Submitted by QTR's Fringe Finance

Literally one day after I reiterated my extremely bearish outlook on regional banks — among other sectors — regionals went tits up today following a series of troubling disclosures from major players like Zions Bancorporation, Western Alliance, and Jefferies.

Reuters summarized today by noting Zions plunged roughly 12% after revealing it would take a $50 million charge tied to two underperforming commercial loans from its California division. Western Alliance dropped nearly 11% after it filed a lawsuit alleging fraud by a borrower, and Jefferies slid about 9% after admitting exposure to bankrupt auto parts maker First Brands.

Between the bankruptcies, lawsuits, and surprise losses, investors finally started to realize what I’ve been warning about for months: the toxic crap in regional banking isn’t isolated — it’s fucking everywhere.

The banks, analysts and the financial press tried to put a polite spin on it, calling the moves “unease over credit quality” or “idiosyncratic risk.” But let’s be honest — when multiple regional banks disclose major losses and lawsuits in the same breath, it’s not a coincidence. It’s contagion.

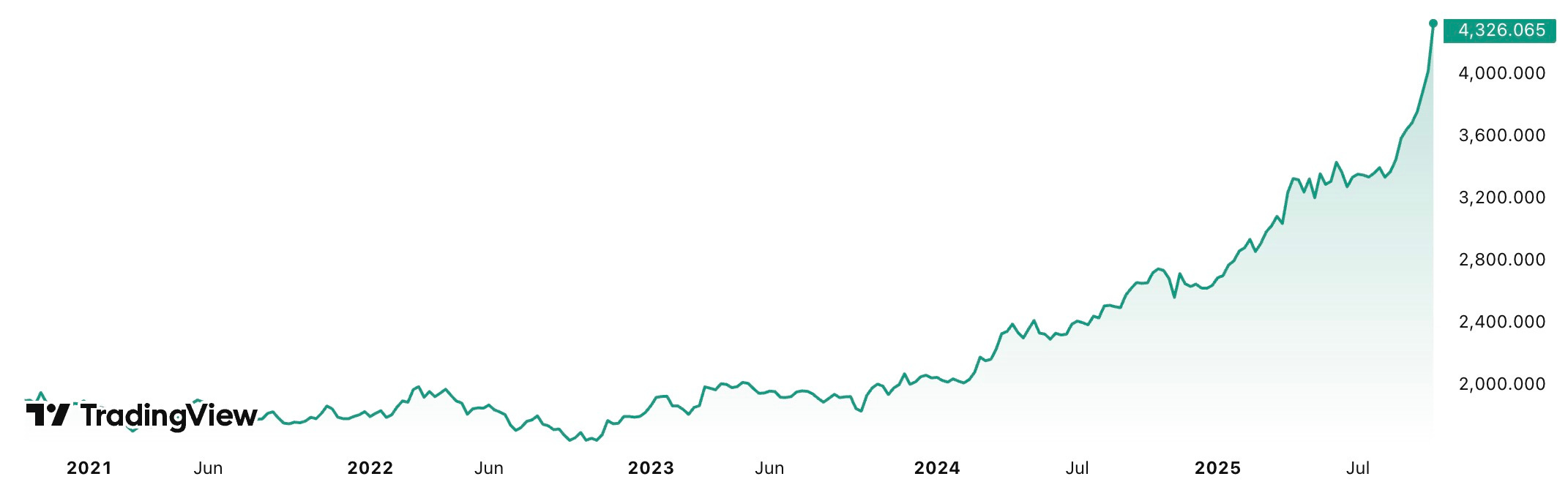

At the same time, a long-held prediction of mine that my podcast listeners and longtime Twitter followers will remember— that gold would eventually start moving more than $100 per ounce in a single session — has also come to fruition, as Zero Hedge pointed out this afternoon.

Chart: Zero Hedge

I made this call for $100 oz/day moves about five years ago, back when most of the coverage I received for being a “massive gold bull” came in the form of ridicule.

People told me, in all their hot shit modern monetary financial jargon, why I was wrong. Nevertheless, I persisted, drank 5 Moscow Mules before 10:30AM, took to a stage in front of a bunch of serious looking fucks in suits, and shrieked at the top of my lungs why buying gold (then at $1,319 an oz.) was the best way to, as my presentation was titled, “Short the Whole F*cking Thing”.

