It was the polar opposite to yesterday's slop.

After a mediocre 3Y, and a dismal 10Y auction yesterday, moments ago the Treasury concluded the sale of the week's final refunding auction, when it unloaded $25BN in 30Y paper to seemingly endless demand.

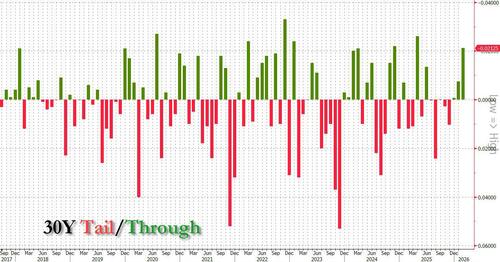

The auction stopped at a high yield of 4.750%, down from 4.825% in January, and the lowest since November. It also stopped through the 4.771% When Issued by 2.1bps, the biggest stop since LIberation Day in April 2025.

The bid to cover was 2.662, up sharply from 2.418 and the highest since January 2018! An oddity today is that the Fed's SOMA tendered for, and accepted, a whopping $7.1 billion, a continuation of yesterday's massive retention when the SOMA ended up with over $11BN of the 10Y.

The internals were also stellar, with Indirects taking down 69.94%, up from 66.77% and the highest since November. And with Directs rising to 24.18% (if not a record high, unlike this week's 3Y auction), Dealers were left with just 5.88%, down from 11.95% last month, and the lowest on record.

Overall, this was a stellar 30Y auction, one of the strongest on record, and clearly an indication that nobody is afraid that tomorrow's delayed CPI may come in overly hot.

Loading recommendations...