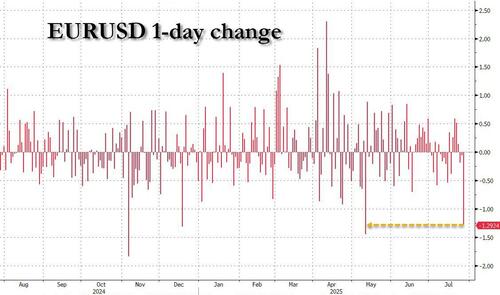

The announcement of a US-EU trade deal was supposed to send the euro soaring; instead the common currency suffered its steepest one-day drop against the dollar since May as Germany and France voiced fears that the long-awaited EU-US trade deal would hurt the European economy.

The euro was down more than 1% against the dollar and weakened by 0.8 per cent against the pound, following the announcement on Sunday that the US would impose 15% tariffs on most imports from the EU.

The agreement, hailed by European Commission president Ursula von der Leyen as “the biggest trade deal ever” and covering nearly 44% of global GDP, averted a possible transatlantic trade war. But as reported earlier, German Chancellor Friedrich Merz said on Monday that the tariffs would cause “considerable damage” to his country’s economy, Europe and the US itself.

“Not only will there be a higher inflation rate, but it will also affect transatlantic trade overall,” he said. “This result cannot satisfy us. But it was the best result achievable in a given situation.”

French Prime Minister François Bayrou was even more dramatic, and said the trade deal marked a “dark day”, adding that the EU had “resigned itself into submission”.

European stocks relinquished earlier gains as the initial relief that a deal had been struck was replaced by concern over its impact on the Eurozone economy.

Germany’s Dax closed 1.1% lower while France’s Cac 40 gave up 0.4%. Tariff-exposed car industry stocks on the region-wide Stoxx Europe 600 fell 1.8 per cent, having risen by a similar amount at the opening of trade on Monday.

That said, the euro still has a long way to fall: the currency remains 12% higher against the dollar for the year, boosted by Germany’s defence spending plans as well as broader investor hopes that President Donald Trump’s America First policies will encourage a wave of economic stimulus in the Eurozone.

Sunday’s deal secured a lower tariff rate for the EU than the 30% that the US president had threatened to impose from August 1.

But the duties still mark a threefold increase from the average tariffs imposed on the bloc by the US before Trump’s “liberation day” announcements in April. The industry body for EU steel producers said a 15% American tariff on most imports from the bloc would add a “huge burden” on its members.

Meanwhile on the other side of the Atlantic, the US Chamber of Commerce welcomed the deal, saying that it “provides relief” to businesses. But it added that the 15% tariff rate “still marks a significant increase in the cost of trading” and that more sectors should be included in the agreement’s zero-for-zero tariff list.

The White House said the deal “achieves historic structural reforms and strategic commitments that will benefit American industry, workers, and national security for generations”.

As Europe’s leaders reacted to the agreement, Spain’s socialist Prime Minister Pedro Sánchez said he supported it “but without any enthusiasm”.

Conservative parties in France and Germany were more vocal, and argued that the deal exposed the weakness of the bloc. Alice Weidel, co-leader of Germany’s Alternative for Germany party, posted on X that it was “not an agreement, but a slap in the face to European consumers and producers!

Elsewhere, speaking in Scotland on Monday, Trump said he planned to set a tariff rate of up to 20 per cent “for essentially the rest of the world”, referring to countries that do not strike specific trade agreements with the US. He added that he planned to announce pharmaceutical tariffs “in the near future”.

Loading recommendations...