Submitted by QTR's Fringe Finance

Make no doubt about it: I am far more of a skeptic, a cynic, and a bear than most of the lobotomized market participants, analysts, and financial-news anchors wandering around the financial landscape like sedated Grand Theft Auto NPCs.

Not only have I personally researched innumerable demonstrable frauds (think about what your mindset would be after analyzing companies akin to Enron and Madoff every single week for 10 years) and heard every bullshit narrative and excuse in the book firsthand while working as a professional short seller, but there’s also the other slight doubt of believing that the entire macroeconomy is nothing more than a giant Ponzi scheme dressed up in television makeup.

I get labeled a “perma-bear,” a “doomsday sayer,” or someone peddling “fear porn,” but that’s not what I’m doing. I’m simply trying to identify trends objectively using fundamentals—a once-respected analytical tool now relegated to the catacombs of equity analysis. Think Cask of Amontillado: Benjamin Graham as Fortunato, while Michael Saylor and Tom Lee brick him in and leave him for dead.

The main problem, as I see it from deep within my own echo chamber, is that the inconvenient conclusions I reach about certain sectors or companies tend to ruffle the feathers of the 80% of today’s market participants who happily attribute grotesquely overvalued stocks to things like “animal spirits,” “seasonality,” or my personal favorite, “the Santa Claus rally.”

