Trade War Begins: Key Highlights

At exactly 12.01am ET this morning, the long-awaited 25% US tariffs on Canada and Mexico as well as an additional 10% levy on China went live. The 25% tariffs taking effect apply to all imports from Canada and Mexico, except for Canadian energy which will be tariffed at a 10% rate.

Canadian and Mexican tariffs were supposed to be the low odds given their potential for blow back onto US growth; according to JPMorgan today’s implementation should therefore raise odds that the plethora of other tariffs that are currently in the works – the 25% EU tariffs, sectoral tariffs on copper, lumber etc., as well as the broader suite of reciprocal tariffs – will be enacted and are more than just negotiating tactics.

Swift retaliation followed from both Canada and China. Canada imposed 25% tariffs of its own on $155bn of US exports including orange juice and bourbon in two stages – immediate tariffs on $30bn of goods and the remaining $125bn in 21 days.

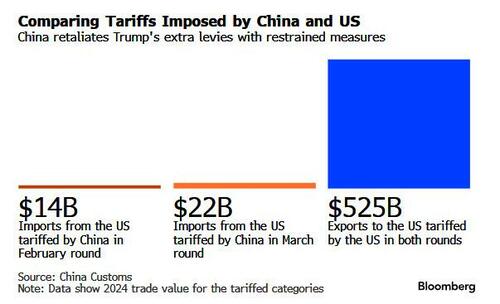

China raised tariffs by 10% on soybeans, pork, beef, and fruits starting March 10th, and 15% tariffs on chicken, wheat, corn and cotton in line with yesterday’s press reports of agricultural goods being Chinese tariff targets. 10 American companies involved in defense work have also been put on the entity list.

Additionally, China's Customs suspended imports of US lumber effective immediately, and suspended soybean import qualification for three US companies from Tuesday including CHS Inc (CHSCO), Louis Dreyfus Company, EGT (BG).

China's MOFCOM earlier stated that China will take countermeasures to firmly safeguard its rights and interests in response to US tariffs, while it urged the US to immediately withdraw its unilateral tariff measures, calling them unreasonable, groundless, harmful to others, and self-serving. Furthermore, it hopes the US will return to the right track of resolving differences through dialogue on an equal footing as soon as possible.

China released a white paper on controlling fentanyl-related substances, via Xinhua; China claims it fulfils its international anti-drug obligations and opposes acquisitions and shifting of responsibility. China also said it firmly upholds current international drug control system.

The Bloomberg chart below compares tariffs imposed by China and US - according to JPM, the tempered and targeting China reaction is keeping sentiment stable with China equities bouncing on today’s China announcement.

Mexico hasn’t made a formal retaliation announcement at the time of writing, but around the Feb 1 deadline Sheinbaum said they would impose “tariff and non-tariff measures in defense of Mexico’s interests” (with ‘sources’ suggesting 5%-20% tariffs on pork, cheese, fresh produce, steel, aluminium). The Blomberg chart below of Mex-US trade items where Mex is a net exporter to the US and could target these goods for tariffs (BBG):

According to JPM, the muted nature of the price action in markets in the wake of the news is somewhat surprising, given the gravity of the economic impact on Canada/Mexico in particular. One could argue that the stoic USD/CNH reaction is not entirely surprising given that any FX retaliation decisions will likely have to wait till the end of the NPC. For CAD, the lack of an immediate reaction could owe to the pre-existing risk premium in the likes of CAD, but defies ex-ante expectations of USD/CAD spiking above 1.50 in the event of actual implementation. According to JPMorgan there are three possible reasons to rationalize this price action:

Markets do not view these tariffs as permanent, and the two-tier nature of the Canadian retaliation with the lumpy second batch not due till another three weeks hints at the possibility (hope?) of de-escalation in the not-too-distant future.

Retaliation itself could be changing the nature of the USD’s reaction function; in theory, symmetric retaliation to tariffs in a balanced trade set-up should not require any currency adjustment; and

Anticipation of blow back of CA/MX retaliation hurting US growth further promotes the emerging narrative of cracks in US exceptionalism, and markets could also be discounting some likelihood of this US growth cost accelerating the timetable for an eventual negotiated settlement.

According to Goldman (full note here for pro subscribers), the 10% hike in the China-focused tariffs will raise the US effective tariff rate by 1.2%, and increase core prices by around 0.1%.

This will bring the average effective tariff rate on imports from China to roughly 34%, and represents a rise in the tariff rate on Chinese imports roughly twice as large as the increase over the entire first Trump administration.

A 25% tariff on Canada and Mexico (10% on Canadian energy) would raise the effective tariff rate by 5.7pp, and core prices by around 0.6%.

FX Flows

In USDCAD we're seeing a solid USD selling bias, coming from both HFs and Real Money and we believe largely cutting USD longs with the lack of momentum higher here, local RM USD selling, and a view that tariffs won't stay on permanently.

