Shortly after a disappointing ISM Manufacturing report (which started yields falling), Fed Governor Christopher Waller (quietly) dropped quite a bombshell on markets for those that were paying attention.

Specifically remarking on a Fed paper "Quantitative Tightening around the Globe: What Have We Learned?", Waller told the 2024 U.S. Monetary Policy Forum in New York that he would like to see two key developments in the Fed's portfolio:

"First, I would like to see the Fed's agency MBS holdings go to zero. Agency MBS holdings have been slow to run off the portfolio, at a recent monthly average of about $15 billion, because the underlying mortgages have very low interest rates and prepayments are quite small. I believe it is important to see a continued reduction in these holdings.

Second, I would like to see a shift in Treasury holdings toward a larger share of shorter-dated Treasury securities. Prior to the Global Financial Crisis, we held approximately one-third of our portfolio in Treasury bills. Today, bills are less than 5 percent of our Treasury holdings and less than 3 percent of our total securities holdings. Moving toward more Treasury bills would shift the maturity structure more toward our policy rate - the overnight federal funds rate - and allow our income and expenses to rise and fall together as the FOMC increases and cuts the target range. This approach could also assist a future asset purchase program because we could let the short-term securities roll off the portfolio and not increase the balance sheet. This is an issue the FOMC will need to decide in the next couple of years."

Translation: Waller is hinting at an 'Operation Reverse-Twist' which will lower short-term yields and steepen the yield curve.

While much chatter has been about the tapering of QT, they will of course not call 'Operation Reverse Twist' by its proper name - QE - because that would reignite animal spirits further and put The Fed in the awkward position of buying short-term bonds at the same as it is hiking rates.

His comments come as Dallas Fed chief Lorie Logan reiterated it’ll likely be appropriate to start slowing the pace at which it shrinks its balance sheet.

All of which is promptly timed just as the pace of RRP erosion is set to accelerate after month-end malarkey and The Fed's BTFP facility is set to expire.

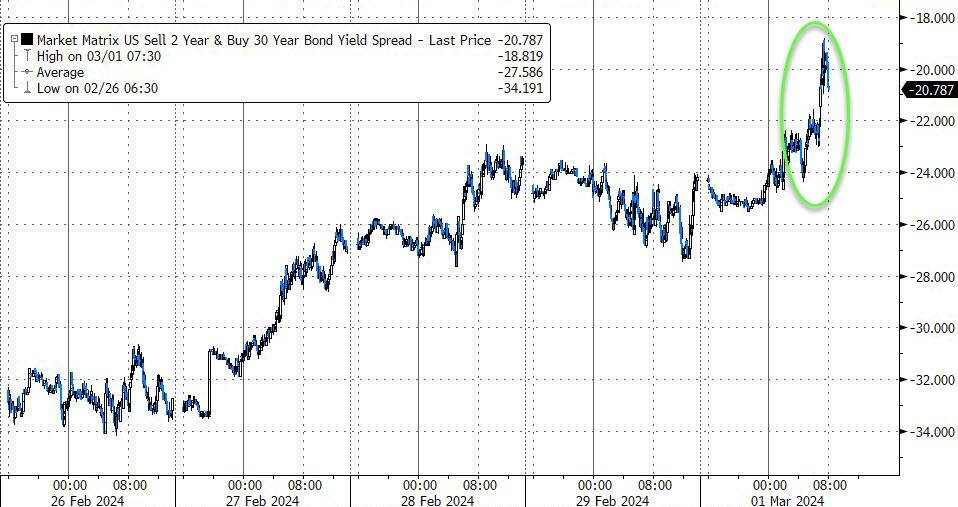

As one would expect this sent yields lower (especially in the short-end)...

Source: Bloomberg

...bull-steepening the yield curve...

Source: Bloomberg

And perhaps more notably, gold is accelerating higher...

Source: Bloomberg

So will The Fed start QE Reverse-Twist... and hike rates to tamp down a resurgent inflation thanks to animal spirits 2.0 prompted by their prior pivot?