Authored by Rystad Energy via OilPrice.com,

-

The end of the Russia-Ukraine gas transit agreement in 2024 will disrupt gas supplies to several European countries, particularly Slovakia, Austria, and Moldova.

-

To replace Russian gas, the EU will need to increase LNG imports and utilize alternative pipelines, such as the Trans-Balkan pipeline and the Balkan Stream.

-

Central and Eastern European countries are collaborating on the Vertical Gas Corridor initiative to enhance energy security and diversify gas supplies.

The European Union (EU) targets a ban on Russian fuel imports by 2027. However, nearly half of Russia's pipeline gas supplies to Europe and Moldova are still passing through Ukraine, totaling 13.7 billion cubic meters (Bcm) in 2023. As the EU discusses the possibility of involving Azerbaijan in a future transit deal, the current five-year gas transit agreement between Russia and Ukraine is set to expire by the end of 2024, leading to concerns about the future flow of these gas volumes. Rystad Energy predicts that Russia's gas will need to be rerouted to Europe through alternative paths, requiring an additional 7.2 Bcm per year of liquefied natural gas (LNG) to replace the gas transiting Ukraine. Supply disruptions may occur sooner than initially expected, as indicated by the Austrian company OMV’s market warning in May.

Slovakia, Austria and Moldova are the European nations most dependent on transit volumes, importing about 3.2 Bcm, 5.7 Bcmand 2.0 Bcm, respectively, in 2023. Last year, Russian gas passing through Ukraine supplied EU countries via entry points in Slovakia and Moldova. Moldova is adjusting its supply while having agreed with Ukraine on a continuous flow of Russian gas until the end of 2025, largely supplied to the pro-Russia separatist region of Transnistria. In 2023, the country imported 74% of its gas through Ukraine and, for the first time, received gas from Romania and the south through reverse flows via the Trans-Balkan pipeline. Italy's energy company Eni and Hungary also imported Russian gas through Ukraine, while Slovenia and Croatia have been smaller takers of Russian gas via Ukraine.

Halting Russian gas pipeline flows via Ukraine would significantly impact countries relying on these volumes. For example, when the transit extension expires after 2025, Moldova would need to reroute its 2 Bcm supplied via Ukraine, possibly through reverse flows of the Trans-Balkan pipeline. To reach Moldova, Russian gas could use the Isaccea entry point between Romania and Ukraine, but a transit agreement for the short 25-kilometer distance through Ukraine would be required. The Trans-Balkan pipeline has been operated in reverse flow since the end of 2022, with 0.54 Bcm of gas entering Moldova via Ukraine from Romania through the Isaccea entry point in 2023. Additionally, gas from the Southern Gas Corridor in Azerbaijan, as well as from Turkish and Greek LNG import terminals, can reach Moldova via the south. When the Russia-Ukraine transit agreement ceases, the only alternative supply routes for Central and East European countries would be the Balkan Stream and the Horgos entry point between Serbia and Hungary.

Russian producer Gazprom and European importers are keen on continuous supplies via Ukraine, while Ukrainian officials deny any intention for a renewed agreement with Russia. Without Azerbaijan or another third party transiting the gas following a swap deal with Russia, the EU will require about 7.2 Bcm of gas to be sourced from the LNG market. Terminals in Poland, Germany, Lithuania and Italy could forward these volumes to the most affected counties, such as Slovakia and Austria,