In EURUSD there is decent two-way with some interest to Sell EURs the 1.0520-1.0530 multi-top that has been a good tactic in recent weeks; as well as cutting of bits of recently re-initiated Short EURUSD positioning. That multi-top very much the focus right now... Goldman's inclination is that today might be the day it goes.

Why Isn’t the USD Rallying?

A few quick thoughts across Goldman's Sales, trading, Rsrch

There remains a meaningful amount of doubt about whether the Canada & Mexico tariffs will truly be in effect for any meaningful amount of time.

China’s restrained response and FX stability are a big inhibitor to a broader DXY reaction. That’s unlikely to change through the Two Sessions (ongoing now); and there’s an argument—to which Sun Lu (GS Strats) subscribes—that China is still trying to keep its response moderate and prioritise the domestic rebound. The RMB vs. the CFETS basket has weakened YTD, and RMB REER is near multi-year lows given inflation differentials (i.e. little ‘pressure’ to weaken RMB).

Trump’s comments in last night’s press conf. about countries gaining an unfair advantage by weakening their currencies, specifically referencing China & Japan as examples (BBG/White House).

Non-US end asset owners (Pension, Insurance etc.) have been increasing hedge ratios in recent weeks on their US assets (partic. the case for Cadandian & Swedish Real Money), making some large USD selling flows.

US assets are taking a hit from US data implying a real sentiment and activity impact from tariffs on the US economy. Yesterday’s ISM Manufacturing included 20 mentions of tariffs in the press release (vs. 4 in January release). The USD’s beta to SPX and SPX’s beta to tariff headlines have gone up.

Tariffs are no longer the #1 theme – focus is now on European fiscal, the end of US exceptionalism, broadening of the ‘AI trade’ to China and China policymakers softening their tone on business etc.., which all cut against the USD.

Digging into some of the individual crosses, Goldman's Kristian Brauten-Smith notes:

EURUSD a star performer on the session: month-beginning flows clearly skewed towards USD-selling in the majors, buts what is notable is the lack of interest from our franchise to buy USDs on tariff delivery in Canada/Mexico/China. It leaves EURUSD within striking distance of the 1.0525/35 multi-top on the year, and the market is drawing parallels to 2020 and EU COVID fiscal delivery putting a floor under EURUSD. It remains to be seen whether defence spending jump starts a struggling manufacturing sector in the medium-to-long term, but just the thought of it is dissuading EURUSD supply close to 1.05. Through 1.0535 and 1.0600/30 becomes critical – highs in December, breakdown level set back in June 2024 on French political noise.

GBPUSD likewise trades well with the long-end of G10 rate curves still well anchored. The 200 DMA and December highs up into 1.2785/2811 are critical for the next week, and a break there would coincide with EURUSDs own break of 1.0535/50 – talk of DXY breakdown probably dominates were we to trade there.

USDCAD continues to see better selling from domestic RM as has been the case for the last 3-4 months now. It doesn’t feel as though Fast Money will overpower this supply, and means USDCAD is probably back being a lower beta Dollar, even were the greenback to regain a footing in the coming sessions.

Bottom Line:

The market is struggling to richen the USD when it is simultaneously marking-down US nominal growth. Our US economist’s view is that we’ve gotten excessively negative on the US data misses recently, but, it seems the market needs more confidence in that part of the equation before we can see any reversion to Tariffs Up--USD Up price-action.

Delta 1 take (From Goldman Delta One head Rich Privorotsky)

Few ppl think Canadian and Mexican tariffs (especially at 25%) will be a lasting feature. Think the real angle is getting allies to impose 20%+ tariffs on China (https://www.cnbc.com/2025/03/01/treasury-chief-urges-canada-mexico-to-m…) and so we’ll be on watch out for later in the week to see if this leg of the policy abruptly reverses (the China tariffs are here to stay imo).

Yesterday I was inundated with calls from US clients asking if they had missed the European rally (in absolute terms maybe yes). The double digit leap in defense stocks and the broader move higher in the geography is quite simply a reflection of the increase in fiscal space. The decision overnight of the US to cut financing to Ukraine will only accelerate that debate (expect another higher start in defense). Think we’ve gotten a bit ahead of ourselves in terms of size and scope. Many broad based spending initiatives or new funds will need unanimous support across all European nations (a high bar especially given Hungary and Slovakia ). That said, the case for European outperformance remains as long as the US continues to be a relatively poor destination for forward returns (Mag 7 capex machine instead of buyback machine...NVDA broke DeepSeek lows and crypto can't hold a rally).

Atlanta Fed GDPnow has hit an extreme low of -2.8%. Surely exaggerated in terms of degree, but directionality likely correct. US equity sentiment feels low/extreme but I'm not sure positioning reflects that. Bracing myself for an adversarial Trump at the State of the Union tonight…think any hope on tariff reversal won’t come until Wednesday. Watching Target and Best Buy on consumer.

Side-note: Polymarket summarizes the mood out there (https://polymarket.com/event/us-recession-in-2025)”

Developing

Loading...