already priced into European equities, the current earnings season is more likely to dominate market movements."

And indeed, as we wrote in our preview, there is virtually no reaction in the EURUSD, which moves very little after the report and was last seen at 1.0863 because the ECB did very much as expected.

As newsquawk notes, a 25bps cut was delivered and based on an "updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission' with the incoming inflation on inflation showing the disinflationary process is well on track".

From the upcoming press conference, we look for any signs that there was dissenting voices on the decision; interestingly, the continued inclusion of the line that it will 'keep policy rates sufficiently restrictive for as long as necessary..." could be seen as one for the hawks in order to appease them against the cut. Reminder, cutting at the October meeting is a departure from the guidance provided around September but very much in-fitting with communication more recently given the progress of inflation and soft growth outturns. Evidently, any disagreement on the board may be clearer from source reports that the Q&A itself.

Dissent insight aside, we are attentive to any guidance from Lagarde that goes beyond the data dependent" and meeting by meeting' approach.