As we arrive at a new week, DB's Henry Allen writes that the focus is still on Ukraine this morning, as the world reacts to the Trump-Putin summit in Alaska last Friday. The main headline was that no deal was reached on a ceasefire, but multiple outlets reported that Putin wanted Ukraine to withdraw from the Donetsk and Luhansk regions, and he offered Trump a freeze across the rest of the frontline in return. Moreover, Trump himself posted that he now wanted to “go directly to a Peace Agreement, which would end the war, and not a mere Ceasefire Agreement, which often times do not hold up.”

After the summit, Trump then spoke with European leaders, although the joint statement from the European leaders made clear that “It will be up to Ukraine to make decisions on its territory.” Then today, Trump is meeting President Zelensky at 1:15pm ET, before a multilateral leading with European leaders at 3:00pm ET. That group will include UK PM Starmer, French President Macron, German Chancellor Merz and Commission President Von der Leyen. In his post, Trump also said that “If all works out, we will then schedule a meeting with President Putin.”

Clearly, we’ll have to wait and see what happens today, but Trump was saying yesterday morning that there had been “BIG PROGRESS ON RUSSIA. STAY TUNED!” And separately, Trump’s envoy Steve Witkoff said on CNN that “We got to an agreement that the US and other nations could effectively offer Article 5-like language to Ukraine”, which is the NATO article which says that an attack on one member will be considered an attack on all. Trump has also been calling on Zelensky to make a deal, and just a few hours ago, he posted that Zelensky “can end the war with Russia almost immediately, if he wants to, or he can continue to fight.” However, US Secretary of State Marco Rubio downplayed expectations of a deal yesterday, saying that “We are not at the precipice of a peace agreement.”

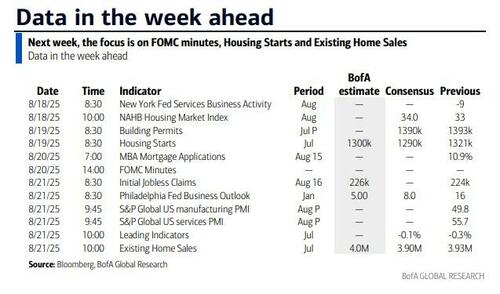

In terms of the week ahead, the main focus away from the White House will be the Fed’s symposium at Jackson Hole, where we’ll hear central bankers including Fed Chair Powell and ECB President Lagarde. Bear in mind that the Fed Chair’s speech at Jackson Hole has often been used to send important policy signals, and it was last year that Powell said the “time has come for policy to adjust” before they then cut rates at the next meeting for the first time since the pandemic. This time around, we don’t have the full agenda yet, but the subtitle for Powell’s speech on the Fed’s website says “Economic Outlook and Framework Review”, so we can expect some insight on those topics.

The last time the Fed had a review in 2020, that resulted in a shift towards average inflation targeting. In essence, they said that after periods when inflation had been persistently beneath 2% (like the 2010s), then monetary policy could seek to reach inflation a bit above 2% to counteract that. The Fed also reinterpreted their approach to full employment, in that a tight labor market alone wasn’t a reason to raise rates. So that implied a move away from the pre-emptive approach whereby the Fed would tighten policy to get ahead of future inflation as the labour market tightened. Of course, we now know that shortly after the framework review, there was then a major burst of inflation, and although it had many drivers, our US economists concluded in a Friday note (link here) that the new framework was a contributor to that overshoot. So this time around, they expect Powell’s speech to call for rolling back the 2020 modifications and restoring a primary role for pre-emption.

When it comes to the near-term path for policy, futures are still pricing in a September rate cut as the most likely outcome. But there was a clear shift last Thursday, as the PPI inflation release for July showed the fastest monthly inflation since March 2022. So that made it clear that a September cut still wasn’t a done deal, particularly with the emerging signs of tariff-driven inflation. And we still know there’s more to come on the tariff front, as Trump said on Friday that he'd be “setting tariffs next week and the week after, on steel and on, I would, say chips — chips and semiconductors, we’ll be setting sometime next week, week after”. So that’s one to keep an eye on, and Trump also suggested that the semiconductor rate could be as high as 300%.

Staying on inflation, we’ve got some more releases out this week, including from Japan, the UK and Canada. The UK will be an important one, as the June reading was unexpectedly strong, with headline inflation rising to +3.6%. Moreover, our UK economist expects it to take another step up in July to +3.8%. By contrast in Japan, our economist sees headline inflation easing a bit to +3.1% in July, down from 3.3% in June. Otherwise, the main data release will be the August flash PMIs on Thursday, which will offer an initial indication on the global economy’s performance this month, particularly with the latest tariffs that have been imposed.

Elsewhere this week, we’ve got a few more earnings releases coming out, although it’s very much the end of the current season with over 90% of the S&P 500 having reported by now. This week’s highlights include several US retailers, including Walmart and Target, which should offer a fresh insight into consumer spending. Last Friday, the US retail sales numbers were pretty robust in July, with the headline reading up +0.5% (vs. +0.6% expected), alongside an upward revision to June as well. However, the University of Michigan’s consumer sentiment index painted a weaker picture for August, with the headline index unexpectedly falling to 58.6 (vs. 62.0 expected), alongside an uptick for inflation expectations.

