Here’s a puzzle: how do you create a trillion-dollar debt bubble that can’t be popped? Answer: make student loans non-dischargeable in bankruptcy.

Now, here’s a trickier one: how do you fix this mess when the solution threatens a multibillion-dollar industry?

This isn’t just a theoretical exercise.

It’s the reality we’re living in.

The U.S. student loan system is a perfect storm of misaligned incentives, regulatory capture, and unintended consequences.

The solutions are surprisingly straightforward – make loans dischargeable, tie lending to degree value, hold institutions accountable.

But implementing them?

That’s where things get complicated.

You see, there’s a reason this broken system persists.

It’s not just inertia or incompetence.

It’s because there are powerful, entrenched interests that profit handsomely from the status quo. They cloak themselves in the noble rhetoric of education, but their actions tell a different story: skyrocketing tuition, subpar outcomes, and a generation drowning in debt.

It’s not about enlightenment; it’s about enrichment – theirs, not yours.

The Numbers Don’t Lie

The results were predictable, if you knew where to look. In 2003, total student loan debt was around $250 billion. Today? It’s over $1.7 trillion.

That’s not growth; that’s an explosion.

But here’s the real kicker: this debt isn’t just a personal burden. It’s propping up a deeply flawed system.

The results are insidious:

- Millions of Americans graduate from college overloaded with debt and underprepared for the job market.

- The institutions that create these outcomes are not held to account because market forces are not at play.

- Colleges have no incentive to control costs or improve outcomes, as they get paid regardless.

- Lenders keep issuing loans without regard for the borrower’s ability to repay, knowing the debt can’t be discharged.

In essence, the non-dischargeability of student loans has created a perfect storm of misaligned incentives. It’s a system that rewards failure and punishes success.

Consider these facts:

- Only 41% of college students graduate within 4 years, yet colleges face no consequences for low completion rates.[1]

