It's deja vu all over again.

With bank earnings season coming to a rapid close, this morning we got results of the last 2 of the "Big 5", when Bank of America and Citigroup both reported Q1 earnings, and we doubt it will surprise anyone that the pattern observed over the past few days remained the same: blowout equity trading revenues, offset by disappointing FICC, and slowing Investment banking advisory and underwriting.

Taking a closer look at the bigger of the two, Bank of America joined JPM, Goldman and MS in posting record equity trading revenues as the bank reaped the benefits of soaring volatility and net interest income topped analysts’ estimates.

Revenue from equity trading rose 17% to $2.18 billion in the first three months of the year, helping the bank beat analysts’ estimates for per-share earnings. Meanwhile, trading of FICC (fixed income, currencies and commodities) missed estimates, bringing in $3.46 billion, below the $3.47 billion estimate.

BofA's sales and trading unit delivered its 12th consecutive quarter of year-over-year revenue growth, CEO Brian Moynihan said in the statement. “Our business clients have been performing well, and consumers have shown resilience, continuing to spend and maintaining healthy credit quality.”

Let's take a closer look at the bigger picture: here is what BofA reported for Q1.

- EPS $0.90, up 18% from the 76c a year ago and beating estimates of $0.82

- Revenue net of interest expense $27.4BN, up 12% YoY from $25.8BN and beating estimates of $27.1BN. This was the highest total revenue in more than a decade

- Trading revenue excluding DVA $5.65 billion, beating estimates of $5.55 billion

- Equities trading revenue ex DVA $2.18 billion, beating estimates of $2.06 billion

- FICC trading revenue ex DVA $3.46 billion, missing estimates of $3.47 billion

- Investment banking revenue $1.52 billion, missisng estimates of $1.55 billion

- Debt underwriting rev. $942 million, beating estimates $856.4 million

- Equity underwriting rev. $272 million, missing estimates of $324.8 million

- Advisory fees $384 million, beating estimates of $421.1 million

- Trading revenue excluding DVA $5.65 billion, beating estimates of $5.55 billion

- Net interest income $14.44 billion, beating estimate $14.36 billion

- Net interest income FTE $14.59 billion, estimate $14.57 billion

- Wealth & investment management total revenue $6.02 billion, estimate $6 billion

- Revenue net of interest expense $27.37 billion, estimate $25.78 billion

- Non-interest expenses $17.77 billion, estimate $17.62 billion

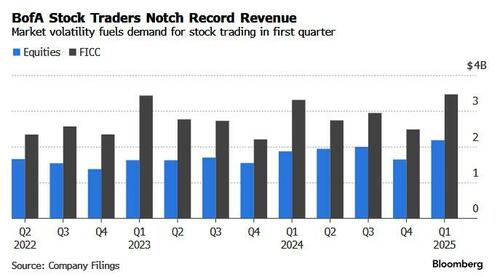

And visually:

Summary highlights from Q1 below:

Net interest income was $14.6 billion, translating into a Net Interest yield which rose from 1.97% to 1.99% QoQ and was unchanged YoY, it also came in below estimates of 2%. The bank's blended cash and securities yield was 3.23% vs. total deposit rate paid of 1.79%. Some more details on these numbers:

- NII increased $0.1B from 4Q24, driven by lower deposit costs, higher NII related to Global Markets (GM) activity, and fixed-rate asset repricing, partially offset by the impact of lower interest rates and ~($250MM) from two fewer days of interest accrual

- Increased $0.4B from 1Q24, as lower deposit costs, higher NII related to GM activity, and fixed-rate asset repricing more than offset the impact of lower interest rates and ~($125MM) from one less day of interest accrual

The bank's provisions matched net charge-offs at the bank, which remained flat, Chief Financial Officer Alastair Borthwick said on a conference call with reporters.

“Employment is obviously healthy, and consumers have proven resilient,” Borthwick said. “The spending across channels and the credit quality of our loan portfolio remains solid.”

Perhaps the most notable number in this context was the bank's net interest income outlook, specifically the bridge from the current $14.6BN number to the projected year-end number (which was left unchanged from last quarter) of $15.5-$15.7BN: here we find that BofA now officially budgets for 4 rate cuts this year: in May, July, Sept and Dec, which is somewhat at odds with BofA's view for no recession this year.

