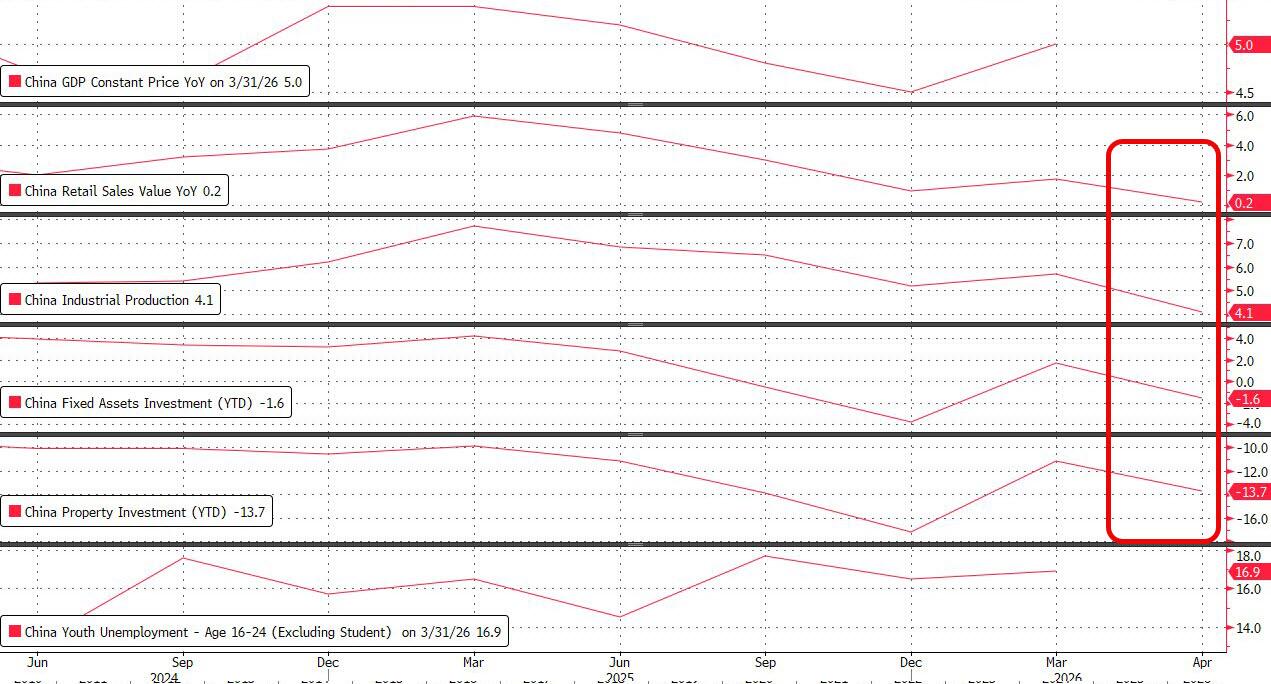

Confirming our Sunday preview, overnight China reported growth data which slowed across the board in April with investment resuming declines, retail sales missing sales and growing at the weakest rate in 4 years while industrial production rose at the slowest pace in three years, calling into question Beijing's reluctance to add stimulus to the economy as a global energy crisis hits factories and consumers across the world.

China's Monday data dump of official data on Monday painted a picture of an economy where booming exports no longer offset deteriorating consumption at home, prompting analysts at banks including Nomura and SocGen to urge bolder measures in support of growth.