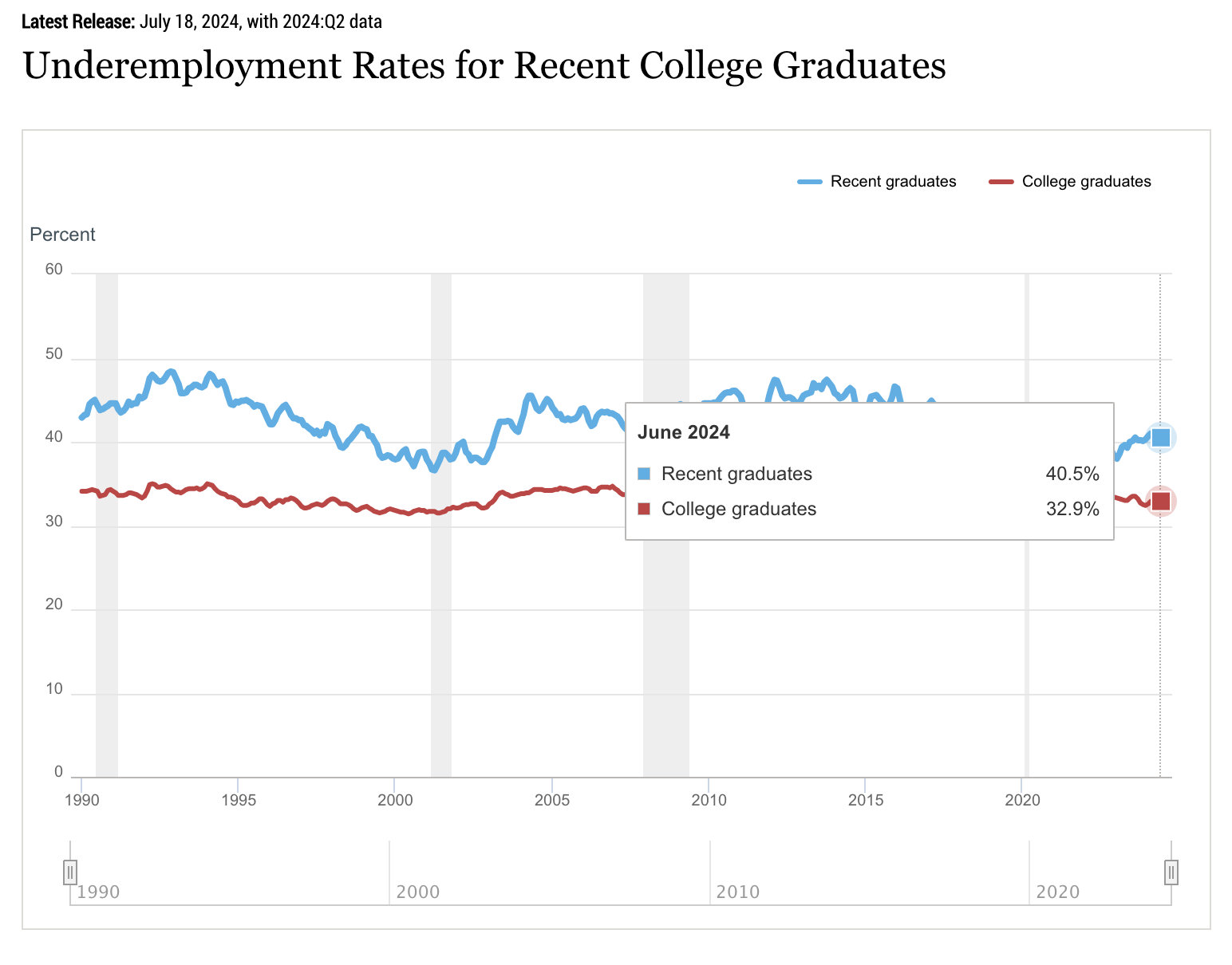

- The average student loan debt for the Class of 2023 is $37,574, but 43% of recent graduates are underemployed in their first job.[2][3]

- Despite skyrocketing tuition, only 60% of college graduates feel their education was worth the cost.[4]

