Looking at the week ahead, Nvidia’s earnings on Wednesday, with a market capitalisation now of $5.46tn, will be the main event. In economics, we have the global flash PMIs on Thursday, along with inflation data from Canada tomorrow, the UK on Wednesday, and Japan on Friday. From central banks, the highlight will be the FOMC minutes on Wednesday. Those flash PMIs will be important, as they’re one of the first indicators on how the global economy has performed this month, so will be scrutinized for any signs of how the war in Iran is impacting activity and prices.

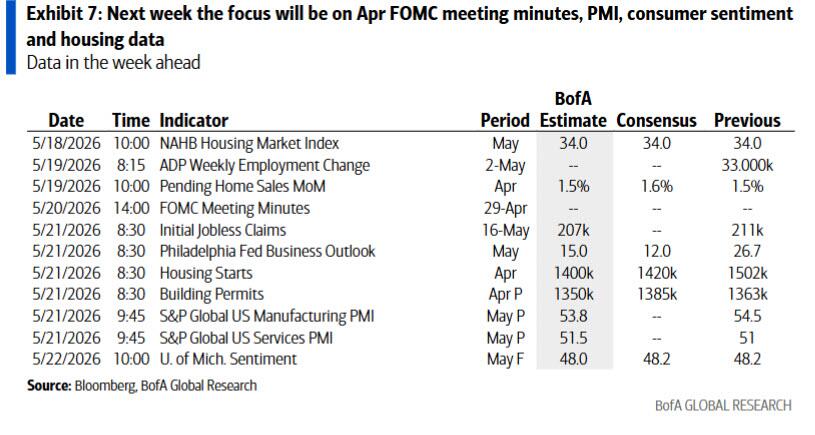

The US calendar is relatively light, with the NAHB housing market index today expected to remain unchanged at a cyclically low 34, followed by Tuesday’s pending home sales, where a modest +1.0% increase is anticipated (from +1.5% previously). Attention will then turn to Thursday’s April housing activity data, where housing starts are expected to ease to an annualized pace of 1.425mn (from 1.502mn), while permits are projected to tick higher to 1.375mn (from 1.363mn). All estimates are according to our economists.

Beyond housing, Thursday is the key day for macro releases. The weekly initial jobless claims are expected to edge slightly lower to 209k (from 211k). The same day will also bring the Philadelphia Fed manufacturing survey, where our economists expect a pullback to +21.0 (from +26.7), alongside the flash PMIs. In the US, manufacturing is expected to soften marginally to 53.7 (from 54.5), while services are seen ticking up to 51.5 (from 51.0).

In contrast to consumer sentiment—which will see an updated reading of the Michigan survey on Friday (expected at 48.2 versus 49.8 previously)—business surveys have generally remained more resilient despite the energy shock. That said, some indicators have shown rising input costs and lengthening delivery times, developments that could signal renewed inflationary pressure building beneath the surface.

Turning to central bank communications, the Fed speaker slate is relatively limited but still notable. Governor Waller is scheduled to participate in an ECB policy panel tomorrow, alongside comments from Philadelphia Fed President Harker (voter) on the outlook. On Wednesday, Vice Chair Barr will discuss consumer financial health metrics, while the Fed will also publish the minutes from the April FOMC meeting. Richmond Fed President Barkin (non-voter) will follow on Thursday with remarks on the economy, before Governor Waller rounds out the week with a further appearance on Friday.

In Europe, the highlights will include the UK labour market report tomorrow and inflation data on Wednesday. DB's UK economist expects headline CPI to slow to 2.98% YoY and core CPI to fall to 2.61% YoY. More detail and forecasts are in the full inflation spotlight note here. The UK will also release the GfK May consumer confidence index and April retail sales on Friday. Other notable European releases include Eurozone consumer confidence on Thursday and Germany’s Ifo survey on Friday.

In Asia, Japan faces a busy week, with key data including Q1 GDP tomorrow and April nationwide CPI on Friday. Our Chief Japan economist expects positive real growth of an annualised 1.3% QoQ for the GDP report and sees core CPI inflation, excluding fresh food, holding at 1.8% YoY, alongside a retreat in core-core inflation, excluding fresh food and energy, to 2.2% (from 2.4% in March).

Finally, beyond Nvidia’s earnings on Wednesday, results are also due from major US retailers, including Walmart, Home Depot, and TJX.

Courtesy of DB, here is a day by day calendar of the week's main events:

Monday May 18

- Data: US May New York Fed services business activity, NAHB housing market index, March total net TIC flows, China April retail sales, industrial production, investment, home prices, Italy March trade balance

- Central banks: BoE's Greene and Mann speak

- Earnings: Baidu, Ryanair Holdings

- Other: G7 meeting of finance ministers and central bank governors (through May 19)

Tuesday May 19

- Data: US April pending home sales, UK March average weekly earnings, unemployment rate, April jobless claims change, Japan Q1 GDP, March capacity utilisation, Eurozone March trade balance, Canada April CPI, March building permits

- Central banks: Fed's Waller speaks, ECB's Lane and Makhlouf speak, BoE's Breeden speaks

- Earnings: Home Depot, Amer Sports

Wednesday May 20

- Data: UK April CPI, RPI, PPI, March house price index, Germany April PPI, Denmark Q1 GDP

- Central banks: FOMC minutes, Fed's Paulson and Barr speak, China 1-yr and 5-yr loan prime rates

- Earnings: NVIDIA, Analog Devices, TJX, Lowe's, Intuit, Target, Experian, Marks & Spencer