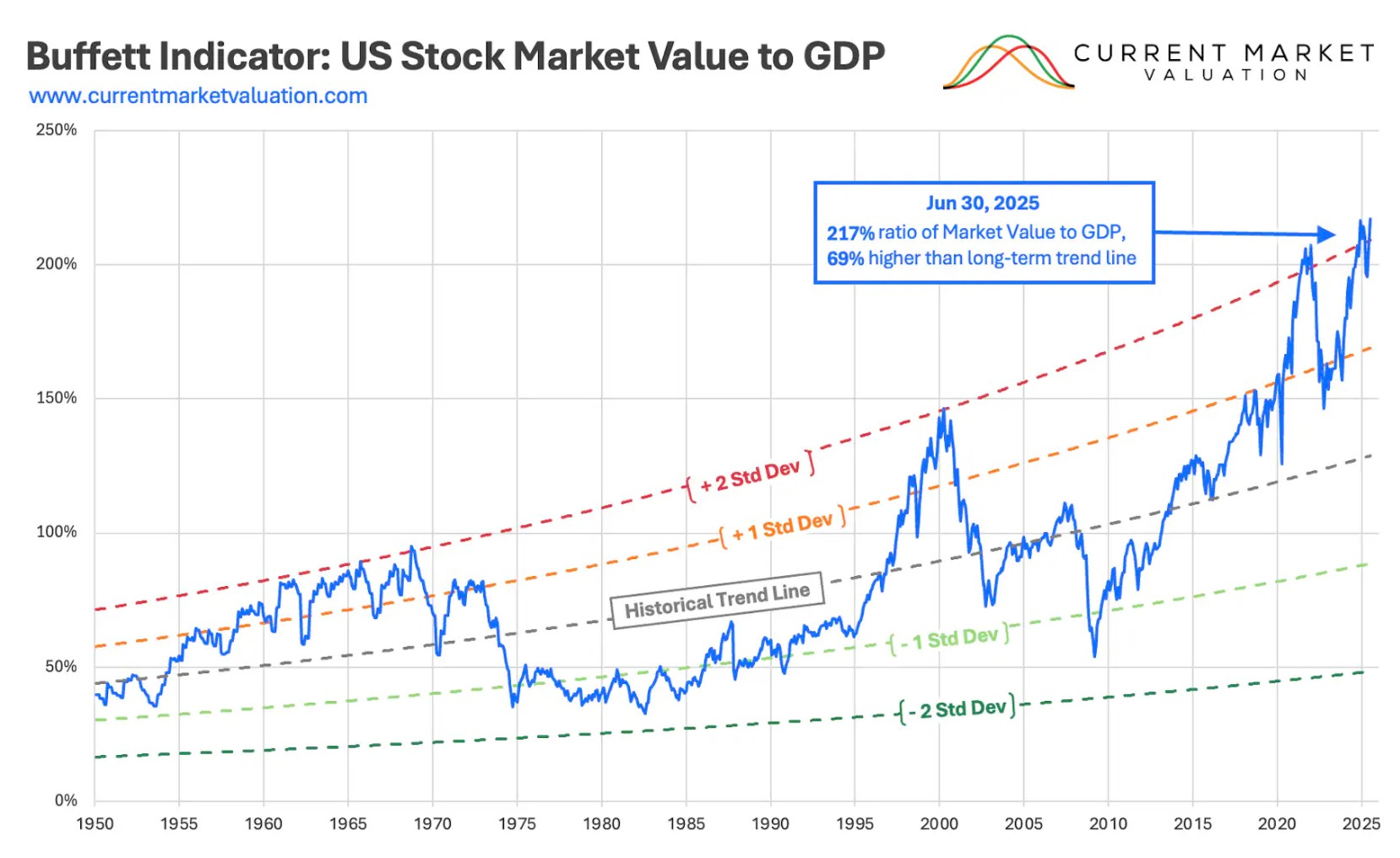

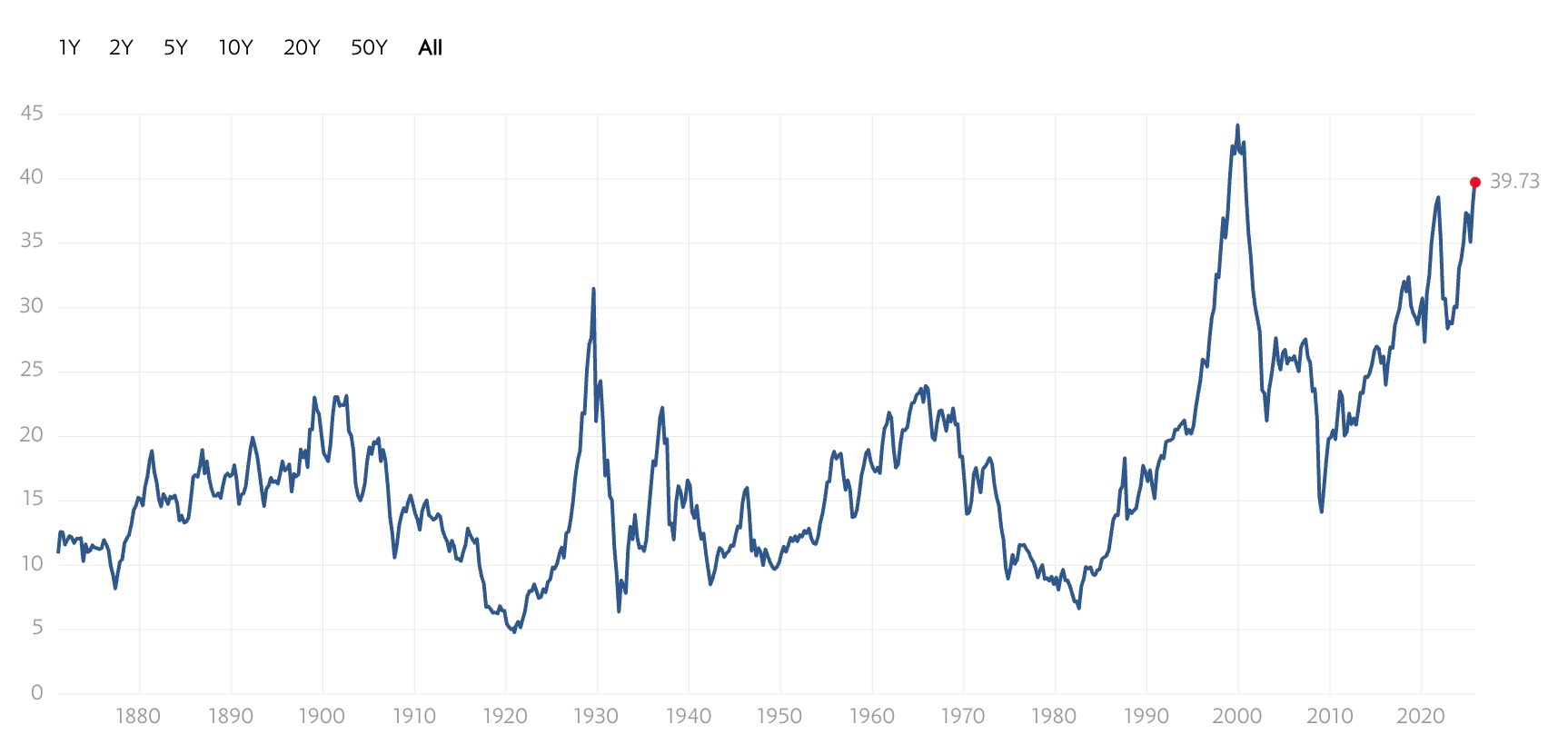

These terms are tossed around as if they’re divine revelations of why buying stocks at 39x P/E ratios finally makes them cheap after all these years. But instead, these gimmicks are really just lazy, backfitted explanations slapped onto whatever direction the market happened to move that day (spoiler alert: up). Bulls can get away with this nonsense endlessly, but bears get labeled anti-American miscreants for pointing out simple math. For example: “Hello, my name is Chris. Has anyone noticed the stock market to GDP indicator is at all time highs?”

Which begets the only acceptable response in today’s market: “Stone him!”