Christoph Halser, Gas & LNG Analyst, Rystad Energy

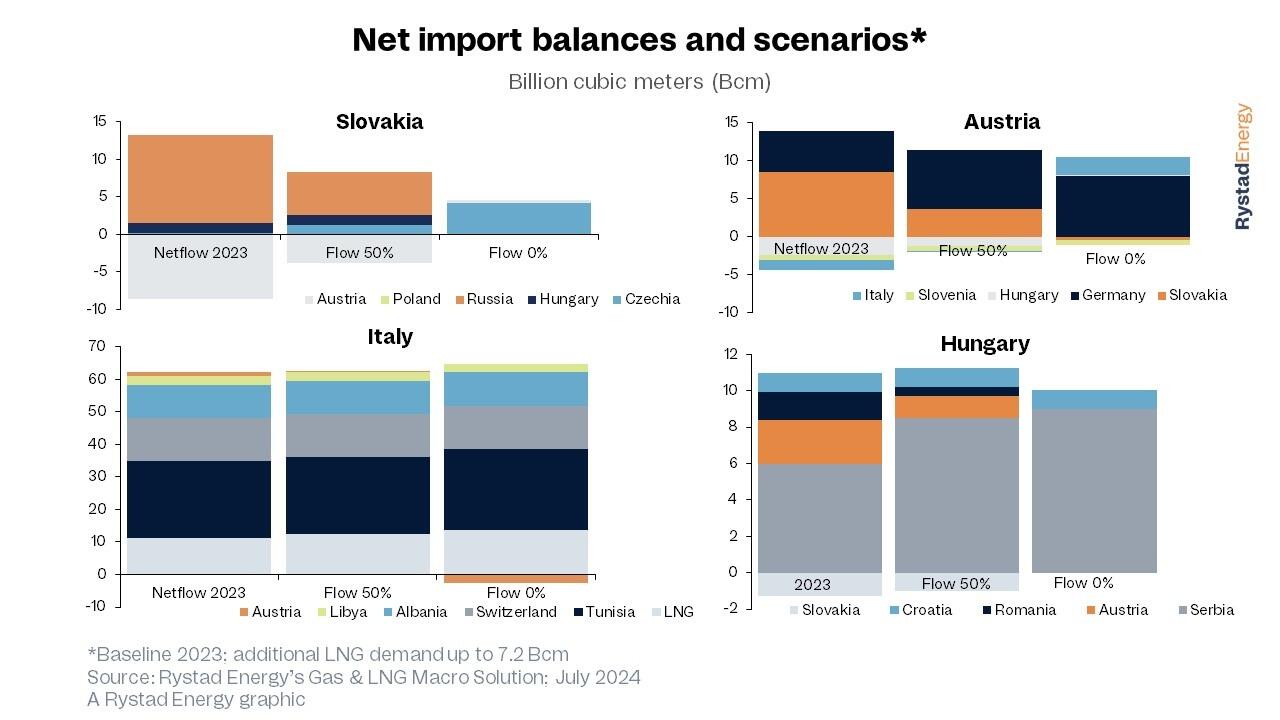

Rystad Energy forecasts potential changes to the 2023 gas balance for affected countries under the assumption of 50% and 0% flow of gas via Ukraine and capacity limitations at relevant entry point alternatives. Without Russian gas, Slovakia would find itself at the end of the flow chain, requiring about 4 Bcm of gas delivered through the Lanzhot entry point from Czechia. With additional regasification capacity in Poland only available in 2025, a zero-flow scenario may even entail reverse flows from Austria into Slovakia.

Austria, the largest offtaker of Russian gas in 2023, would pivot towards increasing imports from Germany via the Oberkappel entry point, expected to operate at a maximum annual capacity of 8 Bcm. However, for Rystad Energy’s baseline year of 2023, the import capacity at Oberkappel will not be sufficient to close the 8.53 Bcm import gap. Without short-term capacity adjustments, gas transits to Hungary would decline, and outflows to Italy would be stopped. If all Russian gas flows via Ukraine were to cease, Austria would need to import up to 2.5 Bcm from Italy via the Arnoldstein-Tarvisio crossing point.

Italy has several options to replace Russian gas pipelines and has largely achieved independence from the Ukrainian transit. However, the country would be required to source about 3.75 Bcm for Slovakia and Austria. These additional supplies could come from the Ravenna floating storage and regasification unit (FSRU) —5 Bcm per year from 2025—and 1.23 Bcm from pipeline supplies through Tunisia.

Hungary would face large challenges in case of a complete halt of Russian gas flow through Ukraine. Assuming Moldova is supplied via the south, capacity via the Trans-Balkan pipeline from Romania would be fully allocated, halting inflows from Romania. Furthermore, Austria would be unable to forward gas to Hungary, while Croatia won't have additional regasification capacity available before 2025. Hungary would have to rely solely on increased gas flow through the TurkStream pipeline, whereby the Horgos entry point would be required to operate continuously at its maximum capacity of 9 Bcm per year. Alternatively, if Austria could source sufficient LNG from Italy, Hungary could receive additional gas through reverse flows at the Mosonmagyarovar entry point from Austria.