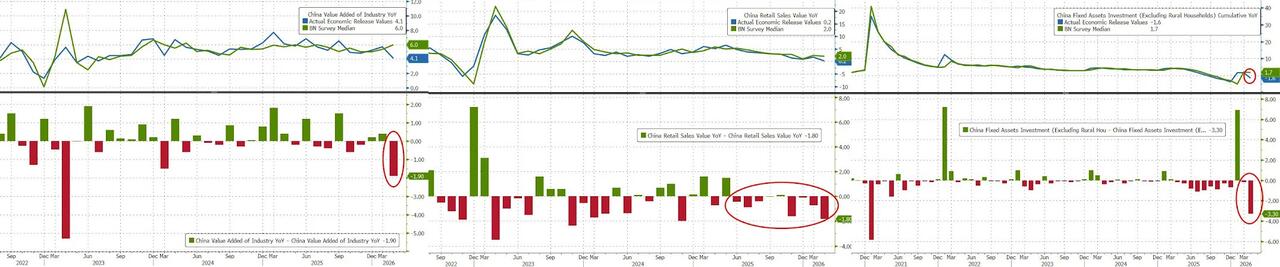

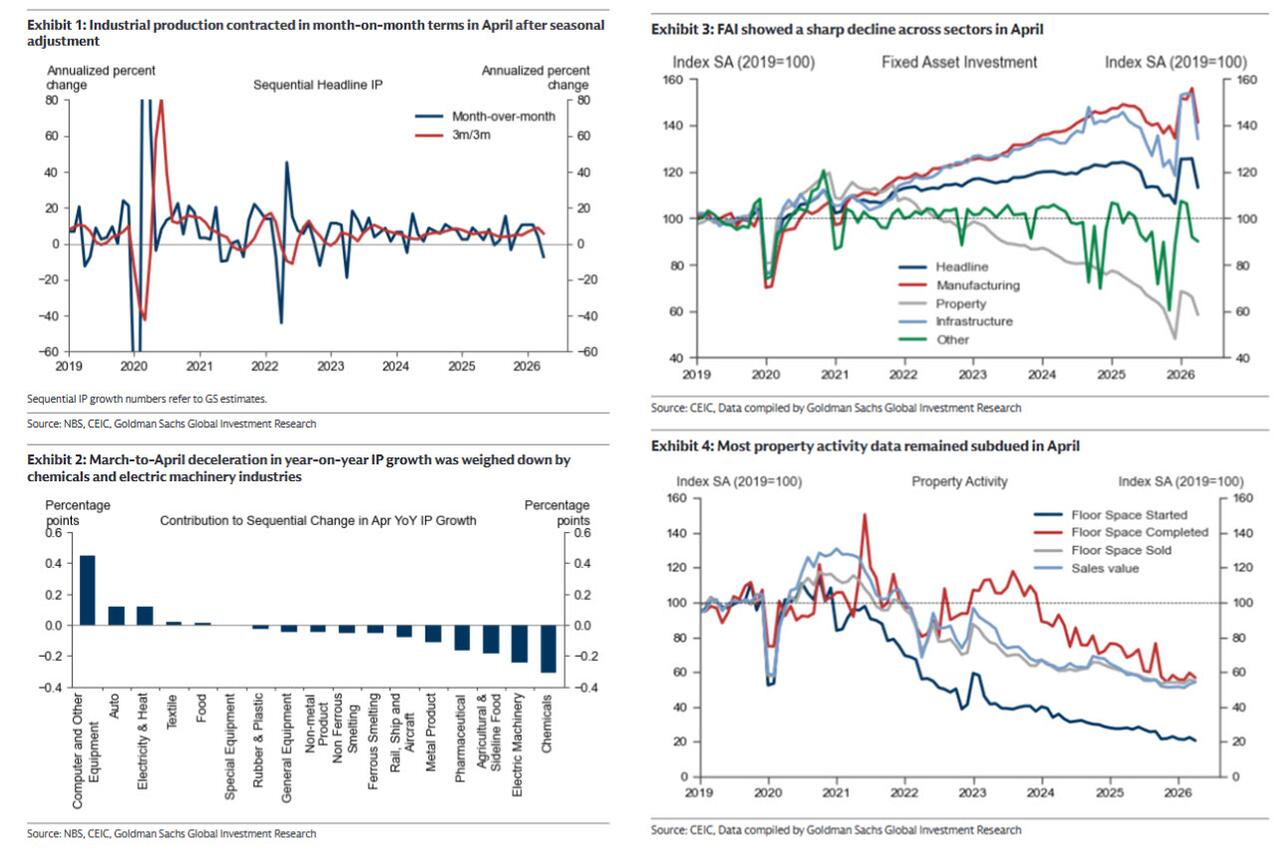

As shown in the chart below, fixed-asset investment unexpectedly shrank 1.6% in the first four months of 2026 from a year earlier, while industrial production grew just 4.1% last month, the weakest in almost three years. Retail sales also missed forecasts and rose just 0.2% in April, the worst reading since they contracted in December 2022, when China reopened from Covid.

What is shocking is that it is common knowledge that Beijing traditionally massages its economic data to present itself in the rosiest possible light: the fact that it allowed data this ugly would suggest that the picture on the ground is much uglier.

Goldman's Delta One head Rich Privorotsky captured this sentiment well, writing this morning that "overnight news from China showed economic data materially below expectations. Industrial production, retail sales and fixed asset investment all missed meaningfully. It’s hard to tell whether this reflects genuine demand destruction but perhaps it helps explain how the oil market has managed to balance despite ongoing supply concerns. I genuinely can’t remember a period when Chinese data, which tends to be heavily massaged, missed by anything close to this magnitude. Negative read through for consumption related categories."

Remarkably, not a single economist surveyed by Bloomberg had predicted as pessimistic a reading for industry, retail sales and investment. The disappointing performance of the world’s second-biggest economy last month is a reminder of its domestic vulnerabilities, after a global artificial intelligence investment boom sent trade soaring.

The breadth of the acute slowdown in April has put the prospect of a more aggressive stimulus back on the agenda after China stood out in its resilience to the fallout from the Iran war. The government pulled back on fiscal spending in March, while the central bank has steered clear of even hinting at any further loosening in policy, amid ample market liquidity and weak demand for credit.

Fu Linghui, spokesman for the National Bureau of Statistics, described the deterioration of economic indicators as “a normal fluctuation from month to month.” But he also highlighted challenges such as a persistent imbalance between supply and demand as well as a complex global environment.

