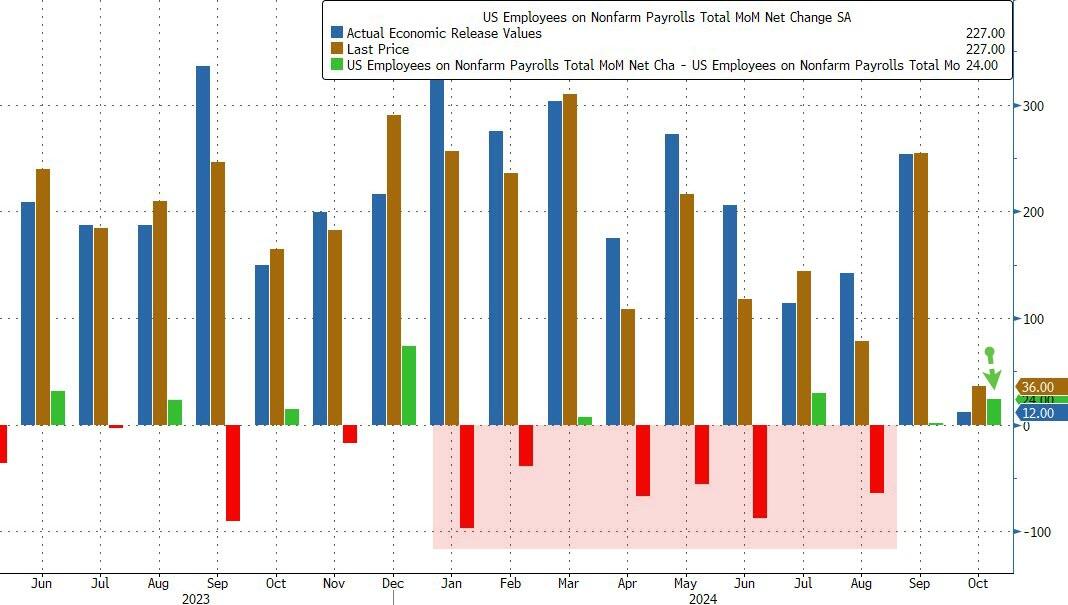

After the October hurricane-driven debacle which sent last month's payrolls print to the lowest in years, at just 12K, traders were expecting a solid bounce today, with many whispering a print that would come above the consensus estimate of 220K... and they were right: moments ago the BLS reported that in November, payrolls growth surged to 227K, the second highest print since March (after the upward September revision).

Unlike previous month, most of which had all seen downward revision, the previous two months were revised higher, September was revised up by 32,000, from +223,000 to +255,000, and the change for October was revised up by 24,000, from +12,000 to +36,000. With these revisions, employment in September and October combined is 56,000 higher than previously reported.

