By Peter de Groot, Head of Macro Strategy at Rabobank

The Inflation Regime That Doesn't Fade

As we noted at the outset of the Gulf conflict, history rarely repeats – but it often rhymes. The closure of the Strait of Hormuz is increasingly revealing a familiar pattern: the building blocks of a global stagflationary shock are falling into place.

A closer look across inflation indicators in advanced economies shows a clear and consistent structure. The upstream impact has been immediate and forceful – exactly as expected in an energy-driven shock. The surge in oil and gas prices has translated into sharp increases in petroleum products such as diesel, and into key industrial inputs like sulphur and fertilisers. Producer price expectations – particularly in energy-intensive sectors such as chemicals, base metals, and wood – have risen rapidly, in many cases outpacing the (initial) post-Covid surge. European industrial surveys point to strong repricing at the start of the production chain.

But further downstream, the picture is more nuanced, for now. While higher input costs are being passed through, the degree of transmission appears more muted than during the inflation surge of 2021–2022. Initial producer price data suggest that firms are adjusting prices, but not with the same breadth or intensity yet. Part of this may be timing – pass-through is always gradual – and whilst the gap between sharply rising price expectations and more modest realized price increases is notable, this could also point to more significant price hikes in the months ahead.

At the consumer level, the divergence is clearer. Inflation has responded, but the impulse remains concentrated in energy and energy-related components. Headline CPI prints have broadly matched expectations, and in some cases even surprised to the downside. Core inflation has remained contained. However, the same sort of slow transmission was seen during the initial phase of the 2021-2022 inflation surge, which, arguably, led policy makers to respond too slowly. So it’s too early to draw any firm conclusions and ‘transitory’ cannot be one of them, for now.

However, there is one crucial difference: the starting point for this shock is materially weaker demand. Labor markets have cooled in many places, albeit not to the same degree. US payrolls growth and job openings have slowed. In the Eurozone, labor market tightness indicators have eased (even as unemployment has stayed at cyclical lows). In the UK, unemployment has moved back to around 5%, vacancies have dropped to a five-year low, and wage growth continues to slow. As Stefan Koopman, our UK analyst, notes, these are not the conditions of an overheated economy requiring aggressive monetary tightening. Instead, they suggest increasing slack – an environment in which firms may struggle to fully pass on higher costs without sacrificing demand.

As a result, while energy prices are likely to push inflation higher in the coming months, the broader macro backdrop does not appear conducive to a sustained second-round inflation spiral. That said, central banks may still feel compelled to respond – more as a signal than out of necessity. In the UK, for instance, a symbolic rate hike cannot be ruled out, as policymakers seek to underscore their commitment to the inflation target, even if the case for a full tightening cycle remains weak.

Policy choices will be critical in shaping the trajectory from here. One of the defining lessons from the 2021–22 inflation episode is that policy responses can amplify shocks. The combination of large-scale fiscal support and ultra-loose monetary policy played a key role in transforming an initial supply shock into a broad-based and persistent inflation surge. Today, the policy environment is different – rates are higher, fiscal space is more constrained – but the uncertainty surrounding the duration of the Hormuz disruption complicates the outlook.

