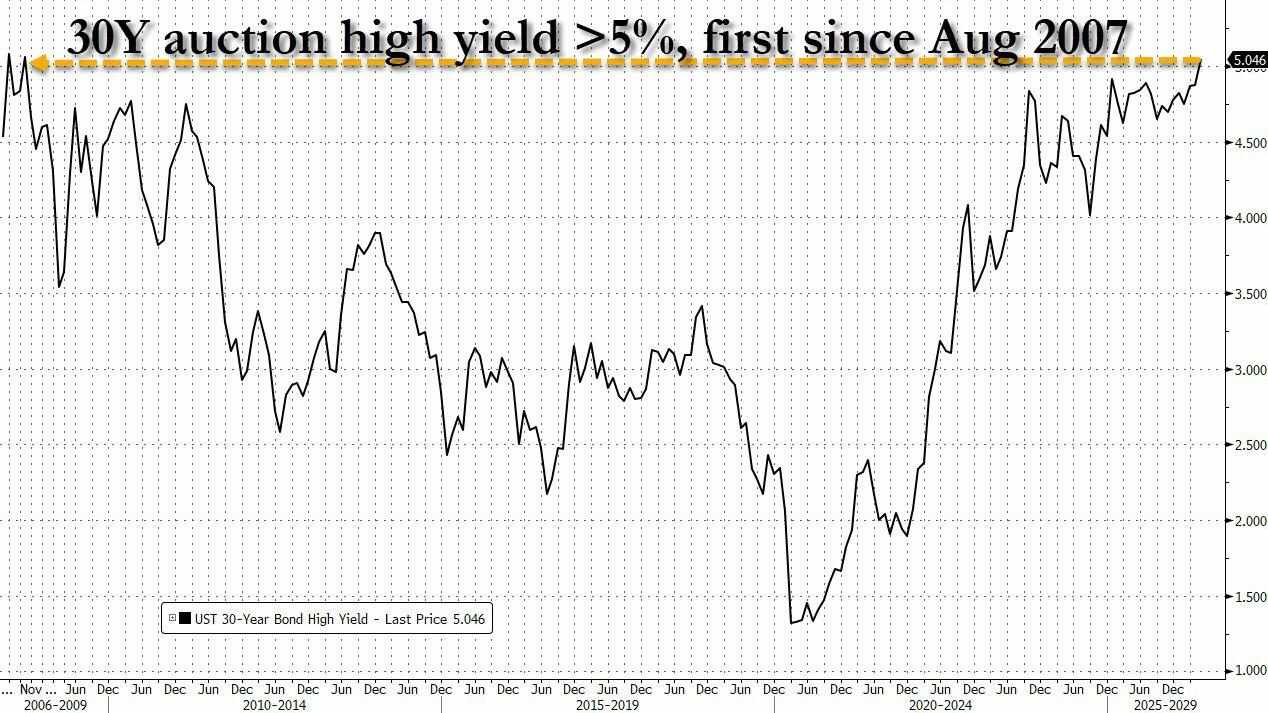

Moments ago, the last refunding auction of the week, the sale of $25BN in 30Y paper, made history: it was the first 30Y auction to print with a high yield above 5%, and a coupon of 5%, since August 2007... which as veteran traders will recall was the month of the historic quant crash which marked the S&P highs at the time and eventually culminated in the global financial crisis.

