Our Dec. 23 note, "Why the Price of Uranium Is About to Soar," was published just days before uranium futures surged 25% to above $100 per pound. Prices have since corrected about 10% to around $91 per pound, but the broader thesis remains intact: up and to the right.

As we first outlined to readers since December 2020 (read here), uranium has emerged as the next gold. In an era of data centers and a rush to power up America with new nuclear reactors and to build next-generation grids capable of supporting explosive data-center growth and broader electrification trends, the world faces a massive uranium supply deficit that is only set to worsen by the end of the decade.

Drawing on Goldman's Global Reactor Tracker, we provide readers with the latest developments, data points, and progress across North America, Europe, and Asia that only reinforce our bullish thesis on Cameco Corp and peers. We expect this to remain a solid bet on the industry this decade. Just remember, the CCJ call was made in December 2020 at around $11 per share.

Analysts led by Brian Lee have done all the hard work in capturing a snapshot of the uranium industry.

North America

1/16/26 - United States - NASA and the DOE have renewed their commitment through an MoU to develop a fission power source for the Moon and future Mars missions. This initiative, driven by an Executive Order, prioritizes deploying a lunar surface reactor by 2030 to provide safe, efficient, and continuous electrical power for sustained lunar missions, independent of sunlight or temperature. This aligns with NASA's 2025 Integrated Lunar Power Strategy, which considers nuclear fission as a primary power generation technology.

1/29/2026 - Canada - Saskatchewan's government and SaskPower are evaluating large nuclear reactor technologies alongside existing SMR plans. This dual strategy aims for energy security and future electricity demand, utilizing Saskatchewan's uranium. GE Hitachi's BWRX-300 SMR is planned for mid-2030s deployment near Estevan, while Westinghouse's AP1000 and AP300 SMRs are also being explored. Large reactors could take 15-20 years to become operational.

1/29/2026 - Canada - Westinghouse and Tetra Tech Canada are collaborating to deploy Westinghouse's AP1000 and AP300 reactors in Ontario. This partnership supports Ontario's exploration of new nuclear generation at the Wesleyville site, where Ontario Power Generation (OPG) is evaluating various reactor technologies. The AP300 SMR aims for design certification by 2027 and operation by 2033.

Europe

1/19/26 - Slovakia- Slovakia and the USA have signed an Intergovernmental Agreement to advance Slovakia's nuclear power program. This includes a new 1,200 MWe unit, possibly a Westinghouse reactor, at the Bohunice Nuclear Power Plant, targeting 2040-2041 operation. This follows a feasibility study supporting SMRs in Slovakia by 2035.

1/23/2026 - Denmark - Denmark is studying new nuclear technologies, including SMRs, to assess their potential and risks. This aims to inform a possible lifting of its 1985 nuclear power ban, driven by energy security and growing SMR interest. The analysis, covering economic viability and regulatory needs, is due Q2 2026 and is supported by a Nuclear Power Alliance.

Asia and other

1/2/2026 - South Korea - South Korea's Nuclear Safety and Security Commission has issued an operating license for Saeul Nuclear Power Plant unit 3, an APR1400 reactor, with commercial operation targeted for January after fuel loading and testing. This unit, featuring enhanced safety measures and contributing 1.7% of Korea's total power, marks a significant step following the reversal of the country's nuclear phase-out policy.

1/2/2026 - Russia - The first VVER-TOI power unit at Russia's Kursk II nuclear power plant was connected to the grid on Dec 31, reaching an initial capacity of 240MW, with a full capacity of 1,250MW. This new unit, is part of a project to replace the older RBMK-1000 reactors at the existing Kursk plant, with all four new units targeted for operation by 2034 (here).

1/5/2026 - China - Unit 2 of China's Zhangzhou nuclear power plant, a Hualong One reactor, has entered commercial operation, completing the first phase of the project and bringing China Nuclear Power Corporation's total operating units to 27. This plant, once fully completed with six units, is expected to provide over 60 billion kilowatt-hours of clean energy annually, significantly contributing to China's energy structure and "dual carbon" goal (here).

1/6/2026 - Russia - Russia's Bilibino Nuclear Power Plant permanently shut down its last unit on December 30 after 51 years, replaced by the 70 MW Akademik Lomonosov floating nuclear power plant. This marks Rosenergoatom's first complete plant shutdown, with unique decommissioning challenges in the Arctic, aiming for full rehabilitation by 2055 (here).

