The U.S. is still at least a decade away from meaningfully reducing its dependence on China for the most critical rare earth minerals, despite billions of dollars in new investment and political pledges to move faster, according to a new report from Bloomberg.

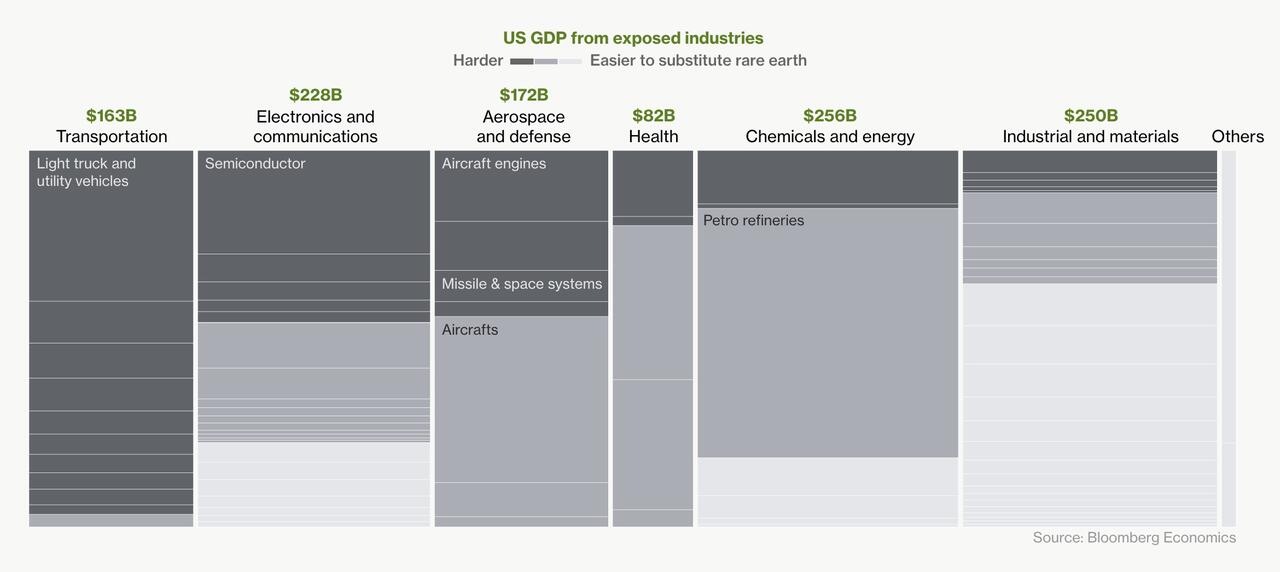

While Washington has pushed to build domestic mining, refining, and manufacturing capacity, analysts say China is likely to retain its dominance over heavy rare earths—particularly dysprosium and terbium—until at least the mid-2030s. Those minerals are essential for the high-performance magnets used in fighter jets, submarines, missiles, electric vehicles, wind turbines, and other advanced technologies.