Yes, why bother with pedestrian concepts like the health of the consumer or the valuation of an index when you can just buy deep out-of-the-money calls on a cash-burning SPAC and turn $10,000 into $1 million because some guy on Reddit said “YOLO”? As I said yesterday in my column about Michael Burry shutting down his fund, the stock market today is basically a giant checkout-counter rack of scratch-off lottery tickets. “Investing” is just scratching the surface with a quarter and praying.

Many of my readers found me during COVID because I was early in saying the pandemic would have a profoundly negative effect on markets. Ultimately, that turned out to be true—though not as fast as I thought—and the crash culminated during Bill Ackman’s “Hell is coming” moment on CNBC. Shortly afterward, I became bullish on a number of equities, including financials and certain consumer staples. That wasn’t an accident—I wrote about it extensively.

By March 13, 2020, with the VIX at over 50, I start talking about stocks like Wal-Mart and Target. By July 2020, with the Dow at 26,870, I started predicting the Dow over 40,000 and talking about financial stocks I was buying due to their low price/book ratios. With Goldman at $216 (now $805) and JP Morgan at $98 (now $309), I told Jon Najarian on a podcast:

“I actually own J.P. Morgan, I think it’s cheap on a price/book valuation. I think all the banks are going to come back. I think any losses that banks incurred to their share price as a result of coronavirus will eventually all be bought back. Because this is a financial problem to some degree, but it’s not a systemic financial problem. And you have the Fed providing unlimited liquidity and an unlimited backstop to the banks. So if you’re buying the banks now, you’re pretty much buying the Federal Reserve. Companies like JPM and GS are not, in my opinion, don’t pose any type of systemic risk. Those financial names are ones I like to buy on the dips. The sector is still off like 25% to 30% this year. I think they are being overlooked, it’s not like hospitality where there’s going to be real pain going forward.”

“I like the banks! I love the names like GS and JPM. As much as I hate the system, those entities are as close to a bet on the Death Star as you can get.”

And then the coup de grace — so you can tell people that one time you saw QTR was bullish on the overall stock market — I told Jon:

“I do think the market could go higher from here and I wouldn’t mind owning an equal weight S&P ETF here. And I hate hearing myself saying that, but that’s the truth”

The point is I have nothing against being bullish. If you believe the Fed will continue its gnarly inflation experiment—trying to inflate away the national debt while monetizing every market dislocation with QE—it’s difficult not to be bullish on the nominal price of equities over the long run. And even recently, while raising concerns about regional banks, private credit, and subprime consumer lending, my thesis has been that we’ll see a sharp deleveraging followed by some form of bailout, with the Fed stepping into the bond market one way or another.

So no, I’m not allergic to bullishness. What I am allergic to is screaming “just buy index funds” at all times—especially when those funds are disproportionately weighted toward the Mag Seven, all trading at valuation levels that require oxygen masks.

Howard Marks pointed out recently that investors who buy at the top usually underperform over the next decade. “Reality is recognizing where things stand,” he says in a recent interview. “The higher P/E ratio you pay, the lower return you should expect.”

“When you buy the S&P 500 at a 23x P/E, your 10-yr annualized return has always fallen between +2% and –2%, in every case, every case,” he concludes.

And Warren Buffett has shown that you don’t need to be short to avoid these traps, you can simply sit in cash instead of elbowing your way into the euphoria.

And so, as I begin compiling my “26 Stocks I’m Watching for 2026,” I’m keeping that perspective in mind. I’ve never had trouble finding niche pockets of the market that present genuine opportunities, regardless of macro valuations. But you’re not likely to see me evangelizing index ETFs heading into a year where the Shiller PE is basically at 39x. That’s not analysis—that’s delusion.

Don’t confuse the fact that the market hasn’t given us a “cheap” S&P 500 in years with the idea that I’ll never be bullish on the overall market again. I simply think we need a meaningful reversion to the mean first.

Right now, there’s no doubt the U.S. economy is undergoing an enormous and seismic shift. Yes, the consumer is shitting the bed, but there’s something bigger at play that’s hard to ignore when you look at the price of gold.

I’ve seen theories ranging from “they’re weakening the dollar to bring manufacturing back to the U.S.” to “the dollar is dead and gold is exposing the corpse,” to “the BRICS will switch to a gold-backed currency and dump Treasuries,” to “stablecoins are about to become the primary buyers of U.S. debt.” I don’t know which of these scenarios is most likely. All I know is that the price of gold—now making a generational move higher—is signaling that we’re accelerating toward some kind of monetary breaking point.

So when Scott Bessent laughed off a question about gold a couple of weeks ago on a televised panel and attributed its rise to “more buyers than sellers,” it was one of the biggest tells I’ve ever seen.

