At the start of the week, commenting on Black Friday sales figures, Goldman analyst Natasha de la Grense said there has been increased focus on the "K-shaped" economy. As outlined in our previous notes (here and here), this widening behavioral gap is becoming more pronounced among working-poor and high-income households.

New data from Goldman analyst Ronnie Walker highlights the widening divide among consumers. He noted that lower-income households are weakening noticeably beneath the surface of otherwise solid aggregate retail trends.

Walker pointed out that while overall sales growth and earnings-call sentiment look solid, retailers serving lower-income zip codes report negative consumer sentiment and barely any nominal same-store-sales growth (0.2% vs. 2.5% for middle- and higher-income areas).

He said this gap reflects constrained borrowing capacity, softer income gains, and reduced immigration flows, adding that 2026 forecasts only suggest continued underperformance in low-end spending as slow job growth and cuts to SNAP and Medicaid under the OBBBA further pressure lower-income households.

Walker explains more in the note:

A Bifurcated Consumer Outlook

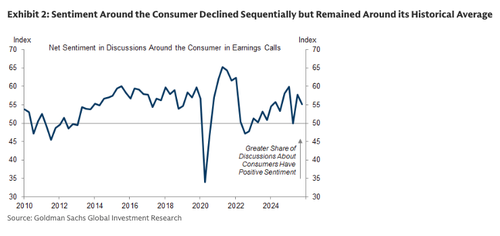

Company commentary and results suggest that the consumer remained healthy in the third quarter. Sales growth among consumer-facing companies improved — sales growth increased by 2pp to +6% year-over-year for the median S&P 500 consumer discretionary company and by 1pp to +1% for the median consumer staples company — while our quantitative measure of sentiment around the consumer on earnings calls declined sequentially but remained around its historical average.

Investors have raised fresh concerns about the health of the lower-income consumer this earnings season. Leveraging our Data Works team's estimates of the median household income of each retailer's store locations, we find that the healthy aggregate trends mask divergences between companies that face lower- and higher-income consumers. The left panel of Exhibit 3 shows that sentiment around the consumer on earnings calls turned negative on net for retailers whose stores are generally located in lower-income zip codes (diffusion index of 45 in 2025Q3 vs. 67 for companies in middle-to-higher income zip codes). Additionally, the right panel of Exhibit 3 shows that nominal same-store sales for that same group of companies have grown only 0.2% on average over the last year (vs. 2.5% for companies exposed to middle- and higher-income zip codes).

Weaker sales growth among companies with greater exposure to lower-income consumers has likely reflected a combination of headwinds to lower-income consumers — that we noted last year include more limited borrowing capacity and underperforming income growth — and the slowdown in immigration. Looking ahead, we continue to expect weak income growth to weigh on low-income spending. Exhibit 4 shows our distributional income growth forecasts: while we expect positive real income growth for all income cohorts in 2026, we again expect underperformance for the bottom income quintile, reflecting tepid job growth and cuts to Medicaid and SNAP benefits.

Despite Walker's gloomy view, this is quite the opposite forecast from Treasury Secretary Scott Bessent.

"In 2026, we are going to see very substantial tax refunds in the first quarter... We're going to see real wage increases. I think next year is going to be a fantastic year," Bessent told President Trump during the cabinet meeting earlier today.

Loading recommendations...