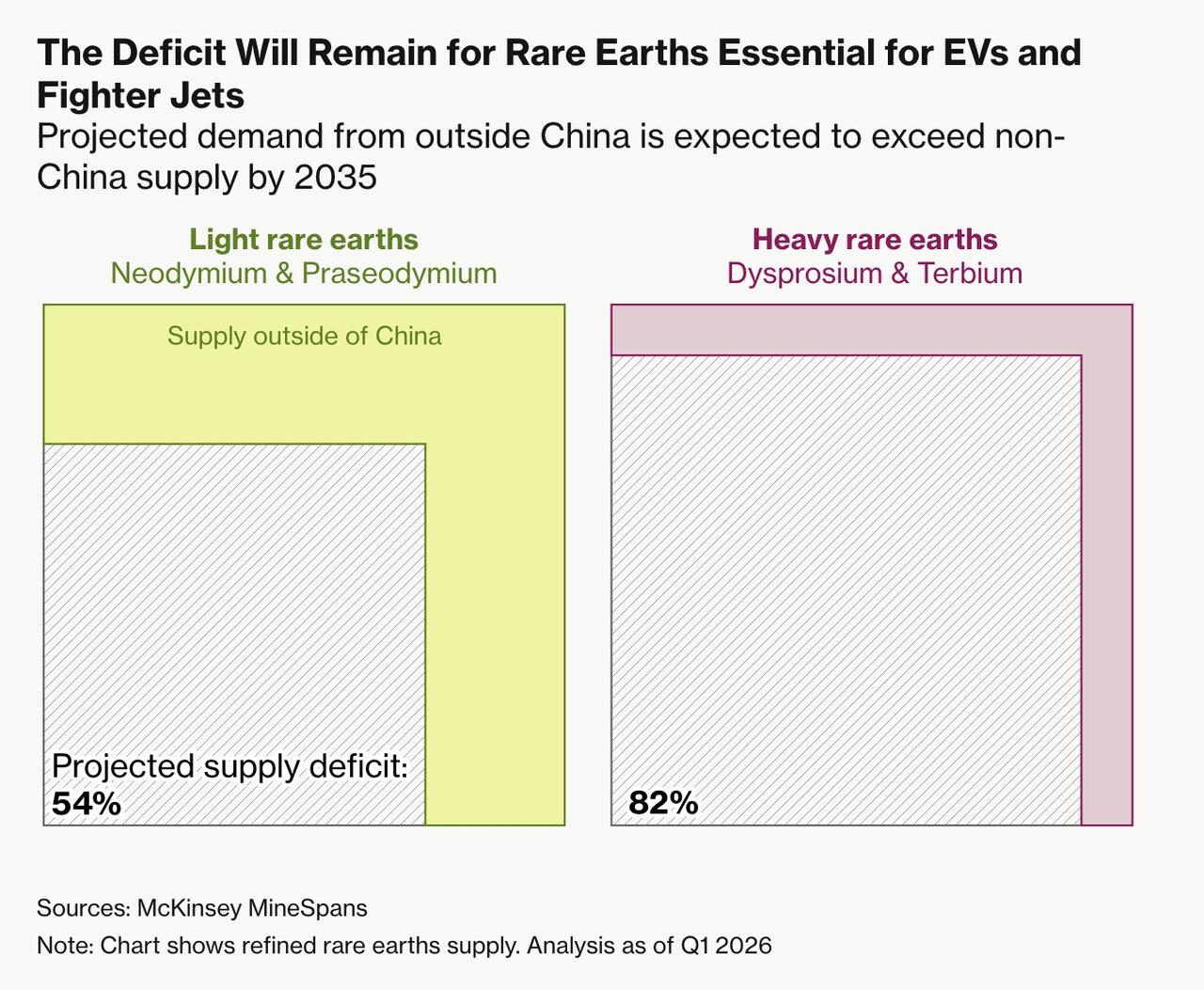

Forecasts from McKinsey & Company, CRU Group, and Benchmark Mineral Intelligence suggest producers outside China will meet less than 20% of global demand for dysprosium and terbium by 2035. The U.S. and its allies may make faster progress in reducing reliance on China for more abundant light rare earths, but the heavier materials remain far harder to replace.

The challenge is not simply digging more minerals out of the ground. Rare earth production involves mining ore, separating it into oxides, and then converting those materials into metals and magnets...a supply chain China dominates at nearly every step.

Heavy rare earths are especially difficult because they are less abundant and far more complex to refine. Producing ultra-pure material can require more than 1,000 chemical separation stages, and even small mistakes can affect magnet performance. Over decades, China built a deep advantage through refining infrastructure, technical expertise, and government-backed industrial policy. It also restricted exports of certain processing technologies, making it harder for competitors to catch up. The U.S., by comparison, has only a small pool of specialists with experience in rare earth separation and processing.

Bloomberg writes that Washington has begun investing heavily to rebuild domestic capacity, including Pentagon support for Lynas Rare Earths Ltd., currently the only commercial refiner of heavy rare earths outside China.

But production remains limited. Lynas produced just eight tons of dysprosium and terbium combined in the first quarter of 2026, while global demand is measured in thousands of tons each year. New projects in the United States, Australia, and Brazil could expand supply, but analysts still expect significant shortages in mining, refining, and magnet manufacturing by 2035.

China’s lower production costs have made the market even harder for rivals; past price swings wiped out many non-Chinese projects before they could scale. That leaves the U.S. facing a long and expensive effort to loosen China’s hold over a supply chain that has become increasingly important to both economic competitiveness and national security.