An unexpected development over the past few weeks is xAI's new partnerships with Anthropic and Google, providing them with a huge amount of capacity. It's worth remembering that xAI is now part of SpaceX, after the two merged back in February - so the revenue from these deals flows straight into the entity about to go public. While much has been made of the potential financial engineering given SpaceX's upcoming IPO, I think there's a bit more to this than just pure accounting tricks.

Anthropic was in a serious bind

If you use Claude products much, you'll be (very, probably) aware that Anthropic has had serious capacity problems, especially early afternoon onwards in Europe and in the mornings in the US (this is when demand seems to be highest as both European users and the Americas are both at work, fighting for capacity). I've written about this compute crunch before a few times - the coming crunch, whether it's here yet, and what comes next.

This resulted in Anthropic having to introduce new peak hour restrictions on their subscriptions, with usage between 5am–11am PT / 1pm–7pm GMT using more of your usage limit - with the aim of smoothing demand between peak hours and off peak hours where they had more capacity available.

However, there is only so much demand shifting you can do when demand is growing as fast as Anthropic's. At some point you end up having to ration users further, which definitely is far from ideal when you have both Google and OpenAI breathing down your neck for customers.

xAI to the rescue?

At the start of May, xAI announced a partnership with Anthropic to provide access to their (older) Colossus 1 datacentre in Memphis. This allowed Anthropic to reverse the usage limit restrictions on their subscriptions, and in general while stability of Anthropic services still leaves a lot to be desired, the peak time crunch has abated (for now, at least).

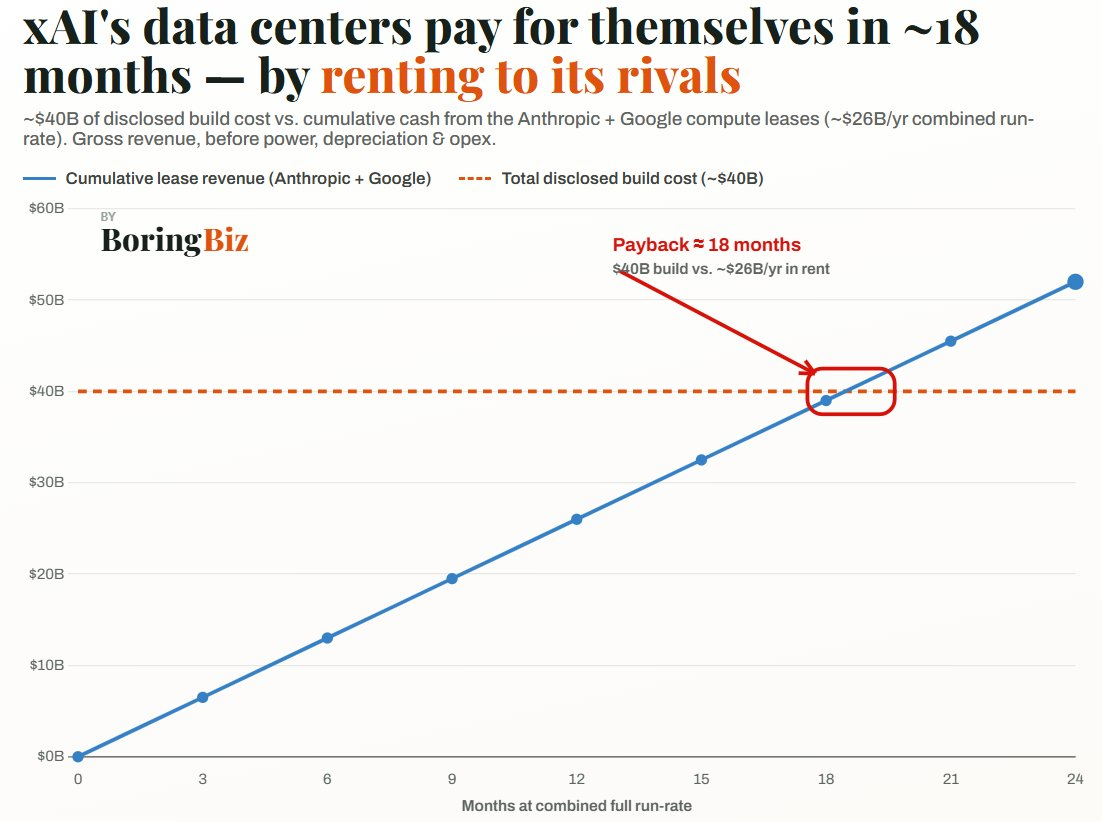

The fees involved are enormous, ramping to $1.25bn/month for 300MW of capacity - approximately 220k GPUs.

Last week, Google announced a similar partnership - $920mn/month for 110k GPUs. It's important to note that both agreements have cancellation clauses - allowing either party to cancel with 90 days' notice after an initial lock-in period.

If you take this on face value, this is a ludicrously profitable deal for xAI:

While this doesn't include opex and depreciation, if the deals continue for 18 months, xAI recoups all the capex they spent and still has many hundreds of MW of GPUs available. With the giant compute shortages likely to persist into the medium term, even older H100s are likely to be extremely useful even 18 months out.

The case against

It's important to note there are certainly some red flags with the deal. Firstly, Elon Musk and OpenAI were/are locked in a bitter legal battle, and the Anthropic deal could be motivated to add pressure to OpenAI more than commercial reality.

And Google is a major shareholder in SpaceX, so they certainly have incentive to juice the valuation of the IPO.

While I'm sure there is some degree (potentially a lot!) of truth in these viewpoints, it's important to note that huge volumes of GPUs are in enormously short supply.

One of the untold stories of this capex boom in datacentres is just how behind all of them are. Even OpenAI's flagship Stargate UAE datacentre - being built in a jurisdiction that is renowned for a laissez-faire attitude to building regulations - is now under direct threat from the current Iran conflict, with Iranian drones having already hit other UAE datacentres.

In comparison, SpaceX/xAI are incredible at building datacentres on time. The original Colossus 1 datacentre was built in 122 days. Musk's empire does have a huge advantage in really understanding how to plan, build and execute enormous infrastructure projects quickly. While the hyperscalers no doubt have the experience to do this, they were built with far less urgency - with typical project execution taking many years. Given the capex only really started to ramp up in the last couple of years, many of these projects are still years away.

This gives xAI a serious competitive advantage that shouldn't in my opinion just be hand waved away.

But what about Grok?

There is no doubt this leaves Grok in an odd spot, with a lot of the datacentre capacity that was destined for Grok training and inference now being leased to a direct competitor.

While it's foolish to write off any model provider, it certainly looks like a serious retreat from Grok vying to be a frontier class lab. But, perhaps, they over-specified their datacentre capacity - there is no doubt that inference demand for Grok models is likely to be seriously behind projections, leaving a bunch of spare capacity which might as well be monetised while the training lottery continues? It's hard to say and the xAI & Cursor deal muddies the water even further.

As such, I think all three things are true to some degree. There's no doubt some level of financial engineering going on. There's also an enormous compute shortage. And it seems to me SpaceX/xAI does have a real competitive advantage in datacentre buildout.

It's just the magnitude of how true each of these are is going to define the success or failure of the biggest IPO in North American history.

Either way, the more I look at it, the more xAI is starting to resemble a datacentre REIT with a frontier lab attached, rather than the other way around.