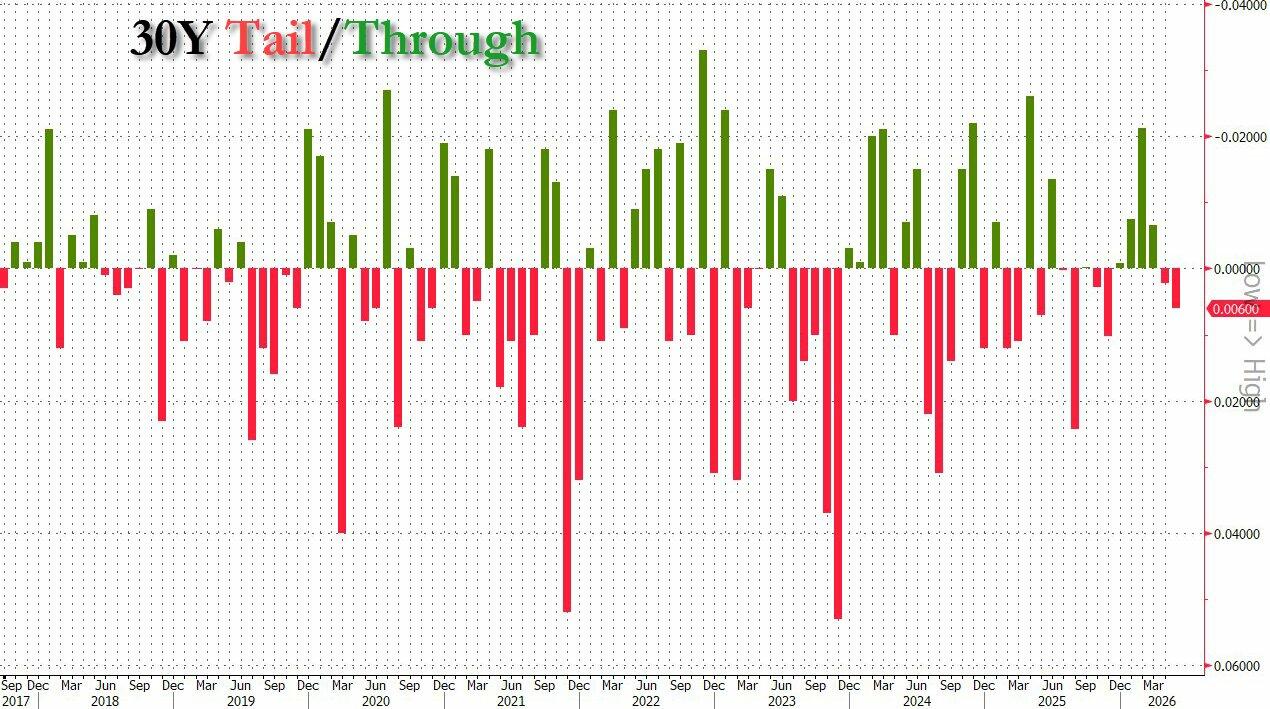

The auction priced at a high yield of 5.046%, up sharply from 4.876% in April, and tailed the 5.041% When Issued by 0.5bps, the second consecutive tail following 4 stop-throughs.

But, as noted above, what is more notable was that this was the first 5% interest rate coupon 30Y auction, and the the first 30Y auction with a high yield above 5% since... August 2007 when surging rates sparked a quant crash. Come to think of it, unlike retail momentum chasers, quants have had a terrible month. How much longer can they last? But we digress...

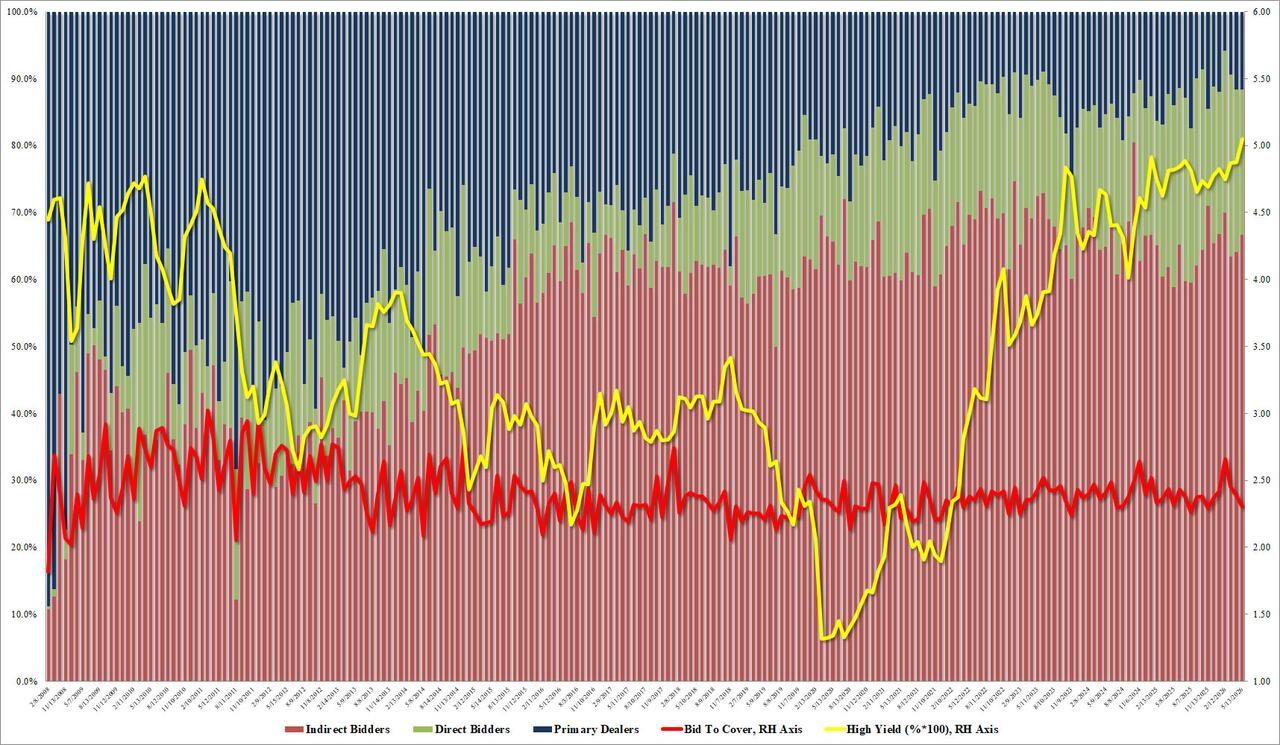

Going back to the auction, the uglyness was all around: the bid to cover was 2.303, down from 2.385, below the 2.43 six auction average and the lowest since Nob 2025.

Internals were not quite as bad, with Indirects taking down 66.6%, up from 64.1% in April and just below the 66.8% recent average. And with Directs awarded 21.74%, Dealers were left with 11.7%.

Overall, this was an ugly, tailing auction, but the question on everyone's lips is whether today's quction will - like in August 2007 - be the VaR shock equivalent of a bond auction that pops this particular bubble. For the answer keep a close eye on quants who are suffering badly.