By Ben Hertz-Shargel of Woods Mackenzie

As industry concerns over an AI bubble mount, the scale of data center ambitions continue to grow. As of mid-October, the US data center pipeline reached 245 GW of planned capacity, driven by a handful of enormous, speculative projects. These projects, and the renewable deals hyperscalers are signing, skew heavily toward Texas. More than a quarter of pipeline capacity targets the state, whose pipeline nearly doubled from 35 GW in Q1 to 67 GW in Q3.

Data Center Alley gives way to Data Center Prairie

It is conventional wisdom that for data center developers, ‘access to power’ has become the mantra. That is, the importance of fiber proximity to end customers and other data centers has been superseded by the imperative to secure power from utilities. The giga-scale campuses that have been announced this year, sited in Pennsylvania, Wyoming, and particularly West and North Texas, signal yet another pivot in strategy. Developers have increasingly given up confidence that utilities can meet their power and timeline demand and instead seek to build their own generation based on local natural resources.

Most frequently this resource is natural gas, with a particular focus on the Permian in Texas. Pacifico Energy’s 5-GW GW Ranch, poolside’s 2-GW Project Horizon, and FO Permian’s 5-GW campus in Midland County are examples. The gas network in the US is at capacity, and building new gas generation far from supply means paying for and - perhaps more importantly for developers - waiting for new pipeline capacity.

In some cases, it should be noted, campuses are being leveraged for their scale and solar or wind resource, such as Tract’s data center parks in Nevada and Utah, and Quantica’s Big Sky Digital Infrastructure campus in Montana. While more headlines have made about the potential for batteries to make data centers flexible assets, we’ve found that batteries are being planned much more commonly to balance renewables at large campuses and to add needed fast-ramping capacity to onsite gas.

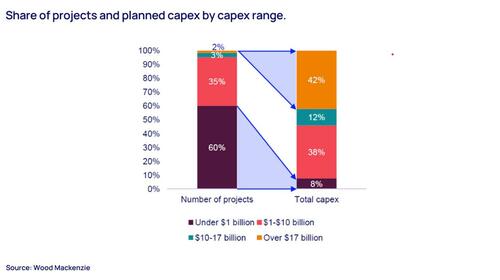

Distorting the capital landscape

These mega campuses not only reflect a new siting strategy: they distort the capital landscape. The 2% of projects over US$17 billion represent 42% of overall capital deployment, with the 60% of projects below US$1 billion contributing only 8%. With questions already intensifying regarding froth in project investment and company valuations, these projects promise to drive even more froth.

The two highest-cost projects, Project Jupiter in New Mexico (US$160 billion) and Project Kestrel in Missouri (US$100 billion), are an order of magnitude more expensive than the campuses being developed by companies like Meta and Microsoft, without appreciable increase in IT infrastructure. They are notably being funded through novel financial engineering: Their developers will be both the payers and payees of industrial revenue bonds (IRBs) issued by the local government, a contrivance that enables tax benefits.

Betting big on onsite generation

The new energy-chasing campuses are committing to onsite generation in a way that developers have been hesitant to in the past. Hyperscalers have been very clear that they prefer grid power, which requires less operating risk, shorter contract commitments, and no exposure to scope 1 emissions. Developer commitment to onsite generation reflects a bet either that hyperscalers urgency to deploy will overcome their concerns, or that the developer will be able to sell to a new generation of hyperscalers with greater risk tolerance and less concern for sustainability.

The net result is that while the number of projects in the pipeline with onsite generation has increased only to 10%, these projects represent a whopping 34% of pipeline capacity.

Unsurprisingly, the vast majority of sites are in Texas, and the technology is gas turbines.

This trend could have significant implications for both energy affordability and reliability. Whether on- or off-grid, projects with utility-scale gas generation will increase gas burns, competing with LNG exports and raising the long-term price of natural gas. This will drive up both gas and electricity bills across the country. To the extent to which turbine-based projects are off-grid, utilities will have an even harder time obtaining turbines given production limitations. That could pose reliability challenges for on-grid load growth, including electrification.

Whether or not a bubble bursts, these affordability and reliability challenges are likely to provoke state intervention to protect customers. As that begins happens, all bets are off.

Loading recommendations...