- Auctions: US 20-yr Bonds ($16bn)

Thursday May 21

- Data: US, UK, Japan, Germany, France and Eurozone May preliminary PMIs, US May Philadelphia Fed business outlook, Kansas City Fed manufacturing activity, April housing starts, building permits, initial jobless claims, Japan April trade balance, March core machine orders, Italy March current account balance, ECB March current account, Eurozone March construction output, Q1 labour costs, May consumer confidence, Australia April labour force survey

- Central banks: ECB's Villeroy speaks, BoJ's Koeda speaks, BoE's Taylor speaks

- Earnings: Walmart, Deere, Generali, Ross Stores, Take-Two, BT, Zoom, Workday

- Auctions: US 10-yr TIPS (reopening, $19bn)

Friday May 22

- Data: US May Kansas City Fed services activity, UK May GfK consumer confidence, April retail sales, public finances, Japan April national CPI, Germany June GfK consumer confidence, May Ifo survey, France May business confidence, Canada March retail sales, April industrial product price index, raw materials price index

- Central banks: Fed’s Waller speaks, ECB's Vujcic, Kazimir, Muller and Lane speak

- Earnings: Cie Financiere Richemont, Lenovo

Taking a look at just the US, Goldman writes that the key economic data release this week is the Philadelphia Fed manufacturing index on Thursday. There are several speaking engagements with Fed officials this week, including events with Governors Waller and Barr and Presidents Paulson and Barkin. The minutes to the FOMC’s April meeting will be released on Wednesday.

Monday, May 18

- 10:00 AM NAHB housing market index, May (consensus 34, last 34)

Tuesday, May 19

- 08:00 AM Fed Governor Waller speaks: Fed Governor Christopher Waller will participate in a panel at the European Central Bank. Moderated Q&A is expected. On April 17th, Waller cautioned that higher oil prices as a result of the Iran war could lead to a “more lasting increase in inflation.” Waller noted that “if the risks to inflation outweigh those to the labor market,” that could require “maintaining the policy rate at the current target range.”

- 10:00 AM Pending home sales, April (GS +1.0%, consensus +1.0%, last +1.5%)

- 07:00 PM Philadelphia Fed President Paulson (FOMC voter) speaks: Philadelphia Fed President Anna Paulson will speak about the economic outlook at the Atlanta Fed’s Financial Markets Conference. Text and audience Q&A are expected. On March 27th, Paulson said that there was “a little bit more of a risk that the transmission of higher fuel prices, higher fertilizer prices, into inflation expectations is faster and maybe a little bit more durable.” That said, Paulson also noted that “for [all these shocks] to turn into sustained inflation, you need a mechanism that keeps that going” and that “on the wage-setting side, it doesn’t seem like there’s a lot of impetus that would make that happen now.”

Wednesday, May 20

- 09:15 AM Fed Governor Barr speaks: Fed Governor Michael Barr will deliver a speech on consumer financial health at a conference in Atlanta, Georgia. Text is expected. On May 5th, Barr said that “the longer [the Iran war] goes on, the greater the risk that the inflation we’re seeing in these prices becomes embedded in the economy, and then we have to worry more.” Barr noted that “we’re in a situation right now where we really need to wait and see to understand what direction [the conflict] is going.”

- 02:00 PM FOMC meeting minutes, April 28-29 meeting: At its April meeting, the FOMC left the fed funds rate and the policy guidance in its statement unchanged. Presidents Hammack, Logan, and Kashkari dissented against the implicit easing bias in the standing policy guidance, while Governor Miran dissented in favor of a 25bp cut. Chair Powell said that the number of FOMC participants who could support moving to balanced guidance has increased since March and that the center of the FOMC “is moving toward a more neutral” outlook for future rate changes, but most felt making a change now was unnecessary. We pushed back our expectations for Fed cuts by one quarter to December and March. With energy cost passthrough likely to keep year-over-year core PCE inflation closer to 3% than 2% all year, we think that a combination of lower monthly inflation prints after the oil shock fades and further labor market softening will likely be needed for the FOMC to cut this year. We still expect that bar to be met but now expect it to take a bit longer.

Thursday, May 21

- 08:30 AM Initial jobless claims, week ended May 16 (GS 210k, consensus 210k, last 211k); Continuing jobless claims, week ended May 9 (consensus 1,785k, last 1,782k)

- 08:30 AM Philadelphia Fed manufacturing index, May (GS 20.0, consensus 18.0, last 26.7)

- 08:30 AM Housing starts, April (GS -3.5%, consensus -5.5%, last +10.8%)

- 09:45 AM S&P Global US manufacturing PMI, May preliminary (consensus 53.7, last 54.5); S&P Global US services PMI, May preliminary (consensus 51.0, last 51.0)

- 12:20 PM Richmond Fed President Barkin (FOMC non-voter) speaks; Richmond Fed President Tom Barkin will deliver a speech at the Urban Land Institute Triangle in Raleigh, North Carolina. Text and Q&A are expected.

Friday, May 22

- 10:00 AM University of Michigan consumer sentiment, May final (GS 48.2, consensus 48.3, last 48.2); University of Michigan 5-10-year inflation expectations, May final (GS 3.4%, last 3.4%)

- 10:00 AM Fed Governor Waller speaks; Fed Governor Christopher Waller will deliver a lecture on the economic outlook at the Frankfurt School of Finance and Management in Germany. Text and moderated Q&A are expected.

Source: Goldman, DB