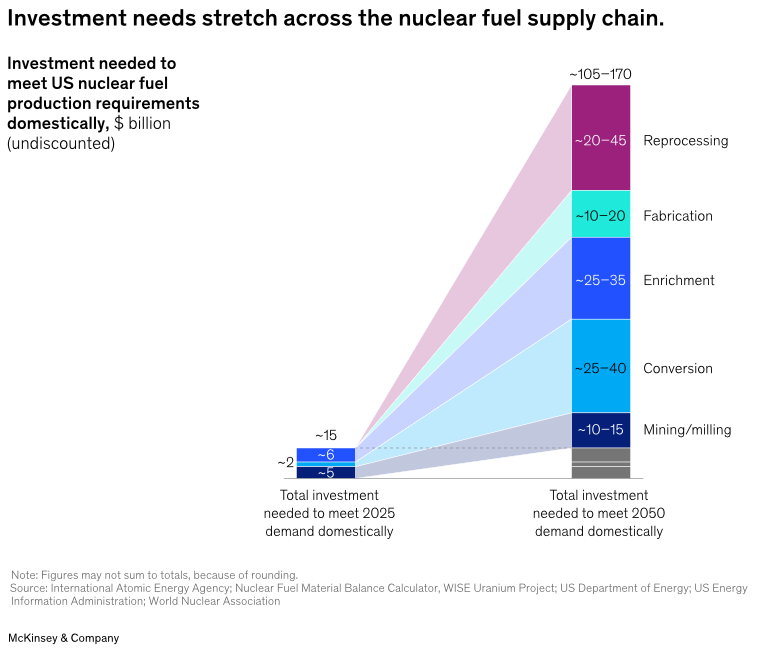

To support current commercial nuclear operations, plus 300 GW of new nuclear capacity for a total of roughly 400 GW by 2050, all fueled domestically, the country would need to invest between $105 billion and $170 billion across the entire nuclear fuel cycle.

Is it still called a bottleneck if the entire industry is the problem?

The consulting firm McKinsey & Company used the most aspirational scenario from the Trump administration’s May 2025 executive orders as its benchmark for their recent report. That means rebuilding capacity from mining and milling through conversion, enrichment, fabrication, and even reprocessing.

It's looking more and more like the $2.7 billion award from the DOE for domestic enrichment barely scratches the surface:

- $15-20 billion for mining and milling

- $30-45 billion for conversion

- $30-40 billion for enrichment

- $10-20 billion for fabrication

- $20-45 billion for reprocessing

These figures assume a mix of new and existing reactors, including Gen IV designs that will demand high-assay low-enriched uranium (HALEU).

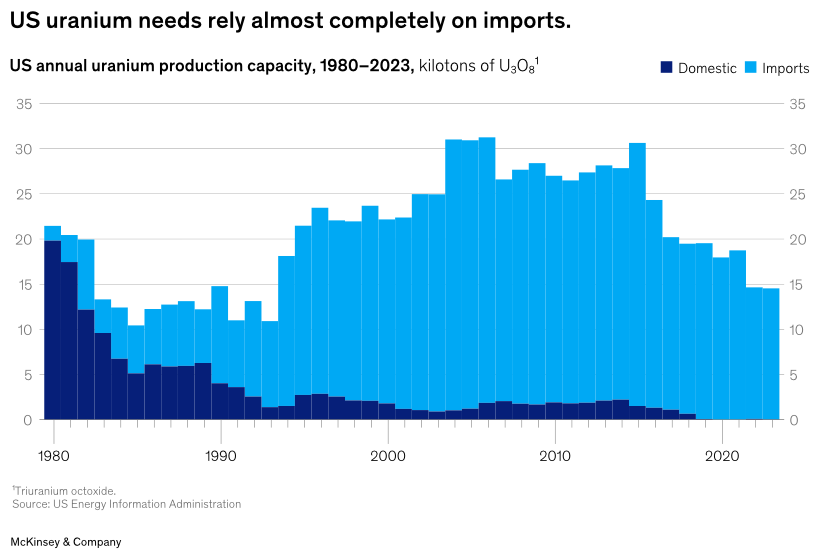

We have documented the vulnerabilities for months. Today the United States imports about 99 percent of the raw uranium ore needed for its commercial fleet…

