By Michael Every of Rabobank

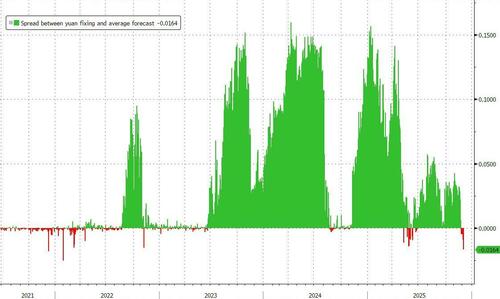

Markets start the day mixed. Bad US ADP jobs data saw the old rule that this is bullish for rates, so stocks. By contrast, Australian household spending of 1.3% m-o-m (regardless of how many it covers) saw rate hike bets pick up, with the 3-year yield above 4% for the first time since January. This morning, China also set the daily reference rate for CNY significantly weaker than expected, underlining its rule remains that its currency goes where it wants, not markets – and it doesn’t want it too strong even as its trade surplus reaches staggering dimensions.

But the rules are changing. The FT says hedge funds warned the White House about picking the head of the National Economic Council, Kevin Hassett, as the next Fed Chair because he “will be swayed by Trump on interest rates.” As our US strategist Philip Marey notes in his 2026 Outlook, that’s exactly what we expect to happen. Moreover, as underlined here many times before, that’s potentially just part of the new central banking rules as economic statecraft wins, and technocracy loses. Indeed, Bloomberg reports Treasury Secretary Bessent is floated to replace Hassett at the top of the NEC, double hatting like Secretary of State Rubio. ‘Move fast and break things’ comes to mind.

Likewise, Brussels floated “emergency” powers to raise €210bn from frozen Russian assets as: NATO’s head pledged it’s “ready to do what it takes” to protect Europe - when it isn’t; the Telegraph warned ‘Trump may now abandon both Russia and Ukraine’ - as Rubio will skip the NATO foreign ministers’ meeting for the first time in 20 years and send a NATO sceptic instead; and talk is of ‘Europe's race back to the draft’ as “Europe’s defence debate now centers on one blunt question: how many people can fight if they must?” – and “very few” is the clear answer.

The EC proposal is still de facto seizure of Russian assets with extra pledged protections for Belgium vs. Moscow’s retaliation and qualified majority voting under Article 122, allowing for ‘exceptional measures’ when the European economy is at risk, to block Hungarian or Slovakian vetoes. EU leaders will make a final decision on 18 December: if no deal can be struck, von der Leyen stated the EU will resort to joint debt issuance, as in Covid. Either way, rules are going to be broken, it seems.

Yesterday, Europe also broke more of its preferred free-market rules. It banned Russian LNG by end-2026 and pipeline gas by September 2027, with oil floated by end-2027; revived its China de-risking plans in an economic security package; threatened to use its Anti-Coercion Instrument vs. China; pushed a magnet recycling plan; and announced a target for 70% of ‘critical goods’ to be “made in Europe”. Make Europe Great Again?

But can Brussels focus as the rule of law comes down on it? Politico argues, ‘Fraud probe risks plunging EU into biggest crisis in decades’ and “People who don’t like von der Leyen will use this against her.” Euractiv says, ‘Welcome to the jungle: Raids, arrests, and a crisis of EU credibility’, and “As far-right parties hammer Brussels over corruption, the EU’s own investigators may be proving them right.” Reportedly, top Commission official Sannino is also taking early retirement amid this scandal. For those thinking maybe economic statecraft is a flag to rally round, Germany’s far left just saved Chancellor Merz from a potential humiliation on pensions by abstaining in a key vote. What if a real military draft or joint debt issuance has to be voted on in Berlin, Paris, Madrid, Rome, etc.?

For the UK, this is tricky given Labor leans towards Europe, with suggestions it might consider a rule-breaking push to re-enter the Customs Union. Yet the EU’s new stance means the UK couldn’t supply most critical goods on top of limiting its ability to trade freely with the US, the Anglosphere, Japan, or South Korea, etc., unless/until a higher tariff pan-Western trade umbrella is eventually raised vs. China (which we see as the broad Trump plan). Grand macro strategy is hard when you don’t know you are in it.

At the macro level, some rule changes are the rule. In the UK, the OBR, stuck in a scandal, says billions in green energy subsidies were excluded from the recent, controversial Budget, as Chancellor Reeves has ordered a Treasury inquiry over leaks about it. (Not the officially sanctioned ones.)

In China, Shanghai launched a clampdown on “property market doom-mongering,” with up to internet 70,000 accounts shut down. That’s after the government reportedly told two private data agencies to withhold monthly home sales data for November, and until further notice. There are questions over when we will see those series return: presumably when sales are going up… which could be some time. Yet neither this nor the news that Chinese AI and big data are officially to guard against Western values and promote socialism will shake the market rule that says China is very investable vs. the previous “uninvestable.” THAT isn’t made by portfolio managers or analysts, but the MSCI equity index review process. Until one day it isn’t.

In the US, Axios reports the White House response to political and economic pressures is to double down on “ultra-MAGA”. As a new example, car fuel efficiency standards are to be relaxed to try to bring down vehicle prices, after floated changes in health insurance and mortgages.

Part of that will also be a White House focus on robotics to match that on AI, mirroring China. Yet how that eases MAGA voters’ concerns over looming job losses is unclear, unless robots first replace the millions of workers Trump wants to deport? Logically, labor costs don’t have to rise if so – and yet that again wouldn’t please many voters either. Mirroring rule breaking because of cost pressures and potential geopolitical emergencies also sees the Pentagon deploying a new, cheap kamikaze drone directly copied from an Iranian design, the Shaheed (as used by Russia vs. Ukraine, and which was unwittingly developed in part by British universities, “because markets”).

Ultra-MAGA also seems OK with its rule change towards backing regime change in Venezuela, as the Telegraph claims Maduro’s ‘terms of surrender’ were unacceptable to Trump: a blanket amnesty for himself and top officials as well as $200m. However, there rumours fly of a looming Maduro exit to various global locations, including Qatar. For its part, China is seen as unlikely to aid Venezuela: its experts reportedly think a Trump takeover could benefit Beijing if ‘spheres of influence’ come back into vogue, which obviously brings Taiwan into the mix again.

To come full circle, once spheres of influence are brought into the debate, and they are, the underlying emergency in Europe is even clearer. It doesn’t have one - it IS one.

If so, many more rules are going to be broken; either that or comfortable delusions will be. Remember:

IN CASE OF EMERGENCY BREAK RULES

Loading recommendations...