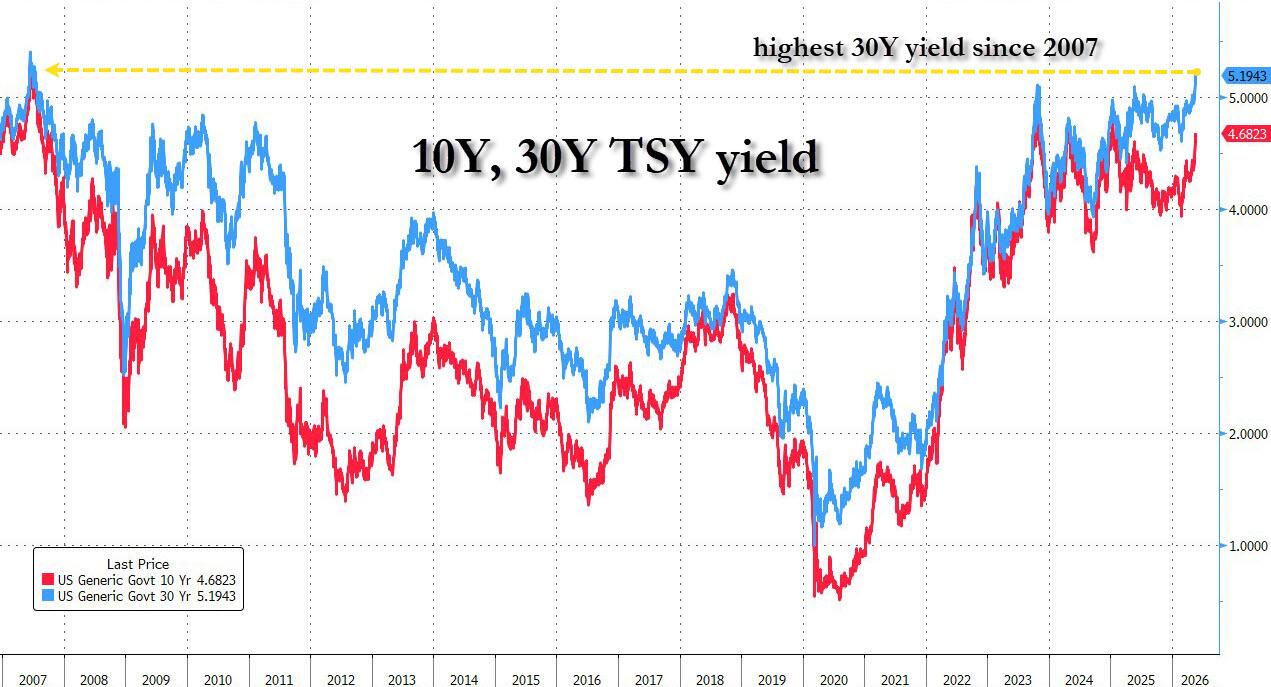

In that context, policymakers may be inclined to assume persistence rather than transience, if only as a precaution. Markets, for their part, have already moved in that direction. Bond yields have repriced sharply higher, particularly at the long end, tightening financial conditions globally. The US 10-year yield rose above 4.67% yesterday, the highest level since mid-January 2025. And although European yields were dragged higher as well, the spread of 10y Treasuries over German bunds has widened from 120bp on 13 April to nearly 150bp yesterday. The rise in US Treasury yields – alongside a widening spread over German Bunds – signals that investors are increasingly focused on both inflation persistence and fiscal sustainability.

This shift in market discipline is not going unnoticed. The IMF has urged Britain to “stay the [fiscal] course” in its ‘Article IV’ consultation. At this week’s G7 meeting, finance ministers and central bankers struck a notably cautious tone, emphasising that any policy support should remain temporary, targeted, and fiscally responsible. Compared to the sweeping interventions seen in recent crises, the response so far has been measured – arguably deliberately so.

Yet this restraint also exposes a tension. While targeted domestic support is relatively straightforward, meaningful international coordination is far more challenging. Countries face competing objectives: protecting domestic growth, ensuring economic security, and enhancing resilience. Measures such as export restrictions may serve national interests but risk undermining collective outcomes. In that sense, the G7’s commitment to cooperation may prove difficult to translate into concrete action.

This suggests a risk of fragile stagflation, with slowing growth alongside persistent inflation. The main danger is not runaway prices but policy errors and poor coordination amid ongoing geopolitical pressures. Much depends on the duration of the Hormuz disruption, as supply shocks may last longer than expected and blur the line between temporary and persistent inflation.

This may also be the reason why we see tentative signs that policymakers are beginning to look beyond purely economic tools. The economic consequences of the Hormuz closure are, after all, rooted in a geopolitical disruption. Discussions within NATO about potentially facilitating maritime passage through the strait underscore a growing recognition that resolving the supply shock itself may be the most effective form of policy response. Although there is no unanimous support yet, according to sources, as per Bloomberg reporting, the fact that NATO is reconsidering an (active) role was seen by investors as a positive development.

Meanwhile, after months of wrangling, the EU finalized the text on the US-EU trade deal, to be signed off by European Parliament and member states before Trump’s 4 July deadline. Reaching a compromise was driven by the overriding objective of “maintaining a stable, predictable and balanced transatlantic partnership”, as put by Cyprus’ minister of commerce. However, the text now includes a 2029 expiration date (unless both sides agree extension). It also includes a clause that would allow the Commission to suspend the deal if tariffs on products using steel and aluminium surpass 15% after 2026 and a ‘pause button’ should the US not keep with its commitments. So let’s see if the US wants to cooperate.