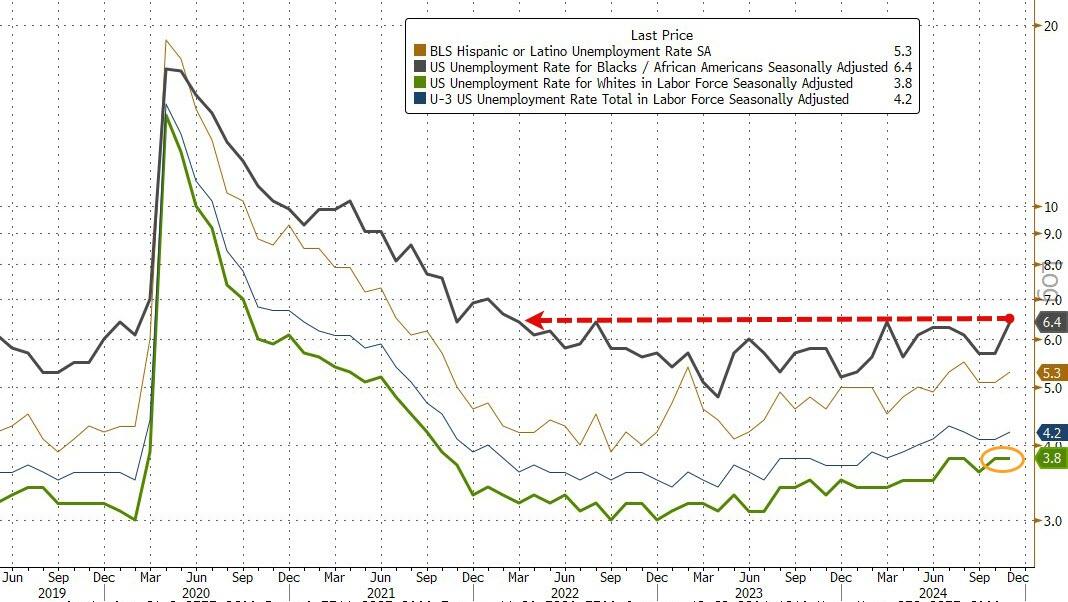

Those looking for a clear indication whether the Fed will keep cutting or halt its easing cycle in two weeks, will have to wait because the rest of the jobs report was mixed: on one hand, unemployment rose from 4.1% to 4.2%, and above the 4.1% estimate (with Black unemployment at 6.4% rising in November, while the jobless rates for adult men (3.9 percent), adult women (3.9 percent), teenagers (13.2 percent), Whites (3.8 percent), Asians (3.8 percent), and Hispanics (5.3 percent) showed little or no change over the month)...

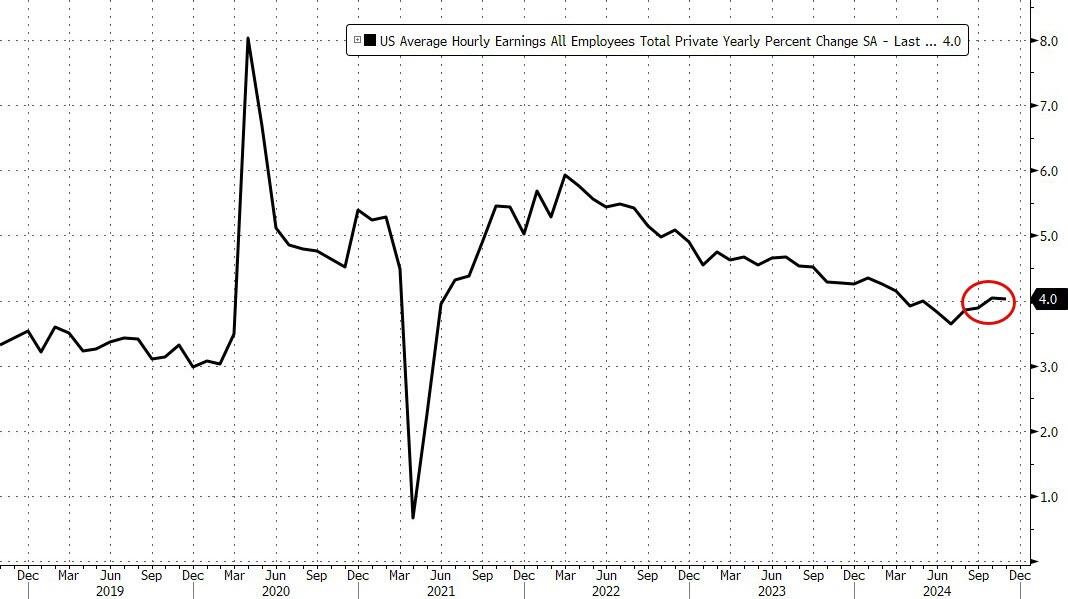

...but hourly earnings also rose, rising 0.4% MoM in November, above the 0.3% estimate, with annual wage growth flat at 4.0%, also above the 3.9% estimate, both indicating that wage growth pressures remain.

Developing.