The 10-year treasury yield rocketed up to near 5%, and analysts say it’s because the economy is strong despite higher inflation.

But if the economy is so strong, why are Americans so indebted, cash-poor, and desperate?

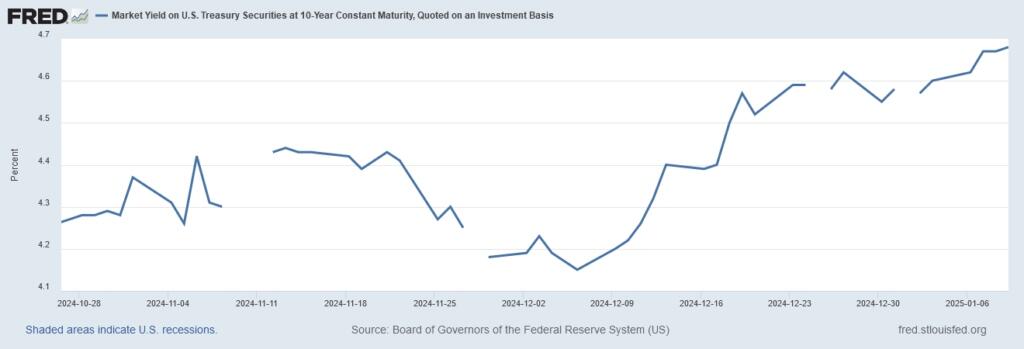

10-Year Treasury Yields

The recent spike in 10-year yields has been explained away by many as the result of a strong economy, but they fail to mention that high inflation makes the 10-year yield harder to contain. High 10-year yields support higher rates for things like car loans and mortgages, and with the world still under the inflationary spell of COVID-era QE and free money “stimulus,” the only answer may be—you guessed it—more free money QE to “stimulate” an economy that’s already stuck in an infinite loop of inflation. As Peter Schiff said recently:

“I think that they’ve already lost control of the long end of the bond market…the Fed is going to be pressured to try to lower long-term rates, and the only way it would be able to do that is by buying the long term bonds, and the only way to get the money to do that is to print it.”

But not even the Fed has a clue for how it would deal with a stagnation scenario.

“It was almost humorous and even it got a laugh out of Powell. A reporter asked him at the last press conference, ‘What’s your plan for stagflation?’ And he laughed and says, ‘Our plan for stagflation is that we’re not going to have it.’”

But we already do. For now. markets are also still trying to figure out how to react to Trump’s win, and uncertainty breeds volatility. So, high inflation coupled with uncertainty and “strong” economic data are the three factors being attributed to the spike in yields. The inflation part is partially right; the only problem is that it doesn’t go far enough, because inflation is actually much worse than what’s being reported. The other problem is that the “strong jobs data” being partially blamed for the rise in yields is never really as strong as what gets reported, as the jobs reports and other economic data are unreliable and designed to paint as rosy a picture as possible.

As Treasury yields keep rising, mortgage rates keep going up, and basic needs keep getting more expensive, 2025 is already shaping up to be a marvel of stagflationary chaos. As predicted, the bond market and broader economy are getting spooky, and Central Banks will keep buying gold to protect themselves from the same problems that government and central bank interventions create.

The question is, how many Americans will protect themselves? The answer is very few, as the average American has hardly any money saved and is living paycheck-to-paycheck while becoming increasingly over-indebted. After all, when economies are extremely weak or extremely strong, they will always be what decides elections even if the root causes go far deeper than any one president, which they always do.

But when Americans are struggling, seeing drastic price increases, and watching with enraged awe as their government continues donating taxpayer money to proxy wars in Ukraine and Israel as American cities flood, burn, and lose their critical infrastructure, they’re going to vote for the other candidate. So, while Trump signed the inflationary COVID stimulus checks, he was able to convince voters even after losing in 2020 that he should be given another chance after the economic deterioration of the last four years..

Whether or not Trumponomics itself ends up being inflationary, central bank monetary policy will always revert back to the only real tool in its toolbox, which is printing money. Whether or not DOGE, tariffs, and other promises materialize, the result of statist intervention to bring down prices is almost always, ironically enough, higher prices. Even if the intervention causes costs to go down in one place, they generally go up somewhere else.

That’s because there are no free lunches in economics, no matter what central bankers may say.