By George Lei, Bloomberg Markets Live reporter and strategist

The US dollar suffered its worse selloff since mid-July last week, bringing some relief to China’s policymakers. With the world’s second-largest economy effectively pegging the yuan to the greenback, Beijing can ride the likely wave of dollar weakness that will also see the Chinese currency depreciate on a trade-weighted basis.

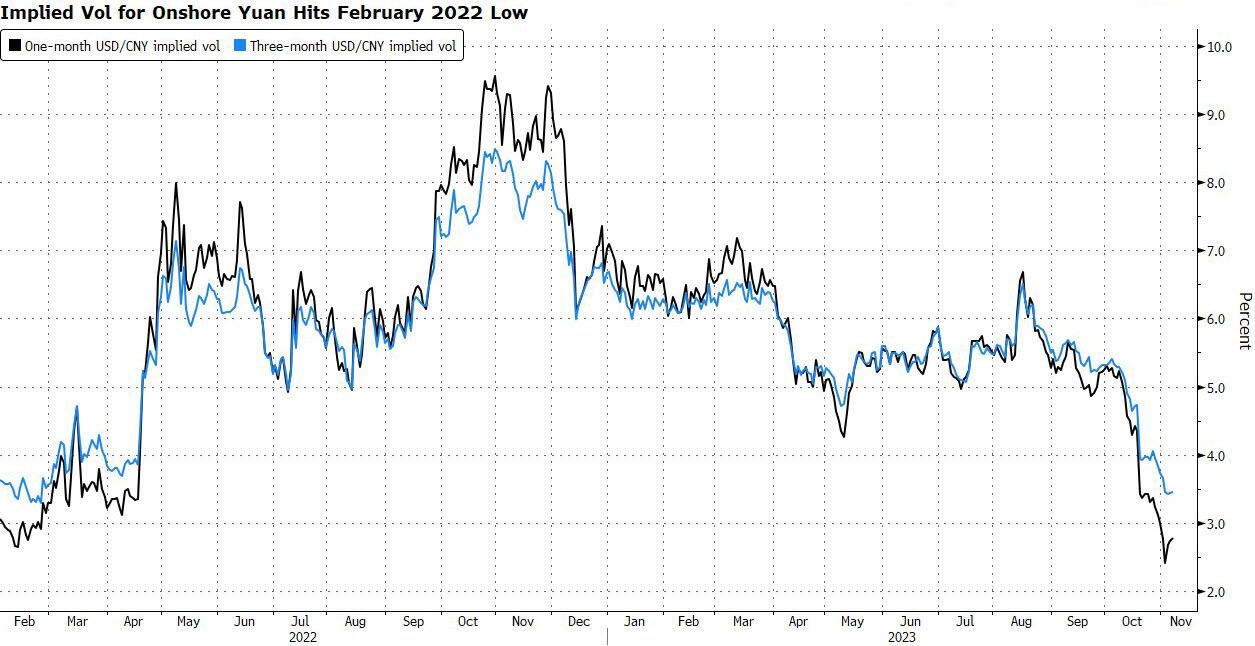

Dollar-yuan has traded around 7.30 since mid-August in both onshore and offshore markets: fluctuations, either upward or downward, have been less than 1%. The steady hand of PBOC helped suppress one-month implied volatility on the onshore yuan below 3%, to the lowest since February 2022. In offshore trading, where PBOC has relatively less clout, one-month implied vol is now lower than 4%, at levels last seen in April 2022.

PBOC’s favorite tool for stabilizing the dollar-yuan exchange rate is its daily fixing. The Chinese central bank has kept such a tight grip on the reference rate, sending its volatility to almost zero, something that last took place 13 years ago. From the onset of global financial crisis in 2008 to the middle of 2010, Chinese authorities essentially pegged their currency at 6.82 per dollar.

Suppressing swings in the dollar-yuan exchange rate is the main route on the road to financial stability. But with it comes side effects that can create headwinds for an economy struggling to recover.

Between mid-July and early-October, the Bloomberg dollar spot index rallied almost 7% from its 2023 low to high. While the yuan declined against the dollar over the same period, on a trade-weighted basis it advanced nearly 4%. That’s because the Chinese currency held up much better against the greenback than other currencies under the PBOC’s support.

Now, should the weakening dollar trend persist, the yuan will likely follow suit on a trade-weighted basis, helping boost the country’s competitiveness.

“It would be too early to declare victory in preserving RMB stability and PBOC will likely phase out its FX policy support gradually,” Ken Cheung, chief asian FX strategist at Mizuho Bank Ltd. said in a client email on Monday. While outflows from onshore equities have moderated recently, China’s property market is still not out of the woods yet and the growth outlook remains generally bearish, Cheung noted.

While the PBOC has practically left yuan’s daily fixings flat, the currency has kept trading on the weaker side over the past couple months, sometimes pushing the boundaries set by policymakers (yuan is only permitted to deviate a maximum 2% away from the reference rate in onshore trading). If the PBOC were to loosen its grip, market equilibrium will probably imply a much weaker Chinese currency despite a falling US dollar.

Bearish dollar moves are “likely to do much of the work” for the PBOC, which makes it less likely for policymakers to “give up on their defense of the currency,” according to a research report from JPMorgan on Friday. The US bank believes a large downside move in dollar-yuan is unlikely given the easing policy stance, and favors selling 3-month volatility for USD/CNH.