If you’re trying to downplay something, you don’t write it off in 3 seconds and say literally nothing. A more subtle response and a bit more of a limited hangout would have shown some more finesse. By being so flippant, he made it obvious to me that he could know there are tectonic shifts happening beneath the surface of the U.S. economy.

With that playing out—and with equities still aggressively valued by nearly every metric you can slap on them, from P/E to the Buffett Indicator—forgive me if I’m not extremely bullish. I still believe, as I’ve written for years, that the massive deterioration, waste, and malinvestment in private credit, commercial real estate, regional banking, subprime lending, AI mania, and of course crypto all need to be purged before markets can find a real bottom. Yes, some of my warnings have seemed early. But “early” is usually just code for “right, eventually,” and it finally looks like the chickens are taking the off-ramp back to the coop.

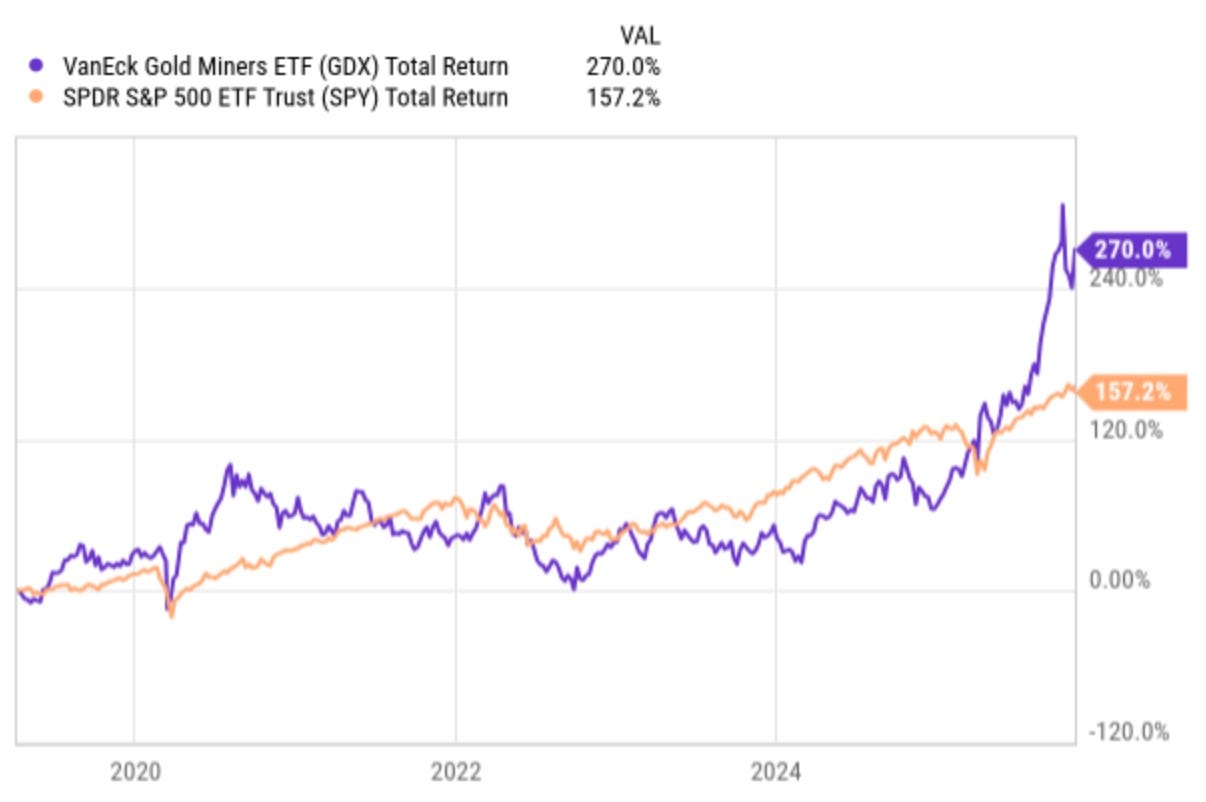

Back in April 2019, a CNBC anchor wrote that perma-bears were “ridiculous people”. Since then, the total return on gold mining stocks is 270% versus the S&P 500 at 157.2%. Sure, in some respects Josh was right because shorting the S&P outright at that time would’ve been a loser—but stepping away from U.S. equities and into gold miners, for example, would have been a winner.

Today, a large chunk of my capital remains in gold and silver miners, and it will continue to— even if they experience a drawdown during a broad market selloff. But there will come a day when I’m bullish on equities again — when the market becomes so cheap it’s impossible to ignore. I don’t know if that will happen during this deleveraging cycle or if the Fed will panic and short-circuit the whole thing. Maybe we’ll wait five months; maybe five decades. Modern monetary policy has made actual forecasting about as reliable as a Magic 8-Ball.

But when the day comes, you guys will be the first to know.

For my thoughts on where the ugly parts of the market are right now, read:

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Loading recommendations...