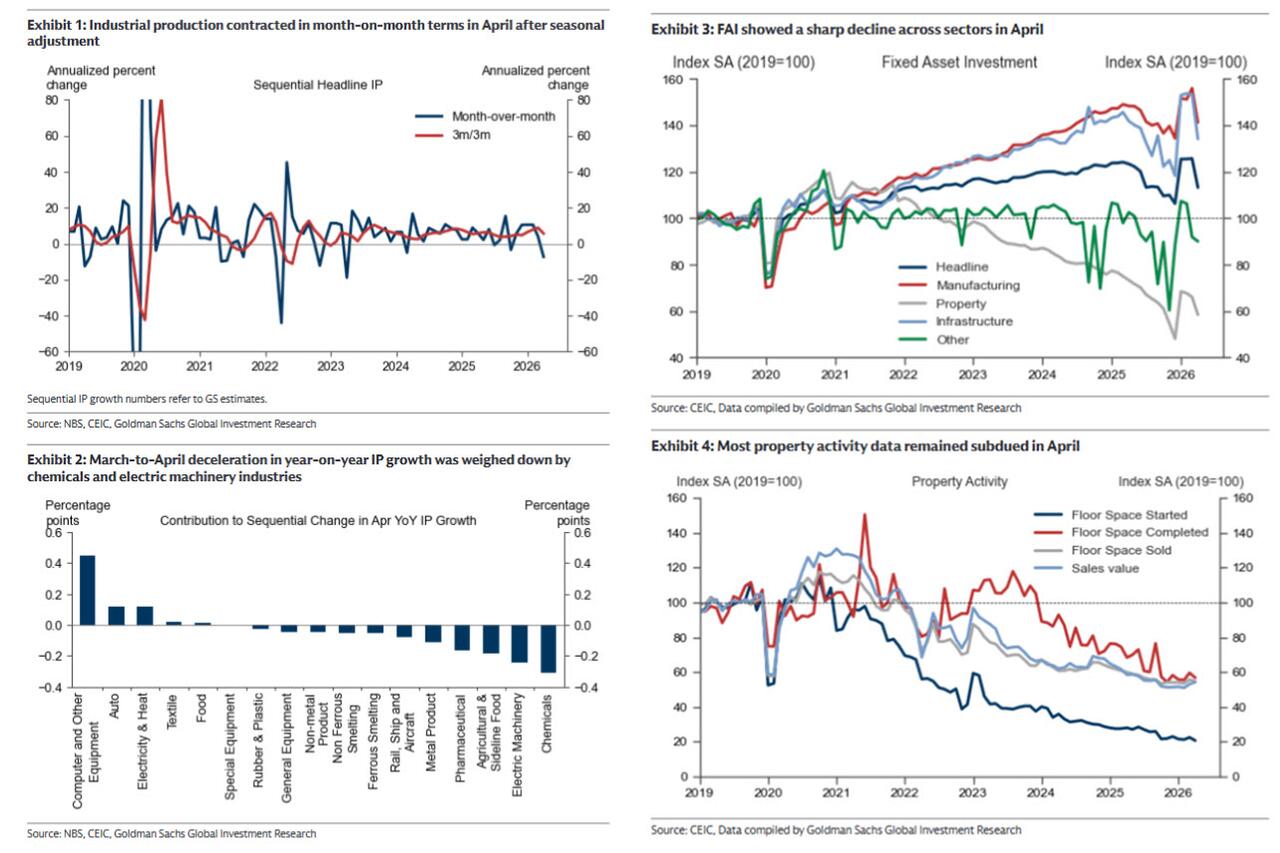

Investment plunged by around 8% in April from a year earlier, according to estimates from Goldman Sachs and Capital Economics, returning to a similar pace of decline seen in the second half of 2025. Manufacturing and infrastructure investment both weakened, while private investment plummeted

In response to the dismal data, Nomura economists wrote that authorities “might need to step up policy support for stabilizing growth,” adding that “Beijing has no room for complacency.”

A rising number of economists has been forecasting the People’s Bank of China won’t lower interest rates this year after the oil shock pushed up inflation expectations, though many still expect a cut to lenders’ reserve requirement ratio. The PBOC last lowered the policy rate and the RRR at the peak of the trade tensions with the US a year ago.

Authorities are still likely to take a patient approach and avoid rushing out response to just one month of data. The Communist Party’s decision-making Politburo will convene in July to review economic growth and policies, making it the next potential window for any adjustment in stimulus.

“The stance still seems to be to play cautiously,” said Jing Liu, chief economist for Greater China at HSBC in an interview on Bloomberg TV. “Our base case is no extra stimulus for the economy for the time being.”

Even though many manufacturers are struggling to cope with higher raw material costs, overall exports soared as Chinese tech products found willing buyers abroad. Greater demand for green energy products is also benefiting China. But a sustained weakening of investment and consumption at home could still bring risks to Beijing’s goal of achieving 4.5% to 5% artificial growth this year.

The April data suggest gross domestic product may expand as little as 4.1% on-year in the second quarter, which could prompt incremental policy easing, according to Macquarie Group Ltd. For now, Goldman is maintaining its forecast for a GDP gain of 4.7% in April-June, compared with 5% in the first three months of the year.

The data “should keep PBOC easing – RRR and even rate cuts – firmly on the table, while fiscal top-up may come later,” SocGen's head China economist Wei Yao wrote in a note.

The plunging manufacturing data comes at a time of continued dismal credit demand and heavy rainfall in southern China, which could be behind the sharp fall in capital spending, Goldman economist Lisheng Wang said in a note (available to pro subs here).