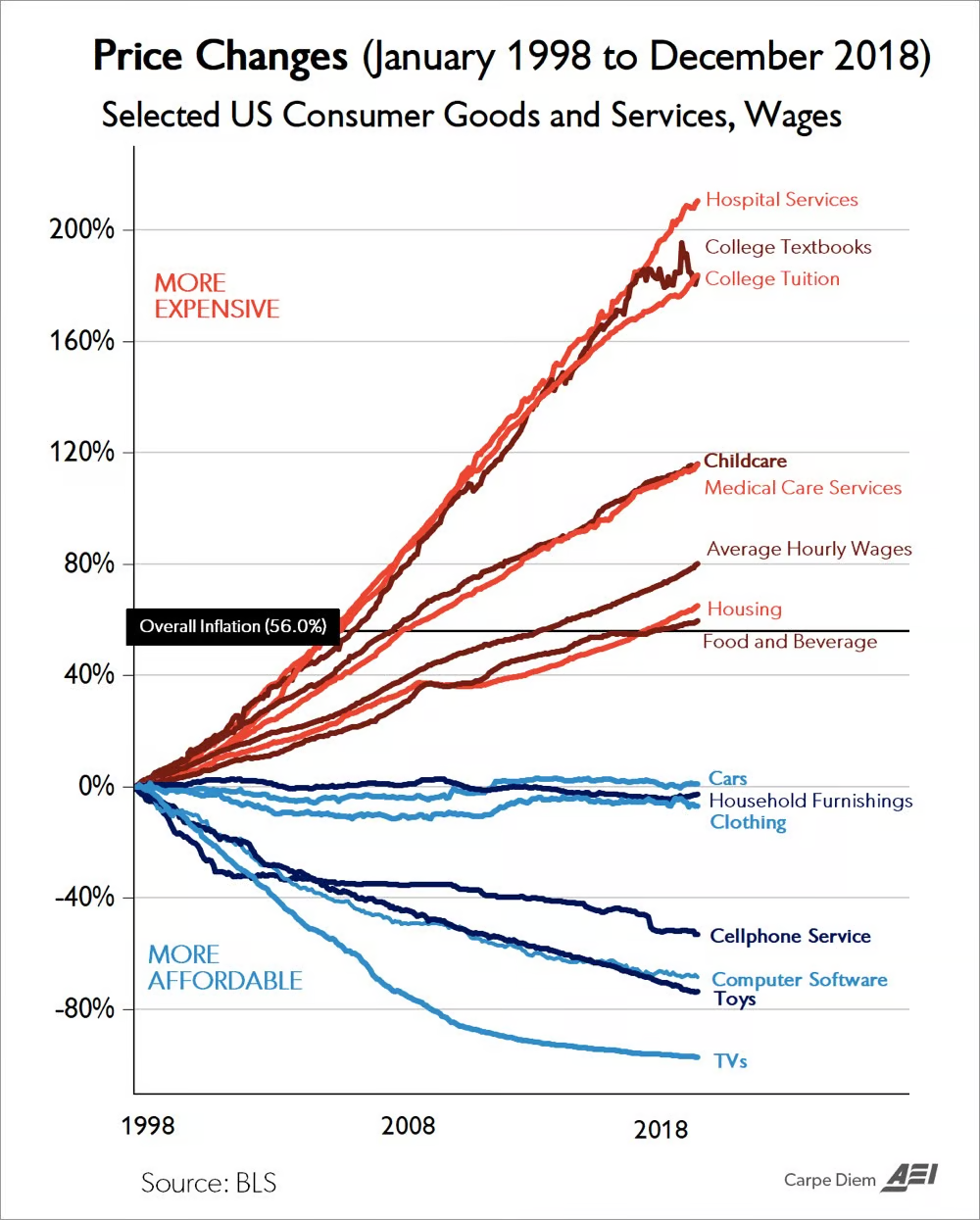

- From 1980 to 2020, the cost of college tuition increased by 180%, while the quality of education and job market preparation have not seen comparable improvements.[5]

These aren’t just numbers. They’re evidence of a system that’s fundamentally broken.

The Institutional Shield

But why don’t market forces correct these issues?

The answer lies in the unique shield that non-dischargeable student loans provide to educational institutions and lenders.

In a normal market, if a product consistently fails to deliver value, consumers stop buying it. Producers either improve or go out of business. But in the world of higher education, this feedback loop is broken.

Colleges and universities, shielded by the guarantee of student loan money, have no real incentive to improve their product or direct students to majors that have an ability to pay back their loans.

They can raise tuition year after year, even as the value of their degrees stagnates or declines.

They can offer degrees with poor job prospects knowing that students will still come—and still be able to borrow.