BofA's balance sheet, liquidity and capital were in line to somewhat stronger vs expectations:

- Basel III common equity Tier 1 ratio fully phased-in, advanced approach 13.3%, estimate 13.5%

- Standardized CET1 ratio 11.8%, estimate 11.8%

- Return on average equity 10.4%, estimate 9.37%

- Return on average assets 0.89%, estimate 0.82%

- Return on average tangible common equity 13.9%, estimate 12.6%

Unlike JPMorgan, BofA did not report a spike in its loan loss reserve build, and instead its provision for credit losses was $1.45 billion (a 0.54% charge off ratio), unchanged QoQ and WoW, and below the estimate of $1.53 billion.

There were no surprises in the bank's deposit and loan trends:

- Loans $1.11 trillion, up 5.9% YoY and above the estimate $1.1 trillion

- Total deposits $1.99 trillion, also above the estimate $1.97 trillion

Turning to the expense side, total non-interest expenses rose 3.1% from a year earlier to $17.8 billion. Analysts had expected a 2.3% increase to $17.6 billion. Compensation expenses $10.89 billion, up $0.7bn QoQ and YoY, and above the estimate $10.84 billion; BofA's efficiency ratio dropped to 64.93% vs 66.77% y/y.

Looking at the most important aspect of today's report, the bank's Global Markets segment, here we find the abovementioned continuation of the already noted pattern: strong equity trading, mediocre everything else, to wit:

- Trading revenue excluding DVA $5.65 billion, beating estimates of $5.55 billion,

- Equities trading revenue excluding DVA up17% to $2.18 billion, beating estimates of $2.06 billion; "driven by improved trading performance and increased client activity"

- FICC trading revenue up 8% excluding DVA $3.46 billion, missing estimates of $3.47 billion, "driven by strong performance in macro products5 and continued strength in credit products"

- Investment banking revenue $1.52 billion, missisng estimates of $1.55 billion

- Debt underwriting rev. $942 million, beating estimates $856.4 million

- Equity underwriting rev. $272 million, missing estimates of $324.8 million

- Advisory fees $384 million, beating estimates of $421.1 million

Noninterest expense for the division rose 9% to $3.8BN, driven by higher revenue-related expenses and investments in the business, including people and technology

Of note, the average VaR for Markets soared from 64 a year ago and 68 in Q4 to a whopping 91 in Q1.

Wall Street commentary on BofA's earnings was generally upbeat:

Piper Sandler’s Scott Siefers

- Positive that 4Q25E net interest income expectations reiterated

- Strong quarter, fees and credit costs the main drivers

- Net interest income topped expectations, though expenses a touch higher than expected

UBS’s Erika Najarian

- “This print was much anticipated, and we think this should be ‘enough’ to bring some momentum back into the stock,” analysts led by Najarian wrote in a note

- “Net-net, results should be more than good enough, but the call is likely critical for more sustained outperformance — to note, we think this is a crowd favorite among money centers coming into earnings”

Citi’s Keith Horowitz

- Pre-provision net revenue beat Citi estimates, particularly strong in equities and net interest income; credit trends solid

- Truist’s John McDonald

- Result came in ahead of consensus driven by beats on provision and fees

- “Most importantly, BAC maintained its prior guidance for NII to increase throughout 2025 and finish 4Q25 at ~$15.5-$15.7b, even while now incorporating 4 Fed cuts of 25bps each into the guide”

Baird’s David George

- “Core pre-provision net revenue better than expected given fee upside in trading, credit holding up well,” the analysts wrote

- Fee income up about 18% quarter on quarter above expectations from strong markets activity, similar to universal peers

KBW’s David Konrad

- Stock should react favorably, trading at a 20% discount to peers

- Result largely as expected; equities strong

Shares of Bank of America, rose 4% to $38.12 in early trading. They’ve gained 5% in the 12 months through Monday, less than the 18% increase in the S&P 500 Financials Index.

BofA's Q1 investor presentation is below (pdf link)

Loading...