Statistical adjustment is another potential factor. Many economists believe authorities took measures to correct over-reporting of the data in late 2025. Such a change may have exaggerated the volatility of the figures recently, as the on-year contraction in steel and cement output narrowed in April, according to Goldman Sachs.

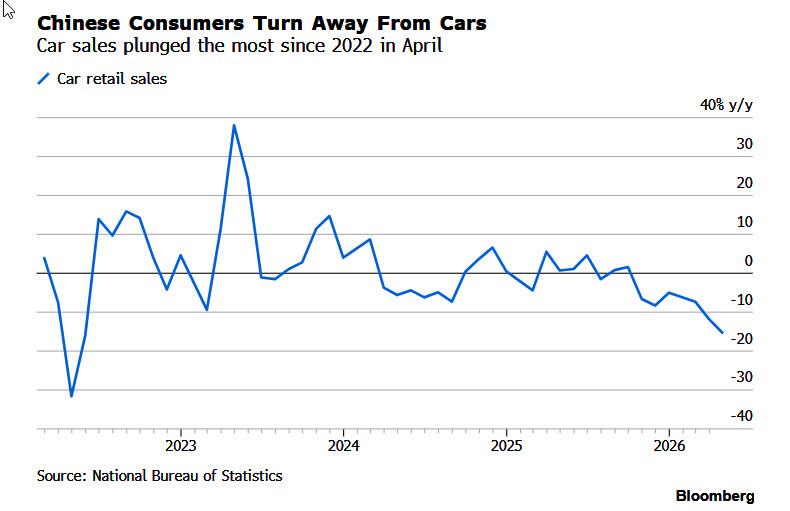

The consumer economy has meanwhile continued to struggle as households spent less on items as varied as autos and furniture. Car sales plunged 15% in April from a year earlier, the worst contraction since mid-2022, when the country was under Covid restrictions. The government has scaled back subsidies for electric vehicle purchases this year, while the Iran oil shock hurt sales of gasoline-powered cars.

Purchases of home appliances and furniture — products that used to be buoyed by government subsidies — declined at a double-digit pace. Gold, silver and jewelry sales plummeted 21% — a huge reversal from earlier this year and 2025, when soaring prices for precious metals led to a speculative investment frenzy.

The industrial sector is also getting more lopsided as export-driven sectors lead the growth while industries that relied on domestic sales lagged. The production of electronics, lifted by soaring global demand for AI chips, expanded 15.6% in April, the fastest pace in two years.

The auto industry also expanded briskly at 9.2%, as overseas EV sales took off. Meanwhile, commodities linked to real estate and construction — such as cement, glass and steel — recorded declines, while crude oil processing volume fell, which ING Bank economist Lynn Song attributed to the war’s impact

Soaring chip prices may partly explain why factory output weakened even as exports surged. While industrial production is reported after an adjustment made for inflation, sales abroad are calculated in nominal terms, making it hard to separate movements in prices versus volumes. Surging costs of chips and electronics accounted for about half of April’s 14% headline export growth, according to Nomura.

“China still looks like a two-speed economy: strong in strategic manufacturing and exports, but weak where household confidence matters most,” said Charu Chanana, chief investment strategist at Saxo Markets in Singapore. “The concern is not just that activity missed, but that the weakness is broadening across the domestic side of the economy.”

There is one silver lining when it comes to the Chinese economy: exports are expected to remain strong after climbing 15% in the first four months from a year ago. Stabilizing trade ties with the US, reinforced by President Donald Trump’s visit to Beijing, further bolster the outlook.

But a turnaround is nowhere in sight for domestic consumption. Chinese households net repaid the most loans in April since comparable data going back to 2010.

“Policy space remains ample,” said Hao Zhou, chief economist at Guotai Junan International Holdings. “The April data are less a sign of deterioration than a trigger for more proactive easing — which should help anchor growth and support a gradual recovery into the second half of the year.”