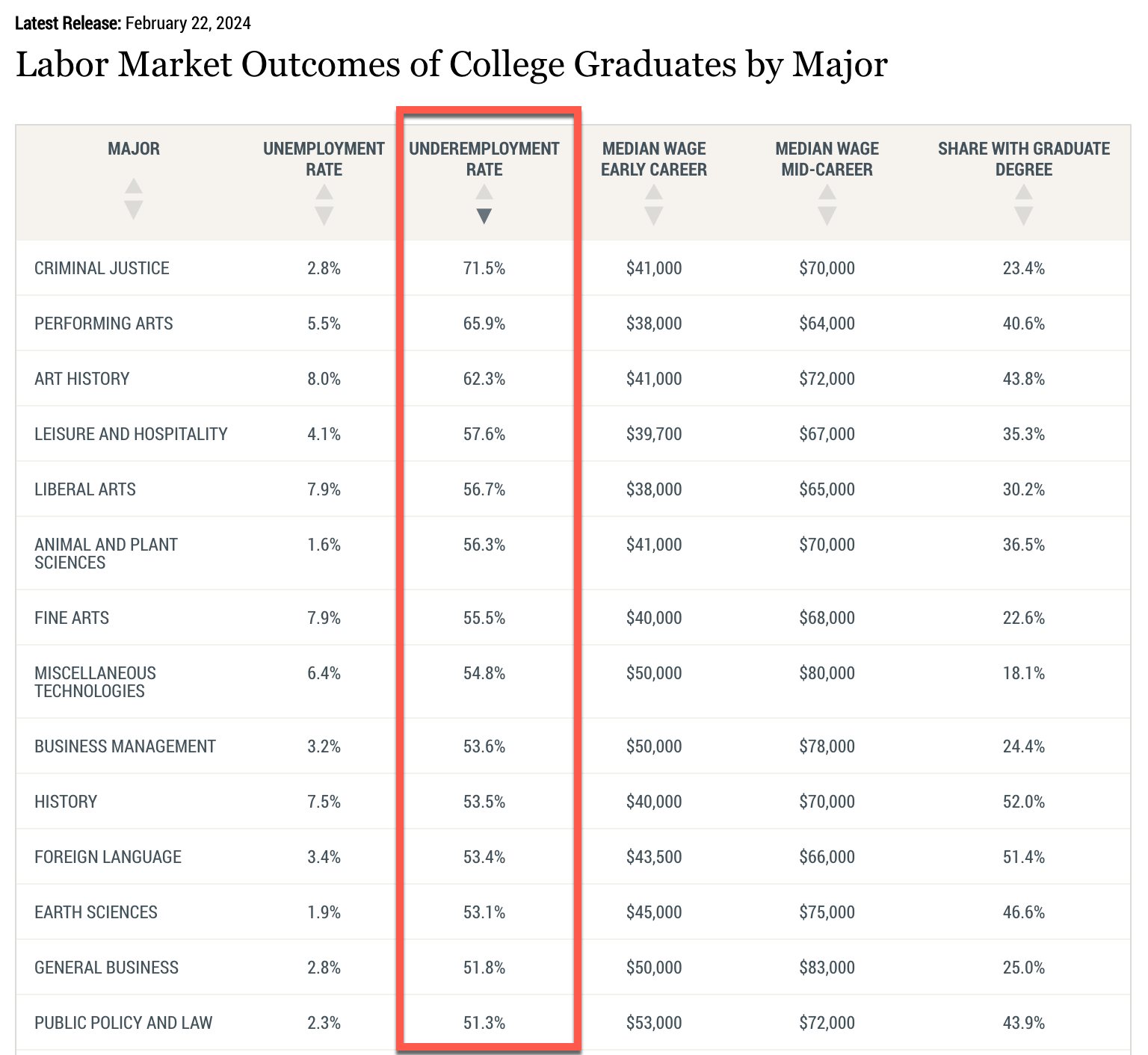

This data by the NY Fed highlights the majors with the worst underemployment, i.e. graduates working in jobs that don’t require a degree. Criminal justice, performing arts and art history have an over 60%+ underemployment rate with performing arts and art history majors being upsold into graduate school piling on even more debt.

Meanwhile, lenders—both government and private—keep the money flowing. Why wouldn’t they? With loans that can’t be discharged in bankruptcy, they’re guaranteed a return, even if it takes decades to collect.

This perverse system means that the very institutions that should be preparing students for success are instead setting them up for a lifetime of debt. And they’re doing it with impunity.

But Wait, There’s More!

In a twist that would be comical if it weren’t so cruel, these loans can follow borrowers into retirement, threatening the very safety net meant to protect them.

Yes, you read that right.

The federal government can and does garnish Social Security benefits to repay defaulted federal student loans.[6] Up to 15% of a person’s Social Security check can be seized, though the government must leave the borrower with at least $750 a month.

Let that sink in for a moment.

The system is so ruthless in its pursuit of repayment that it’s willing to take money from retirees’ already modest Social Security checks.

It’s a stark reminder that in the world of student loans, there’s no such thing as a fresh start.

Not even in your golden years.

Consider these sobering facts:

- As of 2015, 114,000 older Americans had their Social Security benefits garnished due to defaulted student loans.[7]

- The number of Americans aged 60 and older with student loan debt quadrupled from 2005 to 2015.[8]

- Nearly 40% of federal student loan borrowers aged 65 and older are in default.[9]

This isn’t just a young person’s problem anymore. It’s a crisis that spans generations, threatening the financial security of Americans from cradle to grave.

The Birth of a Monster

The road to hell is paved with good intentions, and the student loan crisis is no exception.

It started innocently enough in 1976 with the Education Amendments. The goal? Prevent students from gaming the system by declaring bankruptcy right after graduation. Seems reasonable, right?

But then came the creep.

Five years of non-dischargeability became seven.

Then, in 1998, it became forever.

The final nail in the coffin was the 2005 Bankruptcy Abuse Prevention and Consumer Protection Act, which extended this rule to private student loans.

Suddenly, lenders had a captive market.