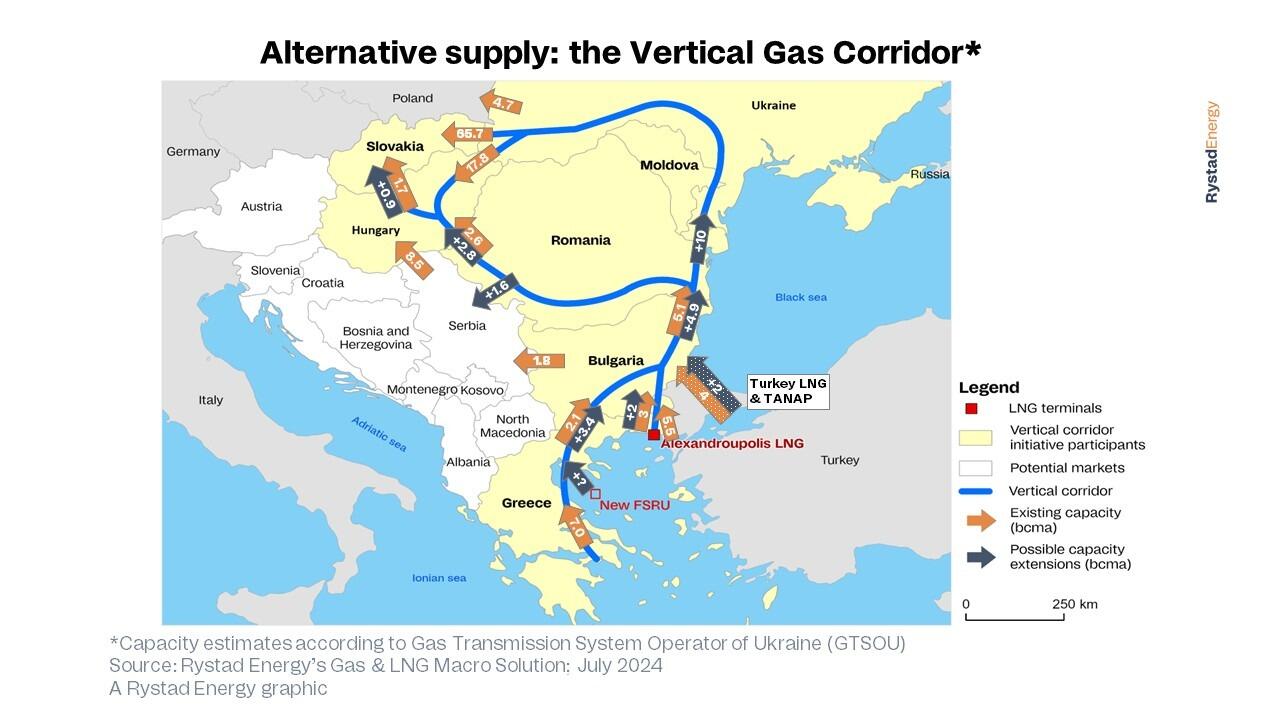

Central and Eastern European countries are preparing for a possible halt in the Ukraine gas transit and have joined forces to create a Vertical Gas Corridor under the EU's Central and South Eastern Europe Energy Connectivity Initiative (CESEC). This year, on 19 January, a memorandum of understanding (MoU) was signed in Athens involving EU energy commissioner Kadri Simson and the Transmission System Operators (TSOs) from Greece, Bulgaria, Romania, Hungary, Slovakia, Ukraine and Moldova. The corridor would utilize existing infrastructure in Ukraine and Moldova and enable LNG imports from Greece and Turkey to reach Slovakia, Hungary and possibly Poland.

Furthermore, Turkey's transmission system operator BOTAS and Bulgaria's operator Bulgartransgaz signed an agreement in January 2024 to increase gas entry capacity at the Strandzha 1 entry point, enabling increased gas flows from Azerbaijan and the Caspian Sea region into Europe. This expansion could aid in raising Azerbaijan's EU gas exports from 13 Bcm to 20 Bcm per year by 2027 and, in the long run, potentially transport Iranian gas through the Solidarity Ring Initiative.

Learn more with Rystad Energy’s Gas & LNG Solution.