Courtesy of DB, here is a day-by-day calendar of events

Monday August 18

- Data: US August New York Fed services business activity, NAHB housing market index, Japan June Tertiary industry index, Eurozone June trade balance, Canada July housing starts, June international securities transactions

- Earnings: BHP, Palo Alto Networks

Tuesday August 19

- Data: US July building permits, housing starts, Italy June current account balance, ECB June current account, Canada July CPI

- Earnings: Home Depot, Medtronic

Wednesday August 20

- Data: China 1-yr and 5-yr loan prime rates, UK July CPI, RPI, June house price index, Japan July trade balance, June core machine orders, Germany July PPI, Denmark Q2 GDP

- Central banks: FOMC meeting minutes, Fed's Waller and Bostic speak, ECB's Lagarde speaks, RBNZ decision, Riksbank decision

- Earnings: TJX, Lowe's, Analog Devices, Target, Estee Lauder

- Auctions: US 20-yr Bonds ($16bn)

Thursday August 21

- Data: US, UK, Japan, Germany, France and the Eurozone August PMIs, US August Philadelphia Fed business outlook, July leading index, existing home sales, initial jobless claims, UK July public finances, Eurozone August consumer confidence, June construction output, Canada July industrial product price index, raw materials price index, Norway Q2 GDP

- Central banks: Jackson Hole symposium, through August 23

- Earnings: Walmart, Workday

- Auctions: US 30-yr TIPS (reopening, $8bn)

Friday August 22

- Data: UK August GfK consumer confidence, July retail sales, Japan July national CPI, France August business confidence, July retail sales, Canada June retail sales

- Central banks: Fed's Chair Powell speaks at the Jackson Hole symposium

Finally, looking at just the US, the key economic data release this week is the Philadelphia Fed manufacturing index on Thursday. The minutes to the FOMC's July meeting will be released on Wednesday. There are several speaking engagements by Fed officials this week, including Governors Bowman and Waller, and remarks from Chair Powell at the 2025 Jackson Hole Economic Policy Symposium.

Monday, August 18

- 10:00 AM NAHB housing market index, August (consensus 34, last 33)

Tuesday, August 19

- 08:30 AM Housing starts, July (GS -1.0%, consensus -2.2%, last +4.6%): Building permits, July (consensus -0.2%, last -0.1%)

- 02:10 PM Fed Governor Bowman speaks: Vice Chair for Supervision Michelle Bowman will speak about fostering new technology in the banking system at the 2025 Wyoming Blockchain Symposium. Speech text is expected. On August 1, Bowman said, "With economic growth slowing this year and signs of a less dynamic labor market, I saw it as appropriate to begin gradually moving our moderately restrictive policy stance toward a neutral setting. In my view, this action would have proactively hedged against a further weakening in the economy and the risk of damage to the labor market."

Wednesday, August 20

- 11:00 AM Fed Governor Waller speaks: Fed Governor Christopher Waller will speak on payments at the 2025 Wyoming Blockchain Symposium. Speech text and Q&A are expected. On August 1, Waller said that he dissented in favor of cutting the policy rate by 25 basis points in July because "tariffs are one-off increases in the price level and do not cause inflation beyond a temporary increase, ... a host of data argues that monetary policy should now be close to neutral, not restrictive, ... [and] while the labor market looks fine on the surface, once we account for expected data revisions, private-sector payroll growth is near stall speed, and other data suggest that the downside risks to the labor market have increased."

- 02:00 PM FOMC Meeting Minutes: At its July meeting, the FOMC left the target range for the fed funds rate unchanged at 4.25-4.50%. The Committee noted that economic growth had “moderated in the first half of the year” but otherwise made minimal changes to the post-meeting statement. In his press conference, Chair Powell highlighted the softer growth pace in the first half of the year, noted that the labor market remains solid but said six times that it faces “downside risks,” and said that inflation is most of the way back to 2% and that a “reasonable base case” is that tariffs will have only a one-time impact on the price level.

- 03:00 PM Atlanta Fed President Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic will participate in a moderated conversation on the economic outlook. Q&A is expected. On August 13, Bostic said "I still have one cut in my outlook. That is predicated on the notion that the labor market stays solid." He added that "We have the luxury today to wait to make a policy adjustment because the labor market remains solid."

Thursday, August 21

- 08:30 AM Initial jobless claims, week ended August 16 (GS 225k, consensus 227k, last 224k): Continuing jobless claims, week ended August 9 (last 1,953k)

- 08:30 AM Philadelphia Fed manufacturing index, August (GS 6.5, consensus 5.5, last 15.9)

- 09:45 AM S&P Global US manufacturing PMI, August preliminary (last 49.8): S&P Global US services PMI, August preliminary (last 55.7)

- 10:00 AM Existing home sales, July (GS -1.0%, consensus -0.4%, last -2.7%)

Friday, August 22

- There are no major economic data releases scheduled.

- 10:00 AM Fed Chair Powell speaks: Fed Chair Jerome Powell will speak on the economic outlook and the framework review at the 2025 Jackson Hole Economic Policy Symposium. Speech text is expected.

Source: BofA, Goldman

Loading recommendations...