No matter how bad things got, borrowers couldn’t escape.

It was a lender’s dream and a borrower’s nightmare.

The Unseen Victims

But the damage goes beyond the obvious. Student loan debt is a silent killer of American competitiveness and risk-taking.

The reality is we’re churning out millions of graduates with no discernible skills drowning in debt. 4 in 10 per the NY Fed are underemployed working in retail or as baristas making zero use of their criminal justice degrees.

Smart graduates laden with debt also can’t afford to take risks. They can’t start businesses. They can’t buy homes. They can’t invest in their futures. They’re too busy paying for their past.

And it’s not just individuals who suffer. The entire economy takes a hit. When a significant portion of the population is funneling its income into loan payments rather than spending or investing, it’s a drag on everyone – even those who never set foot in a college classroom.

The Entrenched Powers

Now, you might be thinking: “This is clearly broken. Why hasn’t it been fixed?”

The answer is as old as politics itself: follow the money.

The student loan system has created a powerful alliance of interests:

- Colleges and Universities: They get guaranteed money, regardless of the quality of education they provide.

- Lenders: They get guaranteed returns, backed by the full faith and credit of the U.S. government.

- Politicians: They get donations from the first two groups, ensuring the status quo remains intact.

This unholy trinity has no incentive to change the system. In fact, they have every reason to keep it exactly as it is.

The Way Out

So, what’s the solution? It’s simple, but not easy:

- Make student loans dischargeable in bankruptcy again.

- Tie lending terms to the value of the degree.

- Impose risk-sharing requirements on educational institutions – Schools would face financial penalties or need to contribute to a risk-sharing pool if their graduates default at high rates.

But here’s the rub: implementing these changes would cause a massive shake-up.

Colleges would have to rethink their entire financial models. They’d have to rethink the majors they offer, their tuition fees and have to dramatically reduce their administrative bloat.

Lenders would face actual risk. Politicians would lose a reliable source of campaign contributions.

In other words, the very people who have the power to fix the system are the ones who benefit from keeping it broken.

The Fork in the Road

We’re at a crossroads.

We can continue down this path, creating a permanent debtor class and stifling economic growth. Or we can make the hard choices necessary to create a sustainable, equitable system of higher education.

The choice is ours.

But make no mistake: the clock is ticking.

Every day we delay, another student signs on the dotted line, committing to a lifetime of debt they will likely never escape.

—-

If you read this far, some related essays you might like:

- Harvard: The Birkin Bag of Education

- Your kids grades are bullshit

- The School of Entrepreneuring

- The perverse incentives driving America’s government schools

- Bread, circuses and education

- The endless ladder

- Solving the wrong problems

Sources

[1] National Center for Education Statistics. (2022). Undergraduate Retention and Graduation Rates. https://nces.ed.gov/programs/coe/indicator/ctr

[2] Education Data Initiative. (2023). Student Loan Debt Statistics. https://educationdata.org/student-loan-debt-statistics

[3] Federal Reserve Bank of New York. (2020). The Labor Market for Recent College Graduates. https://www.newyorkfed.org/research/college-labor-market/college-labor-market_underemployment_rates.html

[4] Strada Education Network. (2020). Public Viewpoint: COVID-19 Work and Education Survey. https://www.stradaeducation.org/wp-content/uploads/2020/12/Report-December-21-2020.pdf

[5] National Center for Education Statistics. (2021). Digest of Education Statistics, Table 330.10. https://nces.ed.gov/programs/digest/d21/tables/dt21_330.10.asp

[6] U.S. Department of Education. (2023). Collections. https://studentaid.gov/manage-loans/default/collections

[7] Government Accountability Office. (2016). Social Security Offsets: Improvements to Program Design Could Better Assist Older Student Loan Borrowers with Obtaining Permitted Relief. https://www.gao.gov/assets/gao-17-45.pdf

[8] Consumer Financial Protection Bureau. (2017). Snapshot of older consumers and student loan debt. https://files.consumerfinance.gov/f/documents/201701_cfpb_OA-Student-Loan-Snapshot.pdf

[9] U.S. Department of Education. (2021). Federal Student Loan Portfolio by Borrower Age. https://studentaid.gov/data-center/student/portfolio