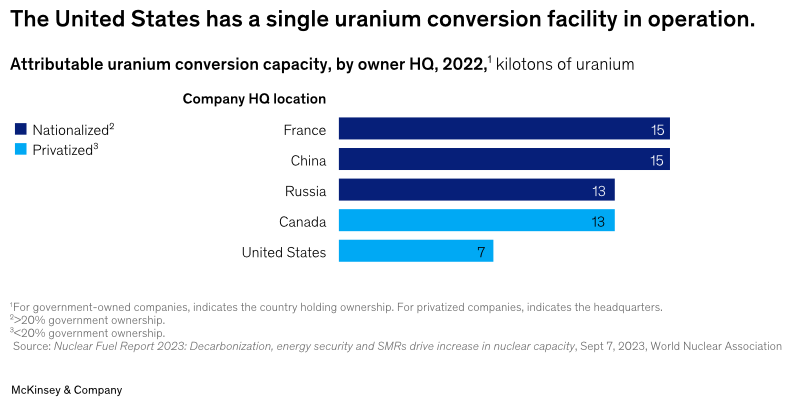

With milling capacity effectively nonexistent and conversion limited to a single operating facility…

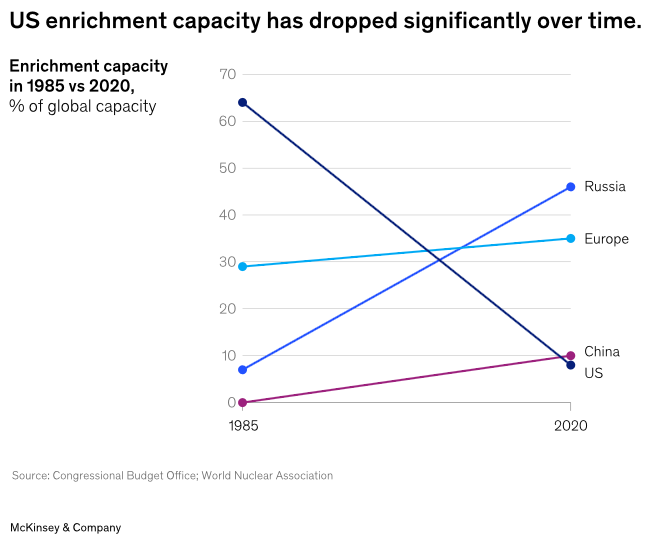

And enrichment capacity covers only about one-third of domestic needs…

The gaps leave utilities exposed to geopolitical risks and price volatility, a point we highlighted when uranium spot prices pulled back earlier this year even as long-term supply deficits widened…

Progress is Uranium: the next gold pic.twitter.com/2SSjvRkdSg

DOE has also awarded nearly $3 billion for enrichment projects, including $900 million each to Centrus Energy and General Matter, while the Export-Import Bank has backed up to $4.2 billion in additional financing. Centrus recently committed $560 million to scale centrifuge manufacturing in Oak Ridge, and we covered its joint-venture discussions with Oklo for HALEU deconversion services.

The private sector is also making progress on their own, not wanting to wait for the government to sort itself out and attempt to take market share while it's up for grabs.

Uranium Energy Corp is expanding ISR mining and advancing conversion licensing. New entrants like FluxPoint Energy and LIS Technologies are targeting conversion and next-generation laser enrichment facilities, aiming for commercial operations before 2030.

We also noted Goldman Sachs’ updates showing persistent supply-demand mismatches that continue to support higher uranium prices over the coming decades.

McKinsey stresses that capital alone will not suffice. Permitting reform, infrastructure build-out, workforce development, and advanced technologies will prove critical to compressing the long lead times inherent in fuel-cycle projects. The firm acknowledges 100% domestic sourcing will prove challenging, yet the analysis underscores that options exist if stakeholders maintain focus.