1/15/2026 - Russia - Russia has approved a five-year life extension for Leningrad-4, an RBMK-1000 reactor, allowing it to operate for a total of 50 years until 2031 after comprehensive modernization and safety checks. This extension ensures continued electricity supply for northwest Russia and the production of medical isotopes, complementing the ongoing replacement of older RBMK units with new VVER-1200 reactors at the site.

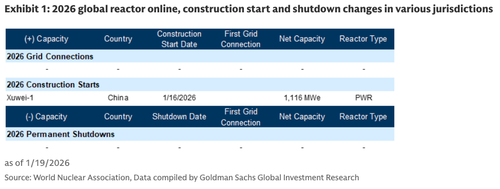

1/16/2026 - China - China has commenced construction on Unit 1 of the Xuwei nuclear power project, a "world's first dual-coupling demonstration" combining Hualong One PWRs with a high-temperature gas-cooled reactor to provide both electricity and industrial heating. This innovative project is projected to annually supply 32.5 million tonnes of industrial steam and over 11.5 billion kWh of electricity, significantly reducing coal consumption and carbon emissions.

1/19/2026 - Japan - Tepco postponed the scheduled January 20 restart of unit 6 at its Kashiwazaki-Kariwa nuclear power plant. The delay occurred after a safety alarm failed to sound during a control rod withdrawal test on January 17. Tepco identified and corrected an error in the alarm's settings by January 18, confirming its proper function. This Advanced Boiling Water Reactor had been offline since the Fukushima Daiichi accident (here).

1/19/2026 - Russia - Rosatom Director expects four foreign nuclear units to start in 2026: Bangladesh (Rooppur), Turkey (Akkuyu), and two in China. Rosatom exceeded 2025 goals despite sanctions, advancing Hungary's Paks II and Turkey's Akkuyu projects. He discussed yuan financing, 100-year unit operation, advanced nuclear tech, and the Northern Sea Route. Zaporizhzhia NPP Unit 1 was licensed in 2025, with generation conditional.

1/26/2026 - South Korea - South Korea confirmed plans for two new large nuclear reactors and 700 MW of SMR capacity by 2038, as part of its 11th Basic Plan. The strategy prioritizes nuclear and renewables to reduce carbon emissions, projecting increased electricity demand and a rise in carbon-free energy to 70% by 2038. KHNP will launch a bidding process for host cities by 2027, targeting reactor completion by 2037-2038.

1/26/2026 - Argentina - Argentina's CNEA plans to reactivate its Neuquén Heavy Water Industrial Plant (PIAP), mothballed since 2017. Once the world's largest facility, it will undergo maintenance and refurbishment to restart production, aiming for revenue generation and exports. A May 2025 MoU with Candu Energy supports the restart and long-term heavy water acquisition, with Argentina's plants needing 485 tonnes and surplus available for export.

1/19/2026 - Russia - Russia's Roscosmos has contracted NPO Lavochkin to develop a lunar nuclear power station by 2036, requiring three missions (2033-2035). This station will power Russia's lunar program and the International Lunar Research Station (ILRS), a joint Russia-China initiative also involving Rosatom and the Kurchatov Institute.

SMR announcement tracker

1/6/2026 - Bulgaria - Blue Bird Energy and Synthos Green Energy formed a joint venture to deploy up to six GE Vernova Hitachi Nuclear Energy BWRX-300 small modular reactors (SMRs) in Bulgaria, aiming to provide affordable, reliable energy. This expands Synthos Green Energy's European SMR strategy, which includes plans for 24 BWRX-300 units in Poland.

1/8/2026 - United States - Terrestrial Energy and Oklo have signed agreements with the US Department of Energy for pilot projects under the Advanced Reactor Pilot Program. Terrestrial Energy will develop a pilot Integral Molten Salt Reactor (IMSR) to expedite commercialization of its 4th generation technology, while Oklo will build a radioisotope pilot plant for medical and research isotopes. These agreements, leveraging Other Transaction Authority, aim to fast-track advanced reactor innovation and achieve criticality by July 2026.

1/8/2026 - China - China's ACP100 (Linglong One) SMR at the Changjiang site successfully completed its non-nuclear turbine test run on December 23. This 125 MWe SMR, developed by CNNC, is the world's first commercial land-based SMR to reach this milestone, verifying its conventional island systems. Commercial operation is targeted for the first half of 2026.