And now here we are. Both my bearish stance on banks and my bullish thesis on gold going apeshit are playing out— and together, they signal a much larger structural shift.

Or for lack of a hot shit modern monetary financial term: sh*t is breaking.

My longtime readers know I’ve said it repeatedly — when the fiat system breaks, or the stock market breaks, or the economy breaks, there’s going to be a “blow-off valve.” I’ve used this analogy for years, and that blow-off now appears to be happening in the metals. Just look at the charts — this is what a pressure release looks like.

As for the banks, make no mistake: there will probably be Federal Reserve intervention again at some point, maybe even full-blown bailouts. But things are going to get worse before they get better. As I pointed out just days ago with Jefferies — another firm now down double digits today — once confidence begins to erode in financial institutions, there’s no amount of PR spin or reassuring language that can stop the panic. I said this days ago when prepping my paid subscribers as to how I was dealing with the volatility that ended last week and what I was buying:

Then came the catastrophic headline that reminded me of Silicon Valley Bank: it was announced that Jefferies (JEF) was facing redemptions as banks look to shore things up after the First Brands bankruptcy (now with added off-balance-sheet debt goodness!)

This is exactly the type of news that can cause a run on a bank, and the timing couldn’t have been worse. It feels like Jefferies could be one of the first institutions under significant pressure as a result. Further, as I’ve been saying for the better part of the last year, regional banks were absolutely slaughtered today.

These are the banks with exposure to commercial real estate and subprime auto loans. I wouldn’t want to be in or near any of these banks anytime soon, as I think they’ll be the dominoes that wind up falling if this chaos continues into next week.

And — as I predicted, the dominos have kept falling.

Here’s the core issue: for years, these banks loaded their balance sheets with illiquid and risky assets, treating them as if nothing could ever go wrong. Losses weren’t even considered possible. Then suddenly, one or two of these loans blow up and rather than admitting that their underwriting standards are garbage and that they misjudged the collateral, banks hide behind fraud allegations against their counterparties. It’s a convenient narrative — one that plays well in the media but means nothing in reality. The jawboning and lawsuits are akin to PR stunts if you ask me, because it’s likely the borrowers are already wiped out.

As we saw recently with the bankruptcies of Tricolor and First Brands, the domino effect is simple. One counterparty scrambles for liquidity, which forces them to sell assets. Those assets are fire sold at actual bids well below marks, that pressure spreads, forcing other players to do the same. Before long, the entire sector is spiraling.

In my opinion, this is not “contained” or “idiosyncratic,” no matter how analysts try to frame it. Once this kind of contagion starts, it feeds on both liquidity risk and psychology. Investors and depositors lose confidence simultaneously, and before you know it, everyone’s racing for the exits.

Tricolor and First Brands may have set the spark, but what’s happening now is the fire. Real, tangible losses are surfacing, and there’s no stopping that process once it begins.

I’ve written many times before that banks — and most corporations, for that matter — never admit to losses until the absolute last minute. They stretch every accounting trick and narrative pivot they can before finally being forced to take charges. Any student of financial history knows this story. Companies will do anything to avoid acknowledging the consequences of their reckless decisions — until the numbers simply can’t be hidden anymore.

What we saw today in Zions and Western Alliance is exactly that very last option.

So here we are: a massive flight from fiat, reflected in gold’s surge and likely indicating the U.S. creditworthiness in jeopardy, combined with one of the stock market’s most fragile sectors — regional banking — finally cracking.

As for how it unfolds, no one can say precisely. But I expect the Fed to intervene at some point — maybe an emergency meeting, emergency cuts, or even behind-the-scenes liquidity operations. Bailouts are coming, but not before shit gets worse. Gold likely continues higher. Something is definitely already breaking in the silver market.

As I wrote earlier this week, regional banks were one of the ten areas of the market I said to avoid right now — and today’s carnage only reinforces that view. Here’s the other nine areas: 10 Areas Of The Market I'd Avoid Right Now

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Loading recommendations...