By Peter Tchir of Academy Securities

ProSec and Credit Risk

If you missed Thursday’s piece titled Is ProSec the New ESG, then I highly recommend checking it out. In fact, I almost stopped writing today just to make sure people saw that. So many interesting conversations on the back of that, and we think it deserves a read. We think that Production for Security (or ProSec) is going to shape government, corporate, and investment decisions for years to come.

It dovetails well with They’re Baaack… where we argue that “this time is different” in terms of trade negotiations with China.

In many ways, it is difficult (and painful) to realize that Academy published a joint T-Report/SITREP/Sustainability report titled Rare Earths – A National Security Threat back in February, 2021! Almost 5 years later, we seem to be finally waking up to the threat and the opportunity - ProSec™.

I really want to stop here. Mostly because I don’t want to dilute the message, but also because we have “stolen” some nice weather in mid-October and it seems to be a shame to be typing when there are so many better things to do. But…

More Money is Lost in Credit from Forced Selling than Defaults

Default this. Default that. So many headlines around banks and credit have been about defaults. I understand that – it is easy to understand and is scary (an entire cottage industry of looking for credit problems to spark the next GFC has emerged since the last GFC).

I understand the fascination.

But I always come back to two main themes:

You can only get a financial crisis from credit when a “SAFE” asset goes bad.

Forced selling is what creates credit losses, far more than defaults.

I’m not even sure if Silicon Valley Bank had to sell its Treasuries, but it was the mark-to-market losses that caused the run on the bank.

SIV’s, which bought highly rated bonds based on “haircuts,” had to liquidate in the GFC as losses breached the buffers that were built in.

I do not know the lowest price that the super senior held by AIG FP traded at on the credit side, but it was “dirt” cheap and never had a loss. The “super senior” on the mortgage side had losses that didn’t fully recover but the credit side did remarkably well, once the forced selling was taken out of the equation.

My “fun” fact is that the 3% - 7% tranche of CDX IG (the “mezz” tranche) even for a 10-year trade, has never suffered a loss. I think there were mark-to-market based CLOs that had losses in investment grade tranches, but I don’t think there has ever been a loss due to credit on any IG tranche of any CLO (which is why I periodically recycle the idea that it is more difficult to break a AAA CLO tranche than it is to get a perfect NCAA bracket).

So, the point here is to worry less about default risk and worry more about potential forced selling.

Is Forced Selling a Risk?

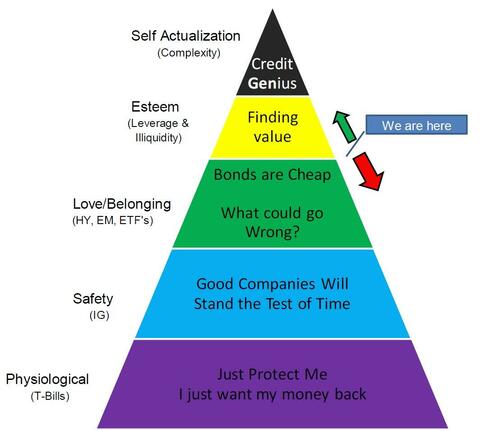

Let’s go back to our “Maslow’s Hierarchy of a Credit Bubble” chart. Yeah, maybe I’ve overused Maslow recently, but that and the Kubler Ross Stages of Grief are really useful.

In my view we’ve edged into the “Esteem” stage where leverage (which begets forced selling) is being used more frequently, but I think we are far away from the sort of trades where each small problem creates selling pressure, thereby exposing more problems.

Most Money Ever Lost By Smart Investors

This is somewhat tongue in cheek and has no empirical backing, but I think it is worth noting. Two credits where I think “smart” money lost massive amounts of money betting against the companies were:

Radio Shack. Their business model seemed to die circa the early 2000s. The brand, the locations, and the products didn’t seem to resonate. Yet, I think they didn’t have a bankruptcy until 2015 or so (I could check AI to get the right date, but it doesn’t matter – this company survived years and years past when “smart” money thought they would go under).

Brunswick. It was a company struggling before the GFC. Then during the GFC, one of their major product lines, boats, was on sale everywhere. How could this company survive? Here is their credit rating history from Bloomberg.

Baa3 08/01/2025

Baa2 08/29/2017

Baa3 08/30/2016

Baa2 06/23/2016

Ba1 06/23/2014

Ba2 11/14/2013

B2 04/20/2012

B3 07/13/2011

Caa1 01/06/2009

Ba3 10/20/2008

Baa3 07/10/2008

Baa2 03/26/2008

Baa1 07/08/2005

Look at the resilience! All the way back to investment grade!

We are debating including them in our ProSec list of companies as they manufacture boats domestically, and while “drones” get all the attention, there is a big push to develop “surface drones” to fight and defend the seas. The Navy has been discussing using a “Hellscape” as a deterrent to China going after Taiwan. The concept could go well beyond that. Could this company, with a market cap of just over $4 billion, fit into our “National Champions” framework?

The main point is that defaults often take far longer than anyone thought and sometimes fail to materialize as the corporations adapt and the business environment changes.

Private Credit Looks a Lot like Bank Lending in the 1990s

I will not belabor the point, but credit was, always, kind of, private.

One of the worst things the CDS market did is make it easy to push spreads wider, creating more forced sellers. Yes, mark-to-market is good, but are credits really as volatile as markets sometimes make them?

At its worst, small groups of lenders can create a “pretend and extend” environment. Keeping companies alive to avoid reporting losses. At its best, the same sort of behavior allows companies the breathing room they need to fix themselves.

Mark-to-market on credit is one of the trickier things out there. Anyone who traded for a living and found a “TRACE Bandit” who would use late day trades on small sizes to create TRACE prints knows how well people can be forced into “forced selling.” At the opposite end of the spectrum, denial that a credit issue is occurring is equally wrong.

I’m not sure where we are in this cycle, but everything tells me that naming something “private” helped in the AUM growth as it tied nicely with “private equity” and is now hurting the industry, despite the fact that credit has always kind of been private.

Trying not to be dismissive of the risks, but let’s not get too panicked over terms.

Bottom Line

Sell credit, of all types, if you are worried about forced selling.

If there are sellers of private credit, who cannot get bids, they will sell “liquid” credit, starting with HY (including ETFs) and move on from there, and it will impact companies that haven’t done anything wrong.

I do not see forced selling and believe that credit risk is not systemic. Therefore I remain comfortable with credit.

Away from that:

Own ProSec in every asset class (commodities, stocks, and bonds).

Shy away from companies that will struggle if “this time is different” with China – which we think it is – as China is driving the narrative more than the U.S.

Good luck and enjoy the weather! (If you are having good weather. Otherwise, enjoy something else).

Loading recommendations...