1/12/2026 - United States - Ameresco and NANO Nuclear signed an MoU to deploy NANO's KRONOS, ZEUS, and LOKI microreactors on US federal and commercial sites, with Ameresco leading EPC. DS Danseok also signed an MoU for NANO microreactors in South Korea. This builds on Ameresco's prior IMSR collaboration.

1/16/2026 - Slovakia - A Project Phoenix study confirmed Slovakia's suitability for SMR deployment, with four sites (Bohunice, Mochovce, Vojany, US Steel Košice) meeting baseline criteria. The next steps involve developing a regulatory framework, detailed site investigations, and public consultation. SMRs could be operational by 2035, enhancing energy security and decarbonization.

1/16/2026 - Uzbekistan - Uzbekistan and Rosatom are progressing on a nuclear power plant project, with first concrete for the SMR anticipated "well before December" 2026, targeting spring pouring. The project initially involved six RITM-200N SMRs (330 MW total), with the first unit critical by late 2029. The plan later expanded to include two large VVER-1000 units and two 55 MW RITM-200N SMRs. Excavation for the first SMR is underway in the Jizzakh region.

1/29/2026 - United States - NextEra Energy plans up to 6 GWe of SMR capacity, primarily for data centers. They are evaluating SMR manufacturers and have identified 6 GW of co-location opportunities at existing or new sites. The Duane Arnold plant will restart by 2029, supported by a Google power purchase agreement. This is part of NextEra's "15 by 35" strategy, aiming for 15-30 GW for data centers by 2035.

Global reactor critical updates

In the month of January, there have been few changes to new reactor construction starts, grid connections, shutdowns, or restarts.

Global reactor construction tracker

The epicenter of the world's nuclear reactor buildouts is China.

Global reactors under construction.

China.

Latest on spot uranium prices:

Spot momentum continues into the new year. Uranium pricing has shown continued strength in the new year, up +21% over the month of January, with spot climbing over $100/lb for the first time in almost two years. Spot market activity was robust with a total of 90 transactions involving 9mn/lbs of uranium. Pricing momentum intensified in the last week of January as Sprott raised funds and accumulated ~2.5mn lbs of uranium. The spot price currently sits at ~$91/lb compared to $82/lb in December.

Term pricing moderate. Term pricing increased in January by $2 to $88/lb, marking its highest level since May 2008. However, term market activity was moderate throughout the month, with one utility finalizing an off-market selection for uranium deliveries starting in 2029. A new utility also entered the market seeking approximately 1.2 million pounds of uranium for delivery in the same year. Additionally, non-U.S. utilities were actively evaluating offers for longer-term uranium and EUP requests.

KAP guidance update. On 2/2/26, KAP provided its 4Q25 operations and trading update, which included 2026 production guidance. The company's 2025 production of 25,839 tonnes uranium (tU) (67.2mn lbs) was in line with guidance of 25,000-26,500 tU. Additionally, KAP provided 2026 guidance of 27,500-29,000 tU (71.5-75.4mn lbs), signaling growth of 9% yoy that is driven by the planned ramp of its JV Budenovskoye, which is fully reserved under offtakes from 2024-2026. Importantly, the midpoint of 2026 guidance is ~5% below its subsoil use contract annual production of 29,697 tU, which was lowered by ~10% from 32,777 tU in August 2025. Additionally, the guidance is dependent on the availability of sulfuric acid, which was a key factor that weighed on production in 2025. We note that KAP could potentially lower its production another ~15% and be within the confines of the +/- 20% threshold provided in its Competent Person's Report.

Color on nuclear stocks:

Nuclear stocks have seen mixed performance over the past three months, with our nuclear coverage averaging a -13% return over the period compared to the S&P which returned 3%. Performance was collectively positive across uranium-levered names (CCJ/UEC), likely in large part owing to the recent rally in spot uranium pricing, while SMR technology players have traded significantly off. With respect to investor positioning, UEC was the only stock in our coverage which saw an increase in short interest, as the stock continues to rally, up 26%/35% over the past 3mo/12mo. Across the remainder of our coverage, short interest decreased across both CCJ and OKLO while SMR saw the largest decrease in short interest.

Cameco