Authored by Riccardo Cumerlato via BondVigilantes.com,

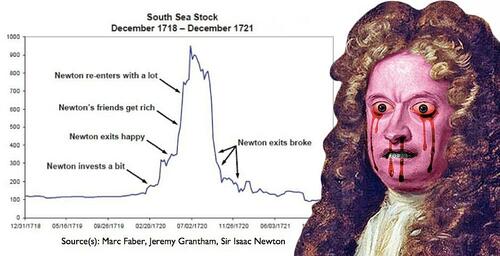

"Once upon a time, a learned man watched his friends grow rich by investing in a company that promised to revolutionise trade. Attracted by the prospect of easy riches, he joined the party, but was cautious at first, investing only small amounts. He even sold his shares for a tidy profit when he felt their price could no longer be rationally justified.

But, as the mania grew and the share prices kept increasing, he couldn’t resist… he bought back in, this time with more money, more conviction, and more confidence.

The bubble popped. He lost a fortune. The man was so shaken that he declared he could ‘calculate the motions of the heavenly bodies, but not the madness of people."

This story of Sir Isaac Newton and the South Sea Bubble of 1720 offers a cautionary tale about speculative excess, even among the most brilliant minds.

But why is it so difficult, even for one of the smartest people ever to have lived, to resist the lure of financial bubbles?

Human nature fuels the hype

During periods market exuberance, it’s not just valuations that defy gravity, so does reason. As Keynes famously put it, ‘It is better for reputation to fail conventionally than to succeed unconventionally’. In other words, it’s easier to join the crowd and be wrong together than to stand alone and be right too early.

For example, during the dot-com boom, financial news channels gave extensive coverage to IPOs, reflecting the excitement of the time.. Analysts who dared to question valuations were labelled ‘out of touch’.

Fund managers and analysts are human too – reading the same headlines, hearing the same chatter, and many will feel the same level of Fear Of Missing Out (FOMO). When everyone else is riding the rocket ship, sitting on the launchpad with a sceptical look and a clipboard isn’t just lonely, it can be career-threatening.

The bubble becomes a social phenomenon, not just a financial one.

Betting against a bubble is structurally hard

Even if a fund manager has the courage to go against the grain, the tools to do so are hardly user-friendly. Going long is simple: buy, hold, and enjoy the ride. Going short? That’s a different beast.

Shorting equities means borrowing stock, posting margin, and paying dividends to the lender. If the stock keeps rising, margin calls pile up. In fixed income, shorting often involves paying the bond’s coupon out of pocket; negative carry at its finest. All the while, the bubble may continue expanding while others enjoy a windfall .

As Keynes (again) warned, ‘markets can remain irrational longer than you can remain solvent’. And irrational markets tend to be very, very solvent.

Short sellers during the meme stock episode faced significant challenges, highlighting the risks of contrarian positioning in volatile markets. Hedge funds betting against GameStop found themselves squeezed by retail traders armed with Reddit threads and stimulus cheques. The stock soared, losses mounted, and some funds were forced to close positions at eye-watering losses. It was a masterclass in how expensive it can be to be right too early, and a reminder that the market doesn’t always reward rationality.

Contrarians need saintly patience (and patient saints)

To survive a bubble, a contrarian needs not just conviction, but also investors who are aligned with a long-term philosophy and understand the nature of contrarian strategies. Take Warren Buffett in the late 1990s. While dot-com darlings soared, Buffett stuck to his guns; no tech, no hype, just fundamentals. Critics said he didn’t ‘get it’. His returns lagged, but his investors stayed loyal.

When the bubble burst in 2000, Buffett emerged unscathed, vindicated, and wealthier. His story is a reminder that sometimes the tortoise really does beat the hare, if the tortoise has patient shareholders.

Buffett’s success wasn’t just about his investment philosophy, it was about the trust he had built with his investors over decades. They understood that his approach was long-term, even if the market wasn’t. Compared to investor that are more reactive to short-term performance , Buffett’s investor base acted more like partners than clients. That kind of long-term perspective is invaluable when swimming against the tide.

Source: Bloomberg

All told, the contrarian’s road can be lonely and often met with scepticism. You not only have to be right about the endgame, but also have to stay invested long enough to enjoy it. As one market wit quipped, contrarian investing can feel like ‘standing in front of an oncoming train and mumbling, ‘it will stop…’

History shows us that overheated markets cool down – bubbles tend to burst – but often not before testing the resolve of those who challenge prevailing market sentiment. Yet for the fund managers who can resist the rally, deploy the right tools, and manage patient capital, the rewards of contrarian courage can be substantial.

Going against the crowd in a bubble isn’t just a test of conviction, it’s an opportunity to shine when the dust finally settles.

Loading recommendations...