The data center investment macro story centers on hyperscalers such as Microsoft, Alphabet, Meta, and Amazon Web Services, whose massive cloud computing services are becoming the backbone for AI workloads, including ChatGPT and others. However, as we've previously noted, the data center buildout has run into supply-chain snarls, including memory chip shortages, power-grid constraints, and even a shortage of turbine blades for natural-gas generators.

The data center boom powering the AI revolution is certaintly impressive to watch unfold, but it won't be a straight line from here as the US attempts to hold the number one spot in the global AI race. Challenges are mounting, and the latest coverage on this comes from a conversation Goldman analyst Brian Singer had with Mark Monroe, a former principal engineer in Microsoft's Datacenter Advanced Development Group, who warned that data center buildouts face three major headwinds.

Here's a recap of the conversation between Singer and Monroe, which focused on three key constraints: power, water, and labor.

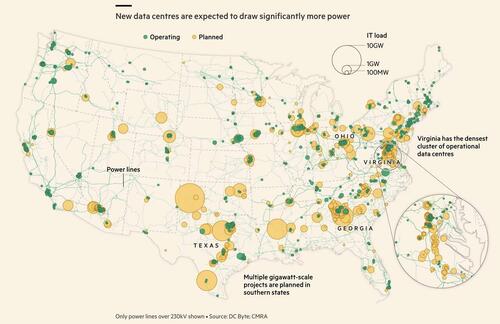

1. Energy: Power remains the most critical near-term constraint for data center deployment, while flexible load management and Behind-the-Meter solutions could help close the power gap. While cloud and AI inference workloads generally require proximity to end-users -- creating power shortages in these congested markets -- AI training workloads are location-agnostic and migrating to remote areas with available power. Grid conditioning or flexible load management for data centers during peak electricity consumption could unlock significant capacity. A Duke University study suggested that 76 GW of new load (10% of US aggregate peak demand) could be integrated if data centers accepted average annual load curtailment of 0.25% (99.75% up time) and 98 GW added for curtailment of 0.5% (99.5% up time). While this could potentially unlock ~100 GW of capacity, Mr. Monroe notes that adoption: (a) is hindered by the industry's inherent risk aversion of cycling IT equipment off and on; and (b) may require stronger financial or regulatory incentives.

Behind-the-Meter power is a costly and likely temporary bridge to initial grid gaps. While a single digit percentage of data centers in the pipeline have BTM requests, Mr. Monroe highlighted this can still be significant for power demand given these are typically larger data centers. Primarily deploying natural gas simple cycle generators, onsite power solutions cost 5x-20x more than grid power. However, Mr. Monroe highlighted that deploying BTM solutions to push forward data center startups can be an economically viable choice given the immense profitability of large scale AI data centers. According to Mr. Monroe, data centers deploying BTM power ultimately aim to connect to the grid eventually over three years, while either relocating to other data centers, integrating and selling power back into the grid, or retiring BTM assets.

2. Water: Community, regulatory and chip advancement pressures likely to shift the industry towards more water-efficient cooling technologies coming at significant energy costs. The industry is seeing a shift from the traditional water-intensive evaporative approaches towards more waterless designs, especially among hyperscalers, as community, regulatory and technological pressure mounts. According to Mr. Monroe, the shift towards closed-loop and waterless cooling systems is likely to raise Power Usage Effectiveness (PUE) from best-in-class levels of 1.08 to 1.35-1.40, representing a 35%-40% energy overhead versus 8% in evaporative systems. Although innovations such as direct-to-chip liquid cooling and higher-temperature water cooling could enable more efficient heat transfer in more geographic locations, co-location data centers are likely to remain committed to chiller-based designs given their diverse customer base and need to commit to cooling architecture early in construction. Regardless of any diminishing share of overall data center cooling solutions, according to Mr. Monroe the demand for chillers is expected to continue to see a material increase over the next decade, driven by overall growth in data center capacity.

3. Labor: Skilled labor shortage could become the next gating factor for data center deployment. Data centers are differentiated from generic industrial buildings by the specialized electrical and mechanical systems required, making electricians and pipefitters critical to the continued data center build out. According to Mr. Monroe, the skilled labor shortage represents the next major constraint after power. Industry organizations, in collaboration with technical universities and colleges, are actively developing training programs to address this gap, while attempting to reach students as early as middle school to make skilled trades more attractive career paths. We estimate the US will require >500,000 net new workers across manufacturing, construction, ops & maintenance, and transmission and distribution to deploy all the power to meet demand by 2030.

Related coverage:

Looking ahead, the key question is whether the U.S. can sustain a largely uninterrupted surge in data center capex, given how much these buildouts are now embedded in both the macro narrative and tech valuations. The investment thesis assumes that continued buildout translates into measurable productivity gains and, in turn, a multi-year uplift in growth. Overall, the execution risk boils down to critical inputs and infrastructure, including core components, grid access, and related supply chain bottlenecks, which could slow buildouts and stymie overly optimistic expectations.

To bypass these ground-based constraints, that's why the narrative of data centers in space has emerged.

Professional subscribers can see the full note on our new Marketdesk.